Limited Pay Life Insurance: Best Companies and Strategic Payment Options (2026)

A limited pay life insurance policy lets you fund permanent whole life insurance within a defined time frame — then never pay another premium for the rest of your life. The coverage stays in force, the cash value keeps growing, and the death benefit remains intact.

But here’s what most guides won’t tell you: the value of a limited pay policy depends entirely on the company you choose and how the policy is designed. A 10-Pay from a mutual company with strong dividends and a properly structured paid-up additions rider is a fundamentally different financial instrument than a 10-Pay from a stock company with no dividends and a death-benefit-first design.

This guide covers both — the mechanics of limited pay life insurance and the companies that actually deliver the best results for cash value growth and wealth building.

Table of Contents

- Best Limited Pay Life Insurance Companies

- What is Limited Pay Life Insurance?

- Types of Limited Pay Policies (With Sample Rates)

- Real Policy Performance: 38-Year Case Study

- Advantages and Disadvantages

- Policy Design: Why Structure Matters More Than Payment Schedule

- Limited Pay vs. Other Life Insurance Types

- Riders and Additional Coverage Options

- How to Choose the Right Limited Pay Policy

- Frequently Asked Questions

Best Limited Pay Life Insurance Companies

The best limited pay life insurance comes from dividend-paying mutual insurance companies that offer flexible policy designs with paid-up additions riders. These are the carriers we consistently recommend for clients focused on cash value accumulation and wealth building through limited pay whole life.

1. Penn Mutual — Best Overall for Cash Value Design

Penn Mutual has been in business since 1847 and remains one of the most innovative mutual insurers for whole life policy design. Their limited pay options include 7-Pay, 10-Pay, 15-Pay, and 20-Pay structures, all available with their Enhanced Permanent Paid-Up Additions Rider (EPPUA), which allows you to direct the majority of your premium toward cash value growth rather than base death benefit.

What sets Penn Mutual apart is the EPPUA’s catch-up provision — if you underfund your paid-up additions in a given year, you can make up the shortfall the following year. That flexibility is rare and valuable for business owners with fluctuating income. Penn Mutual also offers accelerated underwriting (ACE) on policies up to $5 million, meaning qualified applicants can skip the medical exam entirely.

A.M. Best Rating: A+ (Superior) | 2026 Dividend Payout: $265 million (record) | Dividend Interest Rate: 6.00%+ | Distribution: Non-Captive

2. Lafayette Life — Best for Pure Cash Accumulation

Lafayette Life, a subsidiary of Western & Southern Financial Group, is one of the premier limited pay whole life companies for clients focused on cash accumulation and infinite banking strategies. Their whole life product is specifically designed for high early cash value when structured with paid-up additions.

Lafayette Life practices non-direct recognition for policy loans, which means your dividend is not affected by outstanding policy loans — a critical advantage for anyone planning to use their policy as a private banking system. Their limited pay options are available in 10-Pay, 15-Pay, and 20-Pay structures.

A.M. Best Rating: A+ (Superior) via Western & Southern | Comdex Score: 96 | Distribution: Non-Captive

3. Foresters Financial — Best No-Exam Limited Pay Option

Foresters may be the least recognized name on this list, but their limited pay whole life product offers strong cash accumulation without requiring a medical exam — a significant advantage for clients who want to move quickly or have health concerns that complicate traditional underwriting. Their limited pay whole life is designed for straightforward cash value growth with competitive dividends.

As a fraternal organization, Foresters also provides unique member benefits at no additional cost, including scholarships, community activity grants, and orphan benefits.

A.M. Best Rating: A (Excellent) | Comdex Score: 85 | Distribution: Non-Captive

4. MassMutual — Strongest Financial Backing

MassMutual offers the most financially secure limited pay option on the market. With a perfect 100 Comdex score and an A++ rating from A.M. Best, this is the carrier you choose when guarantees and long-term stability matter most. Their limited pay options include Whole Life Legacy 10-Pay and 20-Pay structures.

MassMutual shattered records in 2025 with an unprecedented $2.5 billion dividend payout and a 6.40% dividend interest rate. Their accelerated underwriting program covers policies up to $20 million without a medical exam for qualified applicants — the highest no-exam limit in the industry.

A.M. Best Rating: A++ (Superior) | Comdex Score: 100 | 2025 Dividend Payout: $2.5 billion | Distribution: Non-Captive

Beyond Limited Pay: The Cash Value Optimization Approach

Limited pay whole life is a powerful structure, but it’s only one piece of the puzzle. The real advantage comes from how the policy is designed — specifically, the balance between base premium and paid-up additions. A properly designed high cash value whole life policy with a PUA rider can have 80-90% of premiums directed toward cash value in the early years, regardless of whether it’s a 10-Pay, 20-Pay, or whole life to age 121 structure.

For clients using life insurance as the foundation of an infinite banking strategy or Volume-Based Banking system, the payment schedule matters less than the policy architecture. A whole life to age 121 with a heavy PUA rider can outperform a limited pay policy with a death-benefit-first design.

The takeaway: Don’t choose a payment schedule before you understand your design options. Schedule a consultation and we’ll show you side-by-side illustrations comparing limited pay vs. whole life to 121 for your specific situation.

What is Limited Pay Life Insurance?

Limited pay life insurance is a type of whole life insurance where you pay premiums for a specified period — typically 7, 10, 15, or 20 years, or until age 65 — after which the policy is fully paid up. No more premiums are due, but the coverage, cash value, and death benefit remain in force for your entire lifetime.

The defining advantage is straightforward: you compress your premium obligation into a finite window, then own a permanent asset free and clear. The policy continues to earn dividends (from mutual companies), the cash value continues to grow on a tax-deferred basis, and the death benefit passes to your beneficiaries income-tax-free.

How Paid-Up Additions Change the Equation

There are two fundamentally different ways to structure a limited pay life insurance policy, and the difference is significant:

Traditional design (death benefit focus): The majority of your premium goes toward the base policy, which funds the death benefit. Cash value grows slowly in the early years and accelerates over time.

High cash value design (PUA focus): The policy is structured with a paid-up additions rider so that the majority of your premium goes toward purchasing additional paid-up insurance. This dramatically accelerates cash value growth in the early years while still building the death benefit over time through dividends and paid-up additions.

If your goal is to use limited pay whole life as a wealth-building tool — whether for infinite banking, retirement income supplementation, or generational wealth transfer — the high cash value design is the approach that makes the strategy work. A limited pay policy without a properly structured PUA rider is just expensive life insurance.

Types of Limited Pay Life Insurance Policies

| Payment Type | Premium Duration | Best For | MEC Risk |

|---|---|---|---|

| Single Premium | One lump-sum payment | Estate planning, wealth transfer | High — automatically a MEC |

| 7-Pay | 7 years | Maximum funding speed without MEC | Moderate — at the MEC boundary |

| 10-Pay | 10 years | Infinite banking, cash value accumulation | Low |

| 15-Pay | 15 years | Balanced premium/cash value growth | Low |

| 20-Pay | 20 years | Lower premiums, long-term planning | Very Low |

| 30-Pay | 30 years | Most affordable limited pay option | Very Low |

| Paid Up at 65 | Until age 65 | Retirement planning, premium-free retirement | Very Low |

Single Premium Whole Life

Single premium life insurance involves funding an entire policy with one lump-sum payment, making it the shortest limited pay option available. The policy is immediately paid up from day one, providing leverage on your dollars and an income-tax-free death benefit. However, single premium whole life is automatically classified as a modified endowment contract (MEC), which means you lose the tax-free access to cash value through policy loans. This makes single premium best suited for estate planning and wealth transfer rather than cash value utilization strategies.

7-Pay Whole Life

The 7-Pay structure is significant because of the 7-pay test in the Internal Revenue Code (IRC 7702A), which determines whether a policy qualifies as cash value life insurance or becomes a MEC. Seven years is the shortest time frame you can choose to fully fund your policy without changing its tax treatment. This makes 7-Pay the fastest option for clients who want to maximize funding speed while preserving the ability to access cash value through tax-free policy loans.

10-Pay Whole Life Insurance

The 10-Pay is the most popular limited pay option, particularly for those practicing infinite banking with their policy. You can structure a 10-Pay with a term rider to increase death benefit coverage during the funding years while the whole life death benefit grows. After 10 years of premium payments, the policy is fully paid up and continues to grow through dividends and compounding.

The following sample 10-Pay rates are from an A+ rated carrier for a preferred plus male. Annual rates are for informational purposes only and must be qualified for.

| Age | $100,000 | $250,000 | $500,000 | $1,000,000 |

|---|---|---|---|---|

| 40 | $3,628 | $8,717 | $17,225 | $34,170 |

| 45 | $4,297 | $10,310 | $20,360 | $40,370 |

| 50 | $5,082 | $12,167 | $24,010 | $47,590 |

| 55 | $5,979 | $14,272 | $28,140 | $55,740 |

| 60 | $6,973 | $16,565 | $32,610 | $64,530 |

| 65 | $8,075 | $19,077 | $37,490 | $74,100 |

20-Pay Whole Life Policy

Another popular choice, the 20-Pay provides permanent life insurance coverage fully paid up in 20 years. The lower annual premium compared to a 10-Pay makes this accessible for clients who want the benefits of limited pay without the concentrated cash outlay. The 20-Pay is particularly well-suited for younger clients who want to be done paying premiums well before retirement.

The following sample 20-Pay rates are from an A+ rated carrier for a preferred plus male. Annual rates are for informational purposes only and must be qualified for.

| Age | $100,000 | $250,000 | $500,000 | $1,000,000 |

|---|---|---|---|---|

| 40 | $2,277 | $5,342 | $10,470 | $20,660 |

| 45 | $2,698 | $6,312 | $12,365 | $24,390 |

| 50 | $3,200 | $7,462 | $14,600 | $28,770 |

| 55 | $3,797 | $8,817 | $17,235 | $33,930 |

| 60 | $4,580 | $10,582 | $20,645 | $40,600 |

| 65 | $5,536 | $12,730 | $24,795 | $48,710 |

30-Pay Whole Life

The 30-Pay stretches premiums over three decades, resulting in the most affordable annual premium among limited pay options. The trade-off is a longer commitment period, but for clients starting in their 30s, this means being fully paid up by their 60s — well before or right at retirement.

Life Paid Up at 65

A limited pay policy to age 65 offers permanent coverage that becomes fully paid up at the traditional retirement age. The advantage is obvious: upon entering retirement, your life insurance premium obligation disappears, freeing up cash for other pursuits or expenses. In addition, your life insurance retirement plan is fully funded and can be used to supplement income in retirement through tax-free policy loans.

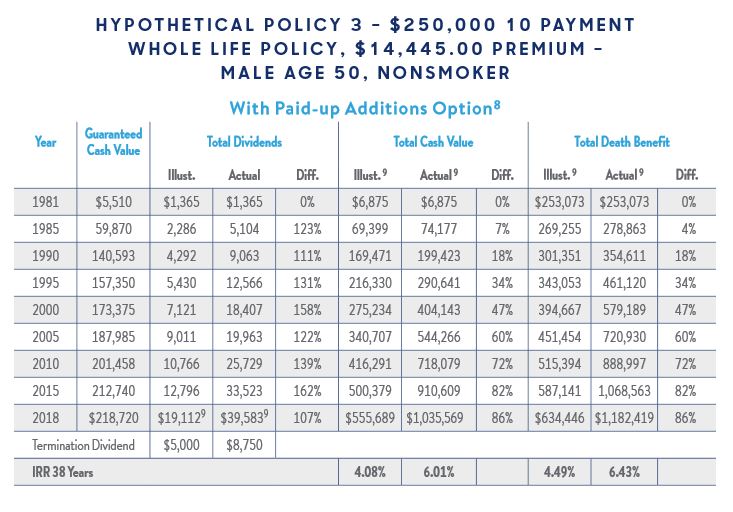

Real Policy Performance: 38-Year Case Study

The following chart shows a real-world performance example of a $250,000 10-Pay Whole Life Policy with a paid-up additions option, taken out in 1980 by a 50-year-old male nonsmoker with an annual premium of $14,445.

| Year | Guaranteed Cash Value | Total Dividends (Illustrated) | Total Dividends (Actual) | Total Cash Value (Illustrated) | Total Cash Value (Actual) | Total Death Benefit (Illustrated) | Total Death Benefit (Actual) |

|---|---|---|---|---|---|---|---|

| 1981 | $5,510 | $1,365 | $1,365 | $6,875 | $6,875 | $253,073 | $253,073 |

| 1985 | $59,870 | $2,286 | $5,104 | $69,399 | $74,177 | $269,255 | $278,863 |

| 1990 | $140,593 | $4,292 | $9,063 | $169,471 | $199,423 | $301,351 | $354,611 |

| 1995 | $157,350 | $5,430 | $12,566 | $216,330 | $290,641 | $343,053 | $461,120 |

| 2000 | $173,375 | $7,121 | $18,407 | $275,234 | $404,143 | $394,667 | $579,189 |

| 2005 | $187,985 | $9,011 | $19,963 | $340,707 | $544,266 | $451,454 | $720,930 |

| 2010 | $201,458 | $10,766 | $25,729 | $416,291 | $718,079 | $515,394 | $888,997 |

| 2015 | $212,740 | $12,796 | $33,523 | $500,379 | $910,609 | $587,141 | $1,068,563 |

| 2018 | $218,720 | $19,112 | $39,583 | $555,689 | $1,035,569 | $634,446 | $1,182,419 |

| IRR Over 38 Years | Illustrated: 4.08% | Actual: 6.01% | Cash Value IRR: 6.01% | Death Benefit IRR: 6.43% | ||||

This example demonstrates several important realities about limited pay whole life insurance. First, the actual performance exceeded the illustrated projections by 86% for both cash value and death benefit over 38 years — a testament to the compounding power of dividends reinvested as paid-up additions from a strong mutual company.

Second, the 38-year cash value internal rate of return was 6.01%, and the total IRR including the death benefit was 6.43%. Since the death benefit passes income-tax-free, a taxable investment would need to return approximately 8.5% (assuming a 25% tax rate) to match the after-tax equivalent. That context matters when evaluating the “lost opportunity cost” objection that critics of whole life insurance frequently raise.

Note that this is a historical policy from a major mutual carrier. While past performance does not guarantee future results, dividend-paying mutual companies have maintained their dividend scales through the Great Depression, the 2008 financial crisis, and every market disruption in between. That consistency is the point.

Advantages and Disadvantages of Limited Pay Life Insurance

| Advantages of Limited Pay Life Insurance | Disadvantages of Limited Pay Life Insurance |

|---|---|

| Predictable and guaranteed costs | Higher premiums in early years |

| Shorter premium payment term | Potential for Modified Endowment Contract |

| Faster cash value growth | Lost opportunity cost |

| Tax-deferred growth of cash value | Possible policy lapse if loans deplete cash value |

| Lifetime coverage | |

| Possible dividends (from mutual companies) | |

| Retirement income supplement via policy loans | |

| Living benefits (accelerated death benefit access) |

The Advantages in Detail

No more premiums after the payment period: Once you’ve completed your limited pay schedule, you own a fully paid-up life insurance policy. No further premiums are due, yet all the benefits of cash value life insurance remain in force — the death benefit, the dividends, and the ongoing tax-deferred growth.

Faster cash value accumulation: Limited pay whole life is a powerful way to supercharge your policy’s cash value growth in the early years. For those looking to use life insurance as a personal bank, having cash value grow quickly is essential — it gives you a larger pool to borrow against sooner.

Increased internal rate of return (IRR): Limited pay policies often produce a better internal rate of return compared to ordinary whole life paid to age 100. Once the policy is paid up, many of the fees associated with it are no longer assessed, providing a higher return dollar for dollar.

Long-term care access: Many limited pay policies provide a long-term care or chronic illness rider that allows you to access the death benefit during your lifetime if you qualify. This dual-purpose functionality — life insurance protection plus long-term care coverage — is one of the most underappreciated benefits of properly designed whole life insurance.

Excellent for children: Limited pay whole life insurance for children is a way to provide for your kids well into the future. A parent can pay into a 10-Pay or 20-Pay policy and give their child a fully paid-up whole life policy — with decades of compounding ahead — before the child even reaches adulthood.

The Disadvantages — With Context

Higher premiums: Limited pay life insurance requires compressing what would normally be a lifetime of payments into 7, 10, 15, or 20 years. The annual premium is higher than ordinary whole life to age 100 as a result. However, you can adjust the initial death benefit amount to fit your budget, and you can structure the policy so the majority of your premium goes toward paid-up additions. Over time, dividends used to purchase additional paid-up insurance will grow both the cash value and death benefit well beyond the initial face amount.

Modified Endowment Contract (MEC) risk: It is possible to MEC your policy with limited pay whole life, particularly with single premium and 7-Pay structures or those funded aggressively with paid-up additions. If your policy becomes a MEC, you lose the ability to access cash value tax-free through policy loans. The good news is that the insurance carrier and your agent can help you determine your MEC limit, and the carrier will alert you if you approach it.

Policy Design: Why Structure Matters More Than Payment Schedule

Most articles about limited pay life insurance focus on the payment schedule — 10-Pay vs. 20-Pay vs. paid up at 65. That’s a secondary decision. The primary decision is how the policy is designed.

A limited pay whole life policy can be structured in two fundamentally different ways:

Design A — Death Benefit Maximization: Higher base premium, smaller or no PUA rider. The policy prioritizes death benefit from day one. Cash value grows slowly in the early years. This is what most insurance companies default to if you don’t specify otherwise.

Design B — Cash Value Optimization: Minimum base premium allowable under MEC rules, maximum PUA rider. The policy prioritizes cash value accumulation from day one. The death benefit starts lower but grows substantially over time through dividends and paid-up additions.

For clients using limited pay whole life as a wealth-building tool — for infinite banking, for retirement supplementation, for generational wealth transfer — Design B is the approach that makes the strategy work. The payment schedule (10-Pay, 20-Pay, etc.) is just the timeline. The design is the engine.

This is why working with an independent agent who specializes in dividend-paying whole life insurance matters. A properly designed policy from the right carrier can mean six figures of difference in cash value over the life of the policy.

Limited Pay Life Insurance vs. Other Types of Life Insurance

Limited Pay vs. Traditional Whole Life

With a traditional whole life insurance policy, premiums are due until age 100 (older designs) or age 121 (newer designs). With limited pay, premiums are compressed into a shorter window — but the coverage is identical once both policies are paid up. The trade-off is higher annual premiums during the funding period in exchange for no premiums after the limited pay period ends. For clients approaching retirement, limited pay eliminates the burden of ongoing premiums on a fixed income.

Limited Pay vs. Term Life

Limited pay whole life differs from term life in a fundamental way: when a term policy ends, coverage stops entirely. You must renew at a higher rate, convert to permanent coverage, or go without protection. With limited pay, once the payment period ends, coverage continues for the rest of your lifetime with no further action required.

Limited Pay vs. Universal Life Insurance

Universal life offers a death benefit and cash value with flexible premiums, but it comes with market risk (for indexed or variable versions) and no guarantees on the rate of return. Whole life insurance — including limited pay — provides guaranteed cash value growth, guaranteed premiums, and a guaranteed death benefit. Universal life may offer more premium flexibility, but limited pay whole life offers more certainty.

Riders and Additional Coverage Options

Paid-Up Additions Rider: The most important rider for cash value optimization. This rider allows you to direct dividends back into the policy to purchase additional paid-up insurance, compounding your cash value and death benefit year after year. Not all carriers offer dividends, so choosing a dividend-paying whole life company is essential.

Accelerated Death Benefit Rider: Also known as living benefits, this rider allows you to access a portion of the death benefit during your lifetime if you are diagnosed with a qualifying terminal, chronic, or critical illness.

Waiver of Premium Rider: If you suffer a total disability, this rider pays all insurance premiums owed to the carrier on your behalf. Your premium is waived while the insurance company pays your tab — keeping your policy in force and your cash value growing even when you can’t work.

Family Insurance Rider: This rider allows you to add term coverage for your spouse and/or children at a fraction of what separate policies would cost.

How to Choose the Right Limited Pay Policy

Choosing the right limited pay life insurance policy comes down to four factors:

1. Company type: Choose a mutual insurance company with a strong dividend history. Stock companies exist to maximize shareholder value. Mutual companies exist to maximize policyholder value. That structural difference shows up in your dividends, your cash value growth, and your long-term returns. All four companies we recommend above are mutual companies or subsidiaries of mutual companies.

2. Policy design: Make sure the policy is designed with a paid-up additions rider and structured for cash value optimization — not death benefit maximization. Ask your agent to show you side-by-side illustrations of the same policy with different base/PUA splits.

3. Payment schedule alignment: Choose the payment schedule that aligns with your income and timeline. If you’re 10 years from retirement, a 10-Pay policy means you’ll be premium-free when you stop working. If you’re 25 years out, a 20-Pay or paid-up-at-65 structure may make more sense.

4. Loan recognition type: For clients planning to use policy loans (for infinite banking or other strategies), understand whether the company practices direct recognition or non-direct recognition. Non-direct recognition means your dividend is not affected by outstanding loans — an important factor for active banking strategies.

Is Limited Pay Life Insurance Right for Your Situation?

Limited pay policies are not ideal for everyone. Before choosing between 7-Pay, 10-Pay, or traditional whole life, get personalized guidance from our independent advisory team to find the strategy that maximizes your cash value potential.

Schedule your complimentary 30-minute limited pay analysis and discover the most efficient way to build cash value through life insurance.

No obligation. No sales pressure. Just honest guidance to help you determine if limited pay life insurance aligns with your long-term financial strategy.

Frequently Asked Questions

What is the best limited pay life insurance policy length?

The 10-Pay is the most popular option, particularly for clients using whole life insurance for infinite banking or cash value accumulation. It strikes the best balance between funding speed and premium affordability. However, the “best” length depends on your specific income, timeline, and goals. A 20-Pay may be more appropriate for younger clients or those who prefer lower annual premiums spread over a longer period.

Can limited pay life insurance become a Modified Endowment Contract?

Yes. Single premium whole life is automatically a MEC. For 7-Pay and other limited pay structures with aggressive paid-up additions funding, MEC risk exists. The insurance carrier and your agent can calculate your MEC limit, and the carrier will alert you if your policy approaches the threshold. Staying below the MEC limit preserves your ability to access cash value through tax-free policy loans.

How much does 10-Pay whole life insurance cost?

Sample rates vary by age, health class, and death benefit amount. For a preferred plus male at age 40, a $500,000 10-Pay policy runs approximately $17,225 per year. At age 50, the same coverage costs approximately $24,010 per year. These are base rates — a policy structured with paid-up additions will have different premium allocations depending on the design.

Is limited pay life insurance good for infinite banking?

Yes — limited pay whole life insurance is one of the most popular structures for infinite banking and personal banking strategies. The accelerated cash value growth from compressed premium payments gives you a larger pool to borrow against sooner. The key is designing the policy with a paid-up additions rider for cash value optimization, not just selecting a limited pay schedule.

Can you borrow against a limited pay life insurance policy?

Yes. You can borrow against your cash value at any time, for any purpose — supplementing retirement income, making purchases, funding a business, or any other need. Policy loans do not require credit checks or approval because you are borrowing against your own cash value. Any unpaid loan balance at the time of the insured’s death will be deducted from the death benefit before it is paid to beneficiaries.

What happens if I can’t afford premiums during the limited pay period?

Most limited pay whole life policies offer flexibility if your financial situation changes. Options may include using accumulated cash value to cover premiums through automatic premium loans, converting to a reduced paid-up policy with a lower death benefit but no further premiums, or exercising the extended term insurance option. A high cash value policy designed with paid-up additions provides the most flexibility because the cash value can sustain the policy through temporary payment gaps.

Is limited pay whole life better than whole life to age 100?

Not necessarily. A whole life to age 100 (or 121) policy structured with a heavy paid-up additions rider can produce excellent cash value growth — sometimes comparable to or better than a limited pay structure, depending on the carrier and design. The advantage of limited pay is the elimination of premium obligations after the payment period. The advantage of whole life to 100 is lower annual premiums with the flexibility to adjust PUA contributions year to year. The best choice depends on your cash flow, goals, and whether premium elimination by a specific date matters to you.

Is limited pay life insurance a good investment?

Limited pay whole life insurance is not an “investment” in the traditional sense — it’s a financial instrument that provides a guaranteed return on cash value, tax-deferred growth, income-tax-free death benefit, and access to cash through policy loans. When designed properly with paid-up additions from a strong mutual company, the long-term internal rate of return can exceed 5-6% on a tax-equivalent basis. The real value is in the combination of guarantees, tax advantages, liquidity, and death benefit protection — a package no single investment can replicate.

13 comments

Patrick

Are any of these Dividend Paying Whole of Life policies available in the UK?

Henry Riano

whole life for 10 years please sends me the information

male born in 1952.

thanks

Insurance&Estates

Hello Henry, if you would like information go ahead and request a call from Barry Brooksby at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Bez danie

Which one is better? Limited Permium pay up to age 23 for kids and up to age 68 for adults or premium pay up to age 121.

Age kids 7 and 10, adults 33 and 43

Thank you

Insurance&Estates

Hello, the best thing to do is get some real numbers by connecting with our limited pay expert Barry Brooksby. You can connect with him directly at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Samantha

Hey , can someone contact me to go over the different companies and decide the best fit for whole life insurance for me .

Thanks 😊

Insurance&Estates

Hello Samantha, I suggest you check in with Barry Brooksby to get started. You can connect with him at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Agatha Stratourides

Please send me lowest quotes for Lafayette 10-yr. limited pay whole life insurance with PUAs for 30-yr. old woman standard and preferred rates to my email only.

Insurance&Estates

Hello Agatha, we’ve passed your request to one of our Pro Client guides. If you haven’t yet connected, reach out to barry@insuranceandestates.com.

Best, I&E

Lydia Spicer

Send me lowest quotes for Lafayette whole life insurance for 58 yr old male and 54 yr old woman to my email only. Do not call me.

Insurance&Estates

Hi Lydia,

Thank you for stopping by. We hope you are finding the site informative.

We will send you an email from @insuranceandestates.com. Please keep an eye out for it.

Sincerely,

I&E

George

I am going to purchase life insurance. I am going with a term policy, but I am contemplating if I should go with a whole life policy, I could convert into a whole life before the term expires, but in the long run, would it be cheaper to get whole life right away?

I&E

Make sure the company you are contracting with for term life offers whole life conversions. Certain whole life companies are going to have far superior options than others so you might want to take that into consideration when choosing your term life company.

It will be cheaper to get whole life right away rather than waiting 10 years or more down the road primarily due to the premium payment difference going up significantly once you reach 40. Term is cheap while you are young but gets more and more pricey as you age. If you lock into a whole life policy now you pay a lower premium. Plus, you can choose a limited pay policy and not have to make premium payments later.

One question you need to ask is, “am I going to live 20-30 more years or am I going to outlive my term policy?” Whole life is the optimists life insurance policy because you know you are going to live well into your 90s so having a policy that builds cash value and lasts your whole life is the far better choice. Unless of course, you die young.