You’ve heard about infinite banking. Now you want to know: is it actually worth it?

This is the honest breakdown — every real advantage and every real limitation of the Infinite Banking Concept (IBC), drawn from our experience designing 1,000+ policies since 2017. No hype, no sugarcoating, no sales pitch disguised as education.

New to infinite banking? Start with our complete guide to understand how it works before evaluating whether it’s right for you.

TL;DR — Should You Do Infinite Banking?

Infinite banking has real, measurable advantages — but it also has real costs and limitations that most advocates gloss over. Here’s the honest evaluation:

- 10 pros: Non-correlated asset, tax-free access, uninterrupted compounding, guaranteed growth, death benefit leverage, creditor protection, privacy, and more

- 7 cons: Minimum ~$500/month commitment, 4-7 year funding lag, mandatory premiums, discipline required, health qualification, creditor protection variances, single-asset-class concentration

- The deciding factor: 90% of IBC “failures” trace back to poor policy design — not problems with the concept itself

- Best for: Disciplined individuals with stable income, a 7+ year horizon, and a desire to control the banking function in their financial life

- Not for: Anyone who needs every dollar liquid right now, can’t commit $500+/month consistently, or expects stock-market-beating returns from a life insurance policy

Bottom Line: If you have the cash flow, the timeline, and the discipline, infinite banking is one of the most powerful financial strategies available. If you don’t, it will frustrate you. This guide helps you decide which camp you’re in.

Why Trust This Guide

This article is written and maintained by the team at Insurance & Estates — ranked the #1 life insurance agency on Trustpilot with 280+ verified reviews. Our team brings 70+ years of combined experience in estate planning, financial services, and infinite banking policy design. Since 2017, we’ve designed and implemented 1,000+ IBC policies as independent brokers (not captive agents), giving us access to every major mutual carrier. We practice what we teach — our advisors use infinite banking in their own financial lives.

Watch: Infinite Banking Pros and Cons (39 min)

Before you dive into the written breakdown below, this video walks through the same evaluation framework — with policy design examples, real client scenarios, and the nuances that don’t always come through in print. If you absorb information better by watching than reading, start here. The article below covers the same ground in depth and serves as your reference once you’ve seen the bigger picture.

Table of Contents

- Infinite Banking vs Traditional Banking vs 401(k)

- Pros of the Infinite Banking Concept

- Cons of the Infinite Banking Concept

- Next Steps

- Frequently Asked Questions

Infinite Banking vs Traditional Banking vs 401(k)

The Infinite Banking Concept uses dividend-paying whole life insurance as a personal banking system. For a complete explanation of how it works, see our infinite banking guide.

The comparison below shows why practitioners choose to store capital in whole life insurance rather than a bank account or retirement plan — and where each option falls short.

| Feature | Infinite Banking | Bank Savings | 401(k) |

|---|---|---|---|

| Tax-Free Growth | ✅ Yes | ❌ No | ⚠️ Tax-Deferred |

| Tax-Free Access | ✅ Via Policy Loans | ❌ Interest Taxed | ❌ Taxed + Penalties Before 59½ |

| Guaranteed Growth | ✅ Contractual | ⚠️ Near 0% | ❌ Market Risk |

| Creditor Protection | ✅ Most States | ❌ Limited | ✅ ERISA Protected |

| Death Benefit | ✅ Tax-Free | ❌ None | ❌ Taxable to Heirs |

| Access Without Penalty | ✅ Any Time | ✅ Any Time | ❌ Before 59½ |

| Uninterrupted Compounding | ✅ Even While Borrowing | ❌ Withdrawals Stop Growth | ❌ Withdrawals Stop Growth |

| Privacy | ✅ Not on Credit Reports | ❌ Visible in Asset Searches | ❌ Reported to IRS |

| Best For | Long-term wealth building, tax-free liquidity, and financial control | Short-term emergency reserves | Employer-match contributions |

Individual results depend on policy design, carrier selection, and implementation discipline. Consult with a qualified professional before making financial decisions.

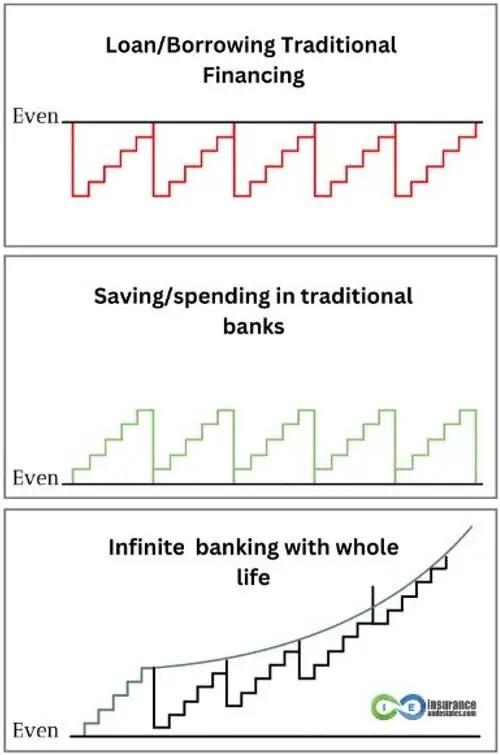

The visual below illustrates this difference in action — how traditional financing, conventional saving, and infinite banking each affect your wealth trajectory over time:

Traditional borrowing depletes your capital every time you finance a purchase. Saving through a bank interrupts compound growth with every withdrawal. Infinite banking keeps your cash value trajectory upward even during borrowing cycles — because you borrow against your policy rather than from it.

Pros of the Infinite Banking Concept

These are the ten advantages that matter most — each one we’ve seen play out firsthand as practitioners and across the clients we’ve served since 2017.

1. Non-Correlated Asset

Whole life insurance doesn’t rise and fall with the stock market, real estate, or interest rate cycles. Your cash value receives guaranteed growth every single year regardless of economic conditions. This matters most during retirement — when markets drop 20-40%, the last thing you want is to draw income from a depleted portfolio. Your infinite banking policy gives you an alternative income source during downturns without forcing you to sell investments at a loss. It’s your financial foundation when everything else is shaking.

2. Improves Cash Flow and Liquidity

Compare accessing your policy’s cash value to accessing equity in real estate. To tap home equity, you need to qualify for a HELOC, get an appraisal, pass a credit check, and wait weeks. With your infinite banking policy, you call the insurance company and request a check. No qualifying, no appraisal, no credit check — funds arrive within days. Your cash value is a true liquid asset that delivers compound growth in a tax-advantaged environment while remaining accessible whenever you need it.

3. Personal Banking System

This is the core of the concept — you own and operate your own banking system. You borrow against your cash value, purchase assets or eliminate debt, use returns from those assets to repay your policy loan, and repeat the cycle indefinitely. The entire time, your full cash value balance keeps compounding through guaranteed returns and dividends. You control the terms, the timing, and the purpose of every transaction. For a full walkthrough of how to implement this, see our guide on becoming your own banker.

4. Tax-Advantaged Compound Interest

Your cash value grows in a true compound interest environment because gains accumulate tax-deferred year after year. Unlike a bank savings account where interest is taxed annually — reducing your compounding base every year — your policy’s growth compounds on the full balance untouched by the IRS. And when you need access to your money, you take tax-free policy loans rather than taxable withdrawals, keeping your principal and compounding engine fully intact. Properly managed, you can use this structure for life without ever triggering a taxable event on the growth.

5. Leverage Through Death Benefit

From day one, your policy provides a tax-free death benefit that can be many multiples of what you’ve contributed. While the death benefit isn’t the primary focus of infinite banking, it provides immediate leverage — peace of mind that your family is protected if something happens to you. And unlike term insurance that expires, your death benefit grows over time as dividends purchase additional paid-up insurance. The older you get, the larger the legacy you leave behind.

6. Tax-Deferred Dividend Growth

Beyond guaranteed cash value growth, your policy earns dividends from the mutual insurance company’s profits. While dividends aren’t guaranteed, the top mutual carriers we recommend have paid dividends every single year for over a century — through the Great Depression, world wars, and every financial crisis in between. When you use dividends to purchase additional paid-up insurance, they compound on top of your existing cash value, accelerating both your accessible capital and your death benefit simultaneously.

7. Tax-Free Access to Cash Value

You access your cash value through policy loans that are tax-free, require no credit check, don’t appear on your credit report, and have no mandatory repayment schedule. You set the terms. Unlike 401(k) withdrawals that trigger taxes and penalties before 59½, policy loans carry none of that. Your entire cash value — including the portion used as collateral — keeps growing tax-deferred while you use the loan proceeds however you choose. This is what makes the banking function truly “infinite.”

8. Guarantees

Whole life insurance is the only financial vehicle that provides all four of these contractual guarantees simultaneously: guaranteed cash value accumulation, guaranteed death benefit, guaranteed fixed premiums, and a guaranteed minimum interest rate. No market-based investment offers this. When your money earns a guaranteed return year after year, it eliminates the pressure to rush into potentially bad investments — you can wait for the right opportunities because your foundation is already growing with certainty.

9. Privacy

In an era where nearly every financial transaction is tracked and reported, whole life insurance stands apart. Your policy’s cash value doesn’t appear on credit reports, asset searches, or standard financial disclosures. Policy loans remain completely private — between you and your insurance company. No bank reporting, no credit score impact, no public record. For business owners, professionals, and anyone who values financial discretion, this level of privacy is a significant and often overlooked advantage.

10. Creditor Protection

Many states provide substantial creditor protection for life insurance cash values — and several offer unlimited protection. If you face financial difficulty, a lawsuit, or a judgment, your policy’s cash value may be sheltered from creditors depending on your state’s laws. This makes whole life insurance not just a growth vehicle but a protective one — particularly valuable for business owners, physicians, real estate investors, and anyone with elevated liability exposure. The level of protection varies by state, so see Con #3 below and our state-by-state guide for specifics.

Key Takeaway — Pros of Infinite Banking

Infinite banking combines benefits that no single traditional financial product can match: guaranteed tax-deferred growth, tax-free access through policy loans, uninterrupted compounding even while borrowing, a growing death benefit, creditor protection, and complete privacy. The most impactful advantage is what practitioners call the “two places at once” mechanism: when you take a policy loan, you’re not withdrawing your cash value — you’re borrowing against it as collateral. Your full cash value keeps compounding inside the policy while the loan proceeds simultaneously fund real estate, business growth, debt elimination, or other opportunities outside the policy. Your dollar does two jobs at the same time.

Cons of the Infinite Banking Concept

We believe honesty about the downsides builds more trust than overselling. These are the real limitations you need to understand before implementing infinite banking — drawn from our experience working with 1,000+ clients since 2017.

1. Cost Prohibitive for Some

Infinite banking requires a meaningful financial commitment — we recommend a minimum of approximately $500/month or 10% of your gross income, whichever is greater. That’s a real barrier for many households. The good news: most people have more capacity than they realize. Our team specializes in identifying “hidden money” — unnecessarily high insurance premiums, inefficient debt structures, or spending patterns that can be redirected without dramatic lifestyle changes. But if you’re stretched thin with no margin, this isn’t the right time to start. Build your financial foundation first.

2. Mandatory Annual Payments

Your policy requires premium payments to stay in force — there’s no way around this. However, a properly designed infinite banking policy builds in flexibility. The required base premium is only 10-20% of your total contribution, while the remaining 80-90% goes toward paid-up additions, which are optional. In practice, your required monthly payment might be just $200 while your full funding target is $1,000. When money is tight, you pay the minimum. When cash flow improves, you fund the full amount. This built-in flexibility is a critical design feature most people don’t know about.

3. Creditor Protection Variances

As noted in Pro #10, creditor protection for life insurance cash value is one of the strongest reasons to own a policy — but the protection isn’t uniform across the country. Some states (Florida and Texas, for example) provide unlimited protection of cash values from creditors and judgments. Others offer partial protection. A few offer little to none. This is a meaningful consideration if you live in a state with weak protections. The silver lining: if you move to a state with stronger protections, you’re generally granted that state’s protections going forward — so a relocation can substantially upgrade your asset protection posture. Consult with an attorney in your state for specifics.

4. Requires Discipline

Nelson Nash said you must be an “honest banker.” That means borrowing against your policy AND paying it back. If you treat your cash value like a piggy bank — borrowing without repaying — you’ll slow the compounding engine and undermine the entire strategy. Infinite banking rewards discipline and punishes carelessness. The long-term growth of your policy depends on cycling loans through your system and recapitalizing your “bank” after each use. This isn’t a set-it-and-forget-it strategy — it requires active participation in your financial life.

5. You Have to Qualify

Infinite banking requires a whole life insurance policy, which means you must pass life insurance underwriting. If you have significant health issues, qualifying can be harder or more expensive. One workaround: you can purchase policies on children or grandchildren and teach them infinite banking principles — building the system for the next generation even if your own health limits your options.

6. Funding Lag Time

This is the con that frustrates people most. When you start an infinite banking policy, your accessible cash value will be less than your total contributions for the first several years. Depending on policy design, the break-even point — where cash value equals or exceeds premiums paid — typically falls between years 4-7. If you need immediate access to 100% of every dollar you contribute, this strategy isn’t for you. But after the break-even point, growth accelerates significantly and the math works powerfully in your favor for decades.

7. Not Diversified (By Itself)

Putting substantial capital into a single asset class raises a valid concern. But here’s the reframe: infinite banking isn’t an investment — it’s financial infrastructure. The guaranteed elements (cash value growth, death benefit, fixed premiums) provide your stable foundation. The real diversification happens at the next level — when you use policy loans to acquire real estate, fund business ventures, purchase dividend-paying stocks, or eliminate high-interest debt. You’re not breaking the diversification rule. You’re applying it at a higher level with a guaranteed base underneath everything.

Key Takeaway — Cons of Infinite Banking

The most significant drawbacks of infinite banking are the upfront cost commitment (minimum ~$500/month), the 4-7 year funding lag before break-even, and the discipline required to repay policy loans consistently. These aren’t dealbreakers — they’re the price of building a banking system you control. Based on our experience, 90% of “failures” with infinite banking trace back to poor policy design rather than problems with the concept itself. Working with a specialist who understands proper policy structuring eliminates most of these risks.

⚡ Beyond Infinite Banking: Volume-Based Banking

If conventional financial advice has left you sensing something’s missing, infinite banking is the foundation — but it’s not the ceiling.

Most financial planning obsesses over rate of return. A 7% return on $50,000 produces $3,500. A 5% return on $500,000 produces $25,000. Same person, radically different financial life — and the difference isn’t rate, it’s volume.

Volume-Based Banking is the framework our team developed for engineering more capital through your banking system in a tax-advantaged environment. It’s not a different product. It’s a different question. Instead of “what’s my return?” the question becomes “how much of my income is moving through a structure I control?” That shift is what separates practitioners building generational wealth from those treating whole life as a savings account with extra steps.

Next Steps

Get Your Personalized Infinite Banking Illustration

Before committing to any strategy, see what the numbers look like for your situation — not a hypothetical case study. Our Pro Client Guides will build a custom illustration around your age, health, income, and goals.

- Custom Illustration: See your projected cash value, death benefit, and loan capacity year by year

- Side-by-Side Comparison: IBC vs your current strategy — 401(k), savings, real estate equity

- Honest Assessment: Whether infinite banking fits your timeline and financial situation

- Lifetime Coaching: Ongoing guidance to optimize your banking system as your situation evolves

- No Obligation: Complimentary session with zero pressure to purchase

Schedule Your Free Strategy Session →

One illustration with your own data is worth more than a hundred articles. — Steve Gibbs, Estate Planning Attorney & Author of The Ultimate Asset

About the Authors

Barry Brooksby — Authorized Nelson Nash Infinite Banking Practitioner, real estate strategist, and author of Live Rich Die Rich. 25+ years in financial services. Barry has designed and implemented over 1,000 IBC policies and personally uses infinite banking to fund real estate investments. Creator of the Amazing Life Agent program.

Steve Gibbs, JD, AEP® — Estate planning attorney, Co-Founder of Insurance & Estates, and author of The Ultimate Asset. 15+ years in trusts, estates, and asset protection law across CA, FL, and MN. Steve brings a legal and wealth-transfer perspective to infinite banking that most insurance-only practitioners lack.

Together, Barry and Steve lead the team at Insurance & Estates — ranked #1 life insurance agency on Trustpilot with 280+ verified reviews.

Frequently Asked Questions

Looking for basics? Our infinite banking guide covers what IBC is, how it works, and whether it’s a scam. Below are the evaluation-specific questions.

Is infinite banking a scam?

No. Infinite banking is a legitimate financial strategy built on dividend-paying whole life insurance — a 160+ year-old product issued by some of the most heavily regulated and conservatively managed financial institutions in the country. The mechanism (borrowing against cash value via policy loans while the full balance continues compounding) is contractually defined in every policy and is the same mechanism corporations and ultra-wealthy families have used for generations. What can be a scam is bad implementation: agents who sell improperly structured policies, oversell expected returns, or push the strategy on clients who shouldn’t have it. The concept is sound. The execution is where most criticism legitimately lands. For a deeper look at common criticisms and how they hold up under scrutiny, see our complete infinite banking guide.

Is infinite banking only for wealthy people?

No. While infinite banking does require consistent funding — we recommend a minimum of around $500/month — it’s not reserved for the wealthy. Many of our clients are middle-income professionals, business owners, and families who redirect existing cash flow rather than finding “new” money. The strategy actually levels the playing field by giving individuals access to the same banking mechanics that corporations and wealthy families have used for over a century. You don’t need to be rich to start. You need stable income, financial discipline, and a long-term perspective.

How much does infinite banking cost?

Most infinite banking policies start at approximately $500/month, though the ideal funding level is around 10-25% of your gross income. The cost depends on your age, health classification, and how aggressively you want to build cash value. Unlike a gym membership or subscription, every dollar of premium builds equity in an asset you own — it’s not an expense that disappears. A 35-year-old male in good health might pay $1,000/month for a $500,000 policy designed for maximum cash value. Our team can show you exactly what the numbers look like for your specific situation with a free custom illustration.

What’s the difference between infinite banking and velocity banking?

They’re completely different strategies that solve different problems. Infinite banking uses whole life insurance to build a permanent, tax-advantaged banking system you control. Velocity banking uses a HELOC (Home Equity Line of Credit) to accelerate debt payoff — primarily your mortgage. Velocity banking is a short-term debt elimination tactic dependent on variable interest rates and lender approval. Infinite banking is a long-term wealth-building system with contractual guarantees and no third-party gatekeepers. Some practitioners use both — eliminating debt with velocity banking while building their IBC policy simultaneously. For a full comparison, see our guide on infinite banking vs velocity banking.

How does infinite banking fit with my 401(k)?

Think complement, not replacement. If your employer offers a 401(k) match, take it — that’s an immediate 100% return. But recognize the 401(k)’s limitations: you can’t access funds before 59½ without penalties, you’re forced into distributions at 73, and every withdrawal is taxed as ordinary income. Your infinite banking policy has none of those restrictions — tax-free access anytime, no required distributions, complete flexibility. The strongest practitioners we work with max out their employer match in the 401(k), then direct additional savings into their banking policy. You get the upfront tax deduction from the 401(k) plus tax-free access and guarantees from whole life.

Can I do infinite banking with an IUL instead of whole life?

Technically yes, but we generally recommend whole life for infinite banking. Indexed Universal Life (IUL) policies tie cash value growth to a market index, which introduces variability that whole life doesn’t have. Whole life provides guaranteed minimums, guaranteed fixed premiums, and a 160+ year track record of dividend payments from mutual carriers. IULs can offer higher potential upside but come with caps, floors, and cost-of-insurance increases that can erode performance over time. For some clients, an IUL component makes sense alongside a whole life foundation. For a detailed breakdown, see our comparison of IUL vs whole life insurance.

How much money do I need to start infinite banking?

You can start an infinite banking policy with as little as $500/month, though higher funding levels produce better efficiency. The real question isn’t the minimum — it’s what you can commit to consistently for 7+ years. Based on our experience with 1,000+ implementations, clients who fund at 10-25% of gross income see the strongest results. You can also add a lump sum upfront to accelerate early cash value growth. Nelson Nash advocated the goal of eventually having your annual premium equal your annual income — but that’s a long-term target, not a starting requirement.

What happens to my money if the market crashes?

This is where infinite banking shines. Your cash value grows regardless of what the stock market does — you receive guaranteed increases every year no matter what’s happening in the economy. The top mutual companies we recommend maintained their dividend payments through the Great Depression, the 2008 financial crisis, and COVID. When credit markets froze in 2008 and banks stopped lending, policyholders could still access their cash value through policy loans — no credit check, no approval process. Even better, recessions create buying opportunities. While others panic-sell at the bottom, you have liquid capital ready to deploy into undervalued assets.

What if the insurance company goes under?

The risk is extraordinarily low — but the answer is more nuanced than most articles let on. State guaranty associations do provide a backstop, typically $100,000 to $300,000 in cash value protection per insured. For a properly funded infinite banking policy held for 20+ years, your cash value will likely exceed those caps — so guaranty associations alone aren’t your primary protection. Your real protection comes from carrier selection. The mutual companies we recommend have AM Best ratings of A or higher, conservative investment portfolios subject to strict state regulation, capital reserves significantly exceeding required minimums, and dividend payment histories spanning more than a century — through the Great Depression, both World Wars, the 2008 financial crisis, and COVID. When carriers do face trouble, state regulators rarely allow outright failure; they facilitate takeovers by stronger companies so policies continue uninterrupted. The combination of conservative carrier selection plus the regulatory framework — not the guaranty association cap — is what makes the carrier-failure risk genuinely small. For specifics on which carriers we recommend and why, see our guide to the top 10 best infinite banking companies.

Can I convert my existing whole life policy to infinite banking?

You typically can’t “convert” an existing policy directly, but you have several options. First, check if your current policy allows adding a paid-up additions rider — this lets you direct more premium toward cash value growth. Second, consider a 1035 exchange, which transfers your existing cash value into a new policy properly structured for infinite banking — completely tax-free. Third, keep your existing policy for what it is and start a new infinite banking policy alongside it. The right path depends on your current policy details, age, health, and goals — this is exactly the kind of situation where working with a specialist makes a significant difference.

What happens to my infinite banking policy when I die?

Your beneficiaries receive the full death benefit minus any outstanding policy loans — completely income tax-free. If you’ve been practicing infinite banking properly and repaying loans, your death benefit will have grown substantially over your lifetime through dividends and paid-up additions. Many practitioners use the death benefit as a wealth transfer tool, funding the next generation’s infinite banking policies or providing a tax-free inheritance. With proper estate planning, your banking system can continue benefiting your family for generations.

56 comments

Jay Ram

Amazing articles here. My wife and I learned about Infinite Banking and were VERY dubious at first. But after extensive research, we are certain this is perfect for our needs. Who would I reach out to for more info? I’ve tried contacting through the info@ email address a couple of times but haven’t gotten a reply. Glad I found your site with all these great articles on Infinite Banking and hope to speak soon.

Steven Gibbs

Hello Jay and thanks for connecting! Go ahead and reach out to Barry Brooksby by requesting a call at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Steven Gibbs is a licensed insurance agent, and the following agent

license numbers of Steven Gibbs are provided as required by state law:

Resident License; AZ agent #17508301,

Non-resident Licenses: TX agent #2273189, CA agent #0K10610,

LA agent #769583, MA agent #2049963, MN agent #40563357,

UT agent #655544.

Bwhite

I don’t see the part about direct and non direct recognition. Wouldn’t non direct work better with policy loans? Especially if there are multiple loans over time? Love some feedback.

SJG

Direct vs non-direct recognition is debated amongst IBC professionals. Don’t think the question of multiple loans is a huge concern, though again this could be debatable. In my experience, non-direct carriers pay higher dividends on average so perhaps it evens out. I don’t think this is a major determining factor in selecting top companies.

Best, Steve Gibbs for I&E

Brent white

If in had 100k and borrowed 80k it seems like non direct recognition would make a significant difference. This is me just talking I do not the the exact answer. I really want to look at the numbers to see. I’m a big fan of guardian life insurance but I would love to see this compared to say a Lafayette life. Thank you for you incredible article. I’m going through the Nelson Nash Institute as we speak. See at the think tank!

Evelyn

Would it be smart to take a HELOC to pay debt first to have more cash available and then open a Wholelife insurance?

SJG

Hello Evelyn, this is a financial question that is tough to answer in a blog post setting without a better understanding of your financial picture. Alot could depend on the interest rate on the HELOC yet other concerns should also be factored in. Best to schedule a call with one of our pro-team members and a good start would be emailing Denise at denise@insuranceandestates.com.

Best, Steve Gibbs for I&E

Bryce

I’m interested in knowing more about infinite banking. Could I set up a meeting time to discuss it?

Insurance&Estates

Hello Bryce, if you haven’t yet connected with someone, go ahead and request a call from Barry Brooksby at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

UK Investor

Hi there. I noticed that all your products (and those online) pertaining to the IBC are US based. Are there any practitioners you are aware of or any information available of IBC implementation in the UK? I also noticed that you did not answer the question asked in your comments about this above. I(/we, your UK based readers) would appreciate your experienced view on this please. Thank you, in advance of course.

Insurance&Estates

Hello, we can offer products to overseas folks under certain conditions. To inquire further, go ahead and request a call with Barry Brooksby at barry@insuranceandestates.com if a team member hasn’t already reached out to you.

Best, Steve Gibbs for I&E

Jeffery Barker

I’m about to sell my home in Phoenix Arizona and move back to property that I own in Texas I was wondering how I would go about taking the proceeds from the sell of my house and investing in whole life insurance to start my own IBC and was wondering if you could reach out to me to get me in touch with someone in this area that I could talk to that would help me with the the money or the proceeds that I’m going to get an investing it into such a program

Insurance&Estates

Hello Jeffrey, if you’re talking about your primary home, you may be able to just take the proceeds and invest them in a policy if your homestead tax exemption applies. This can all be worked out in a zoom consultation. To start that process, go ahead and email our IBC expert Barry Brooksby to request a meeting at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Lance Daugharty

Good evening after reading your thorough report I would like to speak with Barry at his earliest convenience to get some verbal information on this matter. Thank you for your time.

Insurance&Estates

Hello Lance, thanks for connecting. If you haven’t yet received an email or call from Barry, go ahead and request a call by emailing him at barry@insuranceandestates.com.

Best, Steve Gibbs, Esq.

ify

Hello.

My husband and I are interested in opening accounts but need directions. Pls help.

Insurance&Estates

Hello, thanks for connecting. A great first step is to request a call with our IBC expert Barry Brooksby at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Troy Claiborne

I am interested in opening a whole life insurance policy.

Insurance&Estates

Hello Troy, thanks for connecting. To get started, go ahead and email Barry Brooksby to request a call at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Reasonable Check

What a novelty! An insurance advocate promoting the most expensive insurance policy out there. While some points about IBC are certainly valid, e.g., liquidity compared to other investment options like real estate and certain stock market investments, other concepts are skimmed over without much deliberation. How about where someone puts in $1k a month and you say, “At the end of year one, they would have nearly $10,000 in cash value available.”? Let’s say you’re not stretching and you’ve actually paid only $2k for the policy at that point. I’m a 35 male who pays less $500/year for a $500k (twice the value of your example’s policy) term policy. I take my $11.5k, including my $1.5k savings over whole life and invest where I see fit. If I plug that into an index fund where history tells me I’ll average 8% or better, accounting for boom AND bust years, and I have an account value of ~$12.5k. I’m now $2.5k ahead of your example. Sure, you’ll say, but it could also lose money and IBC using whole life is more secure with flexible loan options. My question is, how are AIG, Berkshire, Humana, Zurich and all the other insurance providers able to offer these plans with the interest gaining account balances? What devices do they use to make money with all those premiums? Seems to me like I saw a lot of them getting into some financial trouble with their investment selections sometime around 2007-08. I think they were called mortgaged-backed securities? If you give your money to those who then go and invest in the stock market (because the returns are much better than IBC), have you really safeguarded your money at all? I’d ask AIG customers how secure they felt before Uncle Sam stepped in and kept the company holding their “infinite bank” funds from going belly up. Also, you stated, “Consider that normal stock market returns are taxed around 20% or more.” This is only true for those investing for less than 1-year. You can’t just compare the least desirable aspects of the stock market with the most desirable of IBC and be considered impartial. Capital gains (gains on investments over 1 year) will limit the average person’s taxes to 15%, and that’s only for non-tax benefited, i.e., NOT 401k’s and IRA’s which both have tax benefits. Also left out that those yields you noted in whole life policies are likely non-guaranteed and the guaranteed yield on your accounts is probably closer to 1-2%, with the POTENTIAL to make 5-6%, which is still less than average annualized return of the stock market (8-10%). To those still reading this comment, I’m sorry for the long post, and please use an investment strategy other than IBC. Buy a term policy to protect your loved ones instead, or at least review other financial resources/forums where they are not trying to directly sell you the product/service being discussed.

Insurance&Estates

Dear Unreasonable Cynic, I am an estate planner first and have been advocating for permanent life insurance solutions for years and really not for the purpose of “selling products”. There is nothing original in your commentary – just typical trashing of insurance products with the end game of promoting Wall Street based investing. Worse part is, this isn’t constructive. Mutual whole life companies didn’t get in trouble in 2007-2008 and by the way, all of Wall Street was in trouble around that time, no? You’re even admitting here there are some valid points about IBC. I encourage you not to fall into the trap of advocating 1 size fits all solutions. Saying things like “buy a term policy to protect your loved ones…” How about for those who follow your advice until their term expires and health issues prohibit getting coverage? I’ve observed folks in this situation when life insurance is needed for liquidity. Your “by the numbers” attack approach lacks reasonableness. There is no one size fits all.

John

I hear a lot about the ibc concept but this is always from North American sources. Is there any information for those of us in the UK?

James

“loan money out to your own company,

charge your company interest,

then your company pays you for the use of your money,

your company can write off the interest,

you recoup the interest, which

you use to pay back your policy loan, and

you then repeat the process ad infinitum.”

When I get the interest from my own company, do I need to pay tax? If so, I need to charge much higher interest rate to my own company to pay back my life insurance company to break even.

Insurance&Estates

Hello James and thanks for commenting. The short answer is that you need to be careful when considering writing off interest from a policy loan to your company. Barry Brooksby can talk with you about this in detail and you can e-mail him at barry@insuranceandestates.com to request a call.

Best, Steve Gibbs for I&E

Bolu

Quick question:

Say I have a policy of $250,000 and a premium of $500 per month. After 12 months of contributions, I’d have contributed $6,000. Say I take loan of $10,000 against that policy,

1. Will it be possible to take a loan more than what I have contributed so far?

2. What will the repayment plan for the $10,000 loan be?

3. Am I at liberty to determine my repayment amount and duration?

4. Say I am paying back $1,050 over 10 months (principal & interest), does that mean I need to be paying $1,550 every month now, being Premium and repayment?

Looking forward to reading your answers.

Insurance&Estates

Hello and thanks for commenting. Your illustration is bit problematic because these policies include a base premium and paid up (cash) additions. The rate at which cash value builds varies between policies and companies, so an actual illustration would be required to meaningfully address how much of a loan you can take after 12 months. Generally though, you would NOT be able to borrow more than contributed in a 12 month period. The repayment plan on a policy loan is whatever you decide to pay back; however, we encourage folks to pay at least what they would be required to pay in a conventional loan. For a more specific look at this, I encourage you to check in with Barry Brooksby at barry@insuranceandestates.com and have an actual illustration prepared.

Best, Steve Gibbs, for I&E

Bolu

Thanks Steve.

I will reach out to Barry promptly.

Guy A

What if you are in your 60’s. Can you pay one large single premium and be up and running ?

Insurance&Estates

Hi Guy,

Paying one single premium creates a modified endowment contract, which is not ideal. Instead, paying into your policy over a number of years is usually the best route to take full advantage of the various life insurance tax benefits and incentives under the tax code.

Best,

I&E

Adolfo

So, what’s the advantage for someone age 66, retired, with a mixed portfolio of IRAs (traditional and Roth), real estate, and savings totaling roughly $1.8M?

Insurance&Estates

Hello Adolfo and thanks for your question. The advantage would be to create predictable estate growth through WL guarantees for at least a portion of your assets, to an extent not possible with IRAs AND creating tax advantages due to flexibility of policy cash value and option for policy loans AND due to non-taxed death benefit passing to heirs.

If you’re interested in exploring options in more detail and obtaining specific examples (scenarios) connect with Barry Brooksby at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Jc

Life insurance loans can be taxable. There are taxable events so every situation needs to be looked at carefully before doing this.

Insurance&Estates

Hello John, thanks for commenting. While I agree that every situation needs to be looked at, I’m not aware of one where a policy loan was taxable. This is simply a matter of the IRS definition of what constitutes income in my experience and if it is a “loan”…

Best, Steve Gibbs for I&E

Andrew

The possibility of being taxed on a life insurance loan is next to none. The IRS cannot charge taxes on debt. It is similar to the way you can perform a cash out refinance on your home and take money out of your home’s equity as debt that cannot be taxed

Thomas Major

I’m guessing the author mistakenly forgot to mention the pro related to paying simple interest on loans like home loans, versus giving a devil what typically can equal 100% interest fee on a 3.5% compound interest loan.

Insurance&Estates

Hi Thomas, excellent point and thanks for reading.

Best, I&E

Brian Terry

Would a 401 k plan borrowed against and repay loan – it’s also tax free and you are “paying yourself “Interest. The 401k account can be in a non market fund eg stable value bonds or money market to ensure no stick market volatility. There is zero cost with this , but no insurance or DB but there are other ways to cover that

Thanks

Insurance&Estates

Hello Brian, thanks for commenting. You can check out our article on 401k loans and withdrawals: https://www.insuranceandestates.com/401k-withdrawals-and-loans/

for a better idea on this as well as our article on policy loans: https://www.insuranceandestates.com/life-insurance-loans/. Point being, 401k loans come with many repayment conditions and thus are not what they’re cracked up to be. When you answer this, you might not be as concerned about replacing the DB given the “night and day” difference with policy loans which are entirely flexible and totally liquid. Just my opinion.

Best, Steve Gibbs for I&E

Phuoc

You say that IBC is independent from whole life insurance. OK. What other vehicle(s) could I utilize to implement this? Everything I read in the PROs except non-correlated asset I can achieve without using a whole life policy and non-correlated asset is a non-issue in terms of importance in the long run.

Insurance&Estates

Hello and thanks for commenting. It is our finding that whole life is the best vehicle for IBC due to its numerous attributes discussed in the article. When you’re mentioning another vehicle its unclear what you mean. If you’re aware of another asset that works better than whole life for IBC, we would be very interested to hear about it. As I’ve often said, think about whole life like a piece of real estate, with a minimum guaranteed return, plus likely dividends based upon 100+ years of history, plus tax free accumulation + liquidity + leverage. When you try to swap for other assets you run into unpredictability in terms of growth and costs.

Best, Steve Gibbs for I&E

Philip Battaglia

What is the difference of using whole life and IUL for this strategy and can you explain why one is better than the other.

Thanks

Insurance&Estates

Hello Philip, thanks for reading and commenting. This would be a small novella to answer in a blog post. I suggest connecting with Barry Brooksby who is our infinite banking expert at barry@insuranceandestates.com and we’ve asked him to reach out to you as well.

Best, Steve Gibbs for I&E

Terry Harrell

Hi.im Terry can i draw all my money out my 401k while I’m still working a 6 to 4 to invest in my bank

Insurance&Estates

Hello Terry, thanks for commenting. Withdrawal from a 401k is a taxable event and may be subject to a penalty if you’re a younger person. Still, there are cases where it makes sense to withdraw and this should be discussed in a confidential setting with an expert.

Best, I&E

Joel Garcia

when you pull all of your 401k out, it is taxable and usually penalized for up to 50%.

Joel G

SJG

Hello Joel, thanks for commenting. We actually do NOT recommend that people “pull out all of their 401ks”. That said, the actual tax ramifications would be the 10% penalty if you’re younger plus whatever the taxes are based upon your bracket. With this in mind, there are cases where it may be advisable to convert a portion of tax deferred assets now and pay taxes at current rates vs later when taxes may be higher. There is also the ongoing question of whether you want to pay taxes on the seed or the harvest. It’s common knowledge in the estate planning world that qualified accounts are extremely inflexible in older years. RMDs are required and often force retirees into higher tax brackets. I suggest that you ponder these truths because there is a widespread idea not ever touch your 401k. Where does this ardent conviction come from? I’ll let you speculate.

Best, Steve Gibbs for I&E

Steven Gibbs is a licensed insurance agent, and the following agent

license numbers of Steven Gibbs are provided as required by state law:

Resident License; AZ agent #17508301,

Non-resident Licenses: TX agent #2273189, CA agent #0K10610,

LA agent #769583, MA agent #2049963, MN agent #40563357,

UT agent #655544.

Paige

Could you explain when it would be beneficial to draw down a 401k and put into an IBC policy?

Insurance&Estates

Hello, thanks for inquiring. Reach out to one of our experts, Jason Herring, at jason@insuranceandestates.com and send a preferred phone contact and best time to call if you haven’t connected with him already.

Best,

I&E

kevin Gardiner

thanks team if i lived in the usa i would use your services

Dwayne

Need the information for estates planning.

mike z

Hello. I am xx male non smoker looking to set up a ten pay whole life participating life insurance. I intend to drop a term policy I have once this is set up. My timeline is to start drawing down my 401K @ 59.5 pay state and local taxes and invest xxxxx per year. I locked in my 401K balance in a fixed return investment currently xxxxx @2.5% . I’m planning to work till 67yrs I’m married 3 kids 5,7,14 yrs old, Spouse 54 homemaker . We are currently funding a indexed whole life policy for spouse xx per year with similar guaranteed returns and accessible cash value thru loans. I’m looking at your plan to offset xx year old son’s college costs in 4 or 5 years. Included in my 401K balance is about xx Roth funds 100% vested, over 5years old. I’m not ready to buy today but like to get info . Thanks Mike Z

Steven T

Hello Steve Gibbs,

Great videos!!! New business owner, also about to get my Realtors license (WA), yet still keep my Clark Kent as IT Lead in the Financial business space. I am also married, 21 yrs, w/ home technician (also new business owner) and three kids: 15,12 and 9. So I want to start with 3 UIL and 3 WLP (2 for me; 1 for wife) as my base contributing 12K -15k per year for each WLP and 5-7k per year for UIL. Afterward, would like to broker (seek my WA insurance lic.) – possibly a part of your team as I am with many clients to follow my lead. I want flexible premiums, best life benefits and riders as well as keep my fees minimal with dividends eventually paying ALL overhead. Please call me or send follow-up e-mail to inlikeu@hotmail to get started. Timeline to start: 11/30/18. Thank You in advance, Steve T

Insurance&Estates

Hello Steven!

Thanks for your enthusiastic feedback and interest in starting your planning and potentially working with our I&E Pro Client Guide team. Given your various interests, I’d like to have Jason Herring reach out to you. He is our most experienced Guide for IUL products and he works with new agents who are interested in affiliating. The catch is that he’s on a mission trip to Honduras right now so his response time won’t be as efficient as usual. I’ll pass your information to him and just ask that you give him some time to respond.

Best to you.

Steve Gibbs, Esq.

Jack Maverick

This is one of the few really coherent and illuminating articles that I’ve read on the subject of “infinite banking” – whoever scribbled it, great job.