Written in conjunction with Denise Boisvert, Debt Elimination Specialist | Author of Purpose Driven Wealth Plan

Most debt advice ends the same way: you grind through years of aggressive payments, and when you’re finally done, you have zero debt and zero assets. You’re back to square one — just older, and without any infrastructure to show for the effort.

This guide presents a fundamentally different approach. Instead of simply attacking debt until it’s gone, you redirect your debt payments into a properly structured whole life insurance policy that builds cash value while you systematically eliminate every balance. When your debt is gone, you don’t restart from zero — you have a functioning personal banking system, a growing tax-free asset, and a death benefit protecting your family. Every dollar you spent fighting debt also built wealth.

If that sounds too good to be true, consider this: 73% of Americans still die with debt, even after following conventional financial advice. The system most people are using doesn’t work. This one does — if you have the discipline and the right policy design.

TL;DR: Life Insurance Debt Elimination Strategy

- The problem: Conventional debt payoff strategies leave you at zero — no debt, but no assets either. You’ve spent years paying banks and have nothing to show for it.

- The strategy: Redirect excess debt payments into a high-cash-value whole life insurance policy. Use policy loans to systematically eliminate debts while cash value continues compounding.

- The result: All debt eliminated in 3-5 years AND a growing, tax-free banking system that funds future purchases, investments, and retirement.

- Real example: Client “Lenny” eliminated $30,000 in credit card debt across three cards using this exact approach — and kept the wealth-building infrastructure after the debt was gone.

- Who this is for: People with stable income who are currently over-paying debt but building zero wealth. You need positive cash flow margin (paying more than minimums) to redirect.

- Who this is NOT for: If you’re spending 100% of income on minimum payments with no margin, you need basic budgeting first. This strategy requires discretionary cash flow to redirect.

Bottom Line: This is wealth building disguised as debt elimination. When your debt is gone, you won’t be back at zero — you’ll have financial infrastructure that keeps working for decades.

Why Trust This Guide

This guide was developed by Denise Boisvert, a debt elimination specialist who has personally guided clients through this strategy for years — including the case study featured below. Denise is the author of Designing a DEBT-FREE LIFE, a comprehensive guide to using high-cash-value life insurance for financial freedom. The article was reviewed by the Insurance & Estates advisory team, which includes a licensed estate planning attorney, Authorized Infinite Banking Practitioners, and independent advisors with access to all major mutual carriers. We don’t sell debt consolidation products or earn referral fees from lenders. Our only recommendation is the strategy and policy design that actually works.

Table of Contents

- Why This Strategy Is Different From Everything Else

- The Debt Crisis: What You’re Actually Up Against

- How Borrowing From Life Insurance to Pay Off Debt Actually Works

- Real-World Case Study: Lenny’s $30,000 Credit Card Elimination

- The Minimum Payment Transition Strategy

- Life Insurance Debt Strategy vs. Conventional Approaches

- How Debt and Interest Work For or Against You

- You Can Beat the System By Becoming the System

- Creating Money Momentum in the Right Direction

- Why Whole Life Insurance Is the Right Vehicle

- What Happens After Your Debt Is Gone (This Is the Real Payoff)

- Should You Cash Out Life Insurance to Pay Off Debt?

- Properly Designing a Policy for Debt Elimination

- How to Fund Your Infinite Banking Policy

- Is Borrowing From Life Insurance to Pay Off Debt Right for You?

- Frequently Asked Questions

Why This Strategy Is Different From Everything Else

There are two ways to think about debt elimination. The conventional approach treats debt as a fire to extinguish — throw everything at it until it’s gone, then start building wealth from scratch. The approach we teach treats debt elimination as the first phase of a wealth-building system, where every payment serves double duty: eliminating a liability and funding an asset.

The difference isn’t just philosophical — it’s mathematical. When you pay $1,200/month directly to credit card companies, that money is gone forever. The bank earns the interest, and you get a zero balance. When you redirect a portion of that payment through a properly structured infinite banking policy, you build cash value that continues compounding tax-free while you systematically eliminate the same debts via policy loans.

The end result: debt eliminated on a similar timeline, but instead of restarting at zero, you own a growing financial asset that provides tax-free access to capital, a death benefit for your family, creditor protection in most states, and a personal banking system you’ll use for the rest of your life.

Key Takeaway

Conventional debt advice asks: “How fast can I get to zero?” The infrastructure approach asks: “How can I get to zero AND have something to show for it?” Both eliminate debt. Only one builds wealth in the process.

The Debt Crisis: What You’re Actually Up Against

According to Experian, the average American household carries over $100,000 in total consumer debt — mortgages, student loans, credit cards, auto loans, and personal loans combined. That translates to nearly 10% of disposable income going directly to debt payments every month.

The trend is getting worse, not better. Credit card defaults have reached their highest level in 14 years. Nearly 100 million Americans are struggling with medical debt. And the opportunity cost of all that interest — the wealth you would have built if those dollars were compounding for you instead of against you — is staggering.

| Debt Type | 2024 | 2025 | Change |

|---|---|---|---|

| Mortgage | $12.05 T | $12.34 T | +2.4% |

| HELOC | $380 B | $422 B | +11.1% |

| Student Loan | $1.60 T | $1.61 T | +0.6% |

| Auto Loan | $1.53 T | $1.56 T | +2.0% |

| Credit Card | $1.14 T | $1.21 T | +6.4% |

| Personal Loan | $245 B | $253 B | +3.4% |

| TOTAL | $17.21 T | $18.33 T | +3.2% |

Source: Experian Consumer Debt Study (June 2025); NY Fed Household Debt & Credit Report (Q3 2025). Total reflects all consumer debt categories. Average consumer debt: $104,755.

Here’s what makes this particularly destructive: compound interest works in both directions. When it’s working for you (inside a properly structured whole life policy), it builds wealth exponentially over time. When it’s working against you (credit card interest, auto loan interest, mortgage interest), it erodes wealth exponentially. Every dollar of interest you pay to a bank is a dollar that can never compound for your family. For a deeper look at how much this costs over a lifetime, see our analysis of your maximum lifetime potential.

This is why simply “paying off debt” isn’t enough. You need a system that stops the bleeding AND starts building at the same time.

How Borrowing From Life Insurance to Pay Off Debt Actually Works

Most people associate life insurance with paying off debt when you die — beneficiaries receive the death benefit and use it to cover a mortgage, student loans, or other obligations. That’s one use, and for a full breakdown, see our guide on what happens to your debt when you die.

But that’s not what we’re talking about here. This strategy uses the cash value of a permanent life insurance policy to eliminate debt while you are still alive — and to build wealth in the process.

The mechanics are straightforward: you fund a properly designed whole life insurance policy that maximizes cash value growth. As the cash value builds, you take policy loans against it to pay off your highest-priority debts. The critical advantage is that when you borrow against your cash value, the entire balance continues earning interest and dividends — your money works in two places simultaneously.

This is the Infinite Banking Concept applied specifically to debt elimination. Nelson Nash, who developed IBC, put it simply: the goal is to recapture the interest you’re paying to banks and keep that money working for you and your family.

The strategy combines two proven approaches:

1. Debt Snowball or Debt Avalanche — You prioritize debts either by smallest balance first (snowball, for psychological momentum) or highest interest rate first (avalanche, for mathematical optimization). Either works. For more on this framework, see our guide on good debt vs. bad debt.

2. Infinite Banking Concept (IBC) — You use policy loans from your properly structured whole life policy to fund the debt payoffs, then repay the loans on your terms while your cash value keeps compounding.

The critical piece most people miss: if you only use the snowball or avalanche method, you end up at zero. No debt, but no assets either. By adding IBC to the equation, every dollar you use to pay off debt also builds wealth inside your policy. When the last debt is gone, the money you used to eliminate it is still there — sitting in your policy, compounding, and available for whatever comes next.

Real-World Case Study: How Lenny Eliminated $30,000 in Credit Card Debt

Our debt elimination specialist, Denise Boisvert, walked a client through this exact strategy. Here’s how it played out:

Lenny had $30,000 in credit card debt spread across three cards. He was making payments above the minimums, but the interest was keeping him on a treadmill — paying aggressively but making slow progress. Here’s the step-by-step approach Denise designed for him:

Step 1 — Assessment of Current Debt: Evaluate the total amount owed across all credit cards. Lenny had a total debt of $30,000 spread across three cards with varying interest rates and minimum payments.

Step 2 — Minimum Payments Adjustment: Identify each credit card’s minimum required monthly payments. Instead of paying more than these minimums, reallocate the excess payments towards the life insurance strategy.

Step 3 — Infinite Banking Introduction: Redirect the funds above the minimum payments into a permanent life insurance policy structured for high cash value growth. This creates a dual-purpose cash reserve that grows over time and can be borrowed against at lower interest rates than credit cards.

Step 4 — Debt Repayment Plan: Utilize the cash value from the life insurance policy to start paying off the credit cards, beginning with the smallest debts first:

- Year 1: Focus on the smallest credit card debt. Lenny aimed to clear his Home Depot card with a $5,000 balance by redirecting $600 monthly into the policy.

- Year 2 and beyond: As each debt is cleared, the previously allocated funds for those debts are added to the life insurance contributions, increasing the policy’s cash value more rapidly and enabling larger debt repayments in subsequent years.

Step 5 — Continuous Monitoring: Monitor the policy’s cash value growth and adjust contributions as necessary, considering potential extra income sources like tax returns, bonuses, or gifts to expedite debt repayment.

Step 6 — Policy Loan Repayment: After settling all credit card debts, the focus shifts to repaying the policy loans. Repayment is flexible and tailored to individual preferences.

Step 7 — Long-Term Financial Strategy: Even after paying debts, continue contributing to the life insurance policy. It serves not just as a debt repayment mechanism but as a personal banking system for future financial needs — offering low-interest loans and growing tax-free.

Step 8 — Legacy and Security: Beyond debt management and financial flexibility, the policy provides a death benefit, securing a legacy for Lenny’s family.

The Outcome

Lenny eliminated all $30,000 in credit card debt — and kept the wealth-building infrastructure after the debt was gone. Instead of being back at zero with no debt and no assets, he had a funded whole life policy with growing cash value, a death benefit protecting his family, and a personal banking system he could use for every major purchase going forward. That’s the difference between eliminating debt and eliminating debt while building wealth.

The Minimum Payment Transition Strategy

The most common question about this approach is practical: “If I’m already stretched thin making debt payments, how can I afford to fund a policy AND keep paying my debts?”

The answer: you’re not finding new money — you’re redirecting existing money flow more strategically.

How the Transition Works

Let’s say you’re currently paying $1,200/month across multiple credit cards, car loans, and personal loans. Of that $1,200, perhaps $400 represents the actual minimum payments required, while $800 is extra payment you’re making to “attack the debt.”

Traditional approach: Throw all $1,200 at debt until it’s gone (3-5 years), then have $0 debt and $0 assets.

Strategic IBC approach:

- Months 1-12: Reduce to minimum payments ($400/month). Redirect the freed-up $800/month into a properly designed whole life policy with a Paid-Up Additions rider.

- During this period: Yes, you’ll pay more interest on your debts (approximately $500-800 total over the year). But you’re building $9,600 in annual premium into infrastructure that will work for decades.

- Months 6-12: Your cash value reaches $6,000-7,000 (with a 90/10 policy design optimized for immediate cash value).

- Months 12-18: Take your first policy loan of $5,000-6,000 to completely eliminate your highest-interest debt. That debt’s minimum payment now gets redirected to increase your policy premium.

- Year 2: You’re now funding the policy at $900-950/month (original $800 + the freed minimum payment from eliminated debt). Cash value accelerates.

- Years 2-3: Use another policy loan to eliminate the next debt. Repeat the cycle.

- Years 3-4: Final debts eliminated via policy loans. Now your entire previous debt payment ($1,200/month) can become policy premium — or you can scale back and deploy capital to wealth-building assets.

Why This Feels Wrong (But Actually Works)

Your instinct will scream: “How can I REDUCE my debt payments? Won’t that cost me more in interest?”

Short answer: Yes, temporarily. You’ll pay an extra $500-1,200 in interest during the first 12-18 months while building policy cash value.

But here’s what you’re buying with that temporary interest cost: financial infrastructure that will be operational for 30-50 years, immediate death benefit protection for your family, elimination of all debts within 3-5 years, and the foundation to deploy capital to productive assets thereafter. You’re not just buying a policy — you’re building the infrastructure for Volume-Based Banking.

You’re trading 12-18 months of interest inefficiency for a lifetime of financial infrastructure. That’s not a cost — it’s an investment in escaping the cycle that leaves 73% of Americans dying with debt.

Critical Requirement: Positive Cash Flow Margin

This strategy requires one absolute prerequisite: you must be earning more than you spend. If you’re spending 100% of income on minimum payments with zero margin, you need to address that first through income increase, expense reduction, or both. The minimum payment strategy only works if you have discretionary debt payments (amounts above minimums) that can be redirected.

The 10:1 Flexibility Safety Valve

Smart policy design includes flexibility for real-life disruptions. A properly structured policy might have:

- Total designed premium: $1,000/month ($12,000/year)

- Base premium (required): $100/month ($1,200/year)

- Paid-Up Additions (flexible): $900/month ($10,800/year)

This 10:1 ratio means if you face an unexpected expense — car repair, medical bill, temporary income disruption — you can drop to just $100/month without the policy lapsing. Once cash flow normalizes, resume full premium. This flexibility is critical during the debt transition phase. For more on how this design works, see our guide on overfunded life insurance.

Life Insurance Debt Strategy vs. Conventional Approaches: An Honest Comparison

Most people considering this strategy are comparing it against what they already know — debt consolidation, balance transfers, snowball method, or simply grinding through payments. Here’s how the approaches compare head-to-head:

| Feature | IBC Debt Elimination | Debt Snowball / Avalanche | Debt Consolidation Loan | Balance Transfer Card |

|---|---|---|---|---|

| Eliminates Debt? | ✓ Yes (3-5 years) | ✓ Yes (3-7 years) | ✓ Yes (restructures) | Partially (single card only) |

| Builds Wealth Simultaneously? | ✓ Yes — cash value compounds throughout | ✗ No — back to $0 when done | ✗ No | ✗ No |

| Death Benefit Protection? | ✓ Yes — immediate, tax-free | ✗ No | ✗ No | ✗ No |

| Tax Advantages? | ✓ Tax-deferred growth, tax-free access | ✗ None | ✗ None | ✗ None |

| Credit Check Required? | No (policy loans don’t check credit) | N/A | Yes | Yes (good credit needed) |

| Repayment Flexibility? | ✓ You set the terms | Self-directed | Fixed schedule | Minimum payments, 0% expires |

| Creditor Protection? | ✓ Protected in most states | ✗ None | ✗ None | ✗ None |

| Addresses Root Cause? | ✓ Builds banking system that prevents re-accumulation | Partially (discipline-based) | ✗ No (often leads to more debt) | ✗ No (often re-accumulate) |

| Long-Term Asset After Debt Is Gone? | ✓ Growing policy with banking function | ✗ Nothing | ✗ Nothing | ✗ Nothing |

| Best For | People who want to eliminate debt AND build a wealth system simultaneously | People with discipline who just want debt gone fast | People with good credit seeking lower interest rate | Small, single-card balances with 0% intro rate |

Note: IBC debt elimination requires a properly designed participating whole life policy from a mutual insurance company. Results vary based on policy design, premium amount, and individual discipline. Not suitable for individuals with no discretionary cash flow above minimum debt payments.

How Debt and Interest Work For or Against You

There are two primary types of debt: destructive debt (liabilities that take money out of your pocket) and productive debt (leverage that puts money into your pocket). The key is to eradicate destructive debt and — if appropriate — use productive debt strategically. For a full framework on this distinction, see our guide on good debt vs. bad debt.

What most people don’t realize is that just like money can grow and compound over time, losses compound the same way. The interest you pay to credit card companies, auto lenders, and mortgage servicers doesn’t just cost you the payment amount — it costs you everything that money would have earned if it were compounding for you instead.

Because people only earn a finite amount of money during their lifetime, sending a share of it to banks in the form of interest instead of building assets is the primary reason most people fall short of retirement goals. This is the opportunity cost that conventional financial advice rarely addresses.

Opportunity Cost: The Hidden Price of Every Payment

Your opportunity cost is the purchase price plus sales tax, compared to how much that money would have earned given time to grow in a compound interest environment. Nelson Nash, author of Becoming Your Own Banker, made the essential point: we finance everything we buy, whether through a loan or with cash. Both have a cost. The question is who collects the interest — a bank, or you.

Recapturing Your Dollars

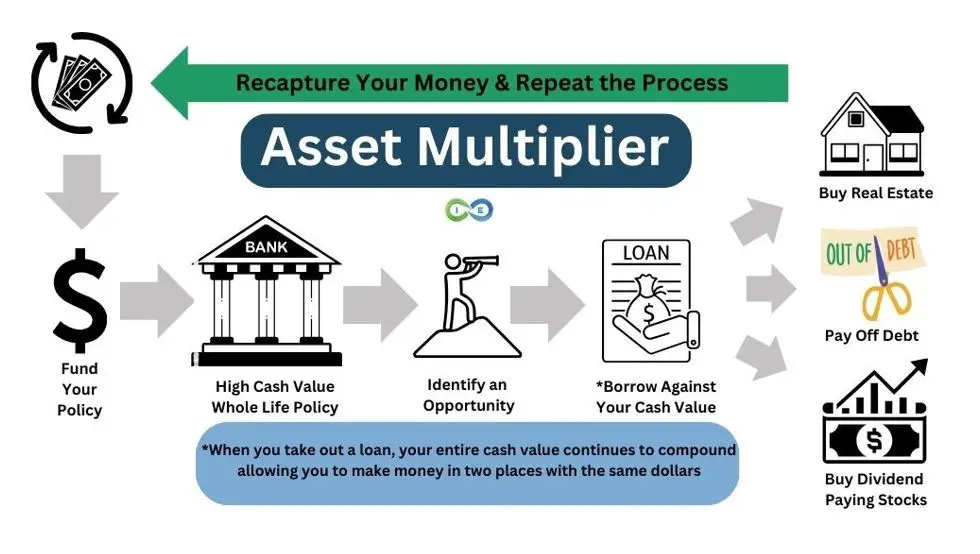

Every dollar you send to a bank or lender is gone forever. But using a properly structured whole life policy, you can become your own banker — borrowing against your own cash value to make purchases and pay off debts, while your entire balance continues earning interest and dividends. The money works in two places simultaneously: eliminating debt AND compounding wealth.

You Can Beat the System By Becoming the System

Most financial advisors recommend paying down debt by working more, spending less, refinancing your home, or consolidating everything into one payment. These approaches have their place, but they share a fundamental flaw: none of them build anything. When the debt is gone, you’re at zero.

Why Traditional Debt Solutions Often Fail

Research consistently shows that households who attempt debt consolidation or refinancing without addressing the underlying system often end up with more debt than they started with. Consolidation treats the symptom, not the disease. The most successful debt eliminators share one common trait: they established systems that prevented debt re-accumulation while simultaneously building wealth. This is precisely what properly structured whole life insurance provides — it’s not just a debt tool, it’s a financial operating system.

Coordinated Strategies: Snowball + IBC

The debt snowball (paying smallest balance first) or debt avalanche (paying highest interest first) are both effective frameworks. The question is whether you use them alone or in combination with IBC.

Using snowball/avalanche alone: you eliminate all debt and end up at zero. Using snowball/avalanche combined with IBC: you eliminate all debt and end up with a funded, compounding policy. The effort is similar. The outcome is dramatically different.

The Asset Multiplier Blueprint: Once debt is eliminated, your policy becomes the foundation for deploying capital to productive assets while cash value continues compounding.

Creating Money Momentum in the Right Direction

Once you understand the concept, the next question is how to make it work mechanically. Three features of properly designed whole life insurance make this strategy possible:

Velocity of Money

When you take a policy loan to pay off a credit card, your cash value continues compounding as if you never touched it. Meanwhile, the borrowed money eliminates a liability. Your dollar is working in two places simultaneously — that’s velocity. As you repay the loan (on your schedule), you’re restocking your personal bank for the next deployment. This cycle — fund, borrow, deploy, repay — is what makes the infinite banking concept “infinite.” For a comparison with another velocity-based approach, see our guide on infinite banking vs. velocity banking.

Paid-Up Additions

Paid-up additions (PUAs) are the engine of this strategy. PUAs allow you to overfund your policy within IRS guidelines, creating immediate cash value that’s available for borrowing much faster than a base-premium-only policy. In a policy designed for debt elimination, the PUA rider typically represents 60-90% of the total premium, maximizing the cash available for deployment while keeping the base premium low enough to maintain flexibility.

Dividends

Mutual insurance companies share profits with policyholders through annual dividends. While not guaranteed, the best mutual companies have paid dividends consistently for over 100 years. These dividends can be used to purchase additional paid-up insurance, further accelerating cash value growth — and further accelerating your debt elimination timeline. Over time, dividend history shows these payments have been remarkably consistent through every economic cycle.

Why Whole Life Insurance Is the Right Vehicle for This Strategy

Not just any life insurance works for this approach. You need a participating whole life policy from a mutual insurance company. Here’s why the loan mechanics matter:

Wash Loans

The best carriers for this strategy offer what’s known as a wash loan — where the loan interest rate is effectively offset by the dividend credit on borrowed funds. With top mutual carriers, you might borrow at 5% while your cash value earns 5% or more in guaranteed interest plus dividends. The net cost of borrowing approaches zero, which is what makes using policy loans for debt elimination so powerful compared to traditional consolidation loans.

Loan Payback on Your Terms

Unlike a bank loan, credit card, or consolidation product, policy loan repayment is entirely on your terms. No fixed schedule. No credit check. No approval process. No penalties for paying early or late. You decide how much and when to repay based on your cash flow and priorities. This flexibility is critical during the debt elimination phase when your financial picture is changing month to month.

For a complete breakdown of the mechanics, see our guide on borrowing against life insurance: pros and cons.

What Happens After Your Debt Is Gone (This Is the Real Payoff)

This is the section no other debt advice ever writes — because conventional approaches don’t have an answer for it. When you follow the standard snowball method and your last debt is paid off, you have… nothing. You’re at zero. The celebration lasts a week, and then you’re starting from scratch building wealth.

With the IBC approach, when your last debt is eliminated, you still have:

- A funded whole life policy with growing cash value that continues compounding tax-free

- A personal banking system — every future major purchase (vehicles, home repairs, investments, education) can be funded through policy loans, keeping the compounding cycle uninterrupted

- A death benefit protecting your family regardless of what happens

- Creditor protection in most states

- Tax-free retirement income available through policy loans in later years

- The foundation for deploying capital to real estate, business acquisitions, or other wealth-building assets

The entire $1,200/month (or whatever you were paying toward debt) is now available to fund your policy at full capacity, deploy into productive assets, or both. You’ve gone from treading water to building momentum — and the infrastructure just gets more efficient every year.

Beyond Debt Elimination: The Infrastructure Play

If the idea of turning debt payments into financial infrastructure resonates — if you’ve sensed that conventional advice leaves you running on a treadmill — our Ultimate Asset framework shows how this foundation connects to a complete wealth-building system. Debt elimination is phase one. Volume-Based Banking is what comes next.

Should You Cash Out Life Insurance to Pay Off Debt?

This is a different question than what we’ve been discussing — and the answer is almost always no.

Cashing out (surrendering) a policy to pay off debt means destroying the asset permanently. You lose the death benefit, the tax-advantaged compounding, the banking function, and the creditor protection. You’re liquidating infrastructure to solve a temporary problem.

Borrowing against your policy is entirely different. The policy stays in force. The cash value continues compounding. The death benefit remains intact (minus the outstanding loan balance). You maintain the infrastructure while using it to solve the problem.

If you’re considering cashing out an existing policy to pay off debt, talk to an advisor first. There may be a better path — including restructuring the debt, taking a policy loan instead of a surrender, or doing a 1035 exchange into a better-designed policy. For a full overview of all the ways to access cash value without surrendering, see our guide on accessing cash value from life insurance.

Properly Designing a Policy for Debt Elimination

Not every whole life policy works for this strategy. The policy must be specifically designed for maximum cash value growth and early accessibility. Here’s what to look for:

Mutual insurance company: A mutual company shares profits with policyholders via dividends. This is non-negotiable.

High PUA-to-base ratio: The paid-up additions rider should represent 60-90% of total premium to maximize early cash value access.

Structured below MEC limits: The policy must stay within Modified Endowment Contract guidelines to maintain tax-free loan access.

Flexible PUA rider: You need the ability to reduce premiums during tight months without the policy lapsing (the 10:1 safety valve described above).

Competitive loan rates: Look for carriers with non-direct recognition or wash loan features where the loan cost is effectively neutralized by dividend credits.

Strong financial ratings: A+ rated carriers from the top-rated insurance companies. See our reviews of Penn Mutual, MassMutual, Guardian, Lafayette Life, and New York Life for specific carrier analysis.

For a full breakdown of policy design principles, see our guide on whole life insurance illustrations and our overview of the top infinite banking companies.

How to Fund Your Infinite Banking Policy

One of the best ways to ensure consistent funding is to “pay yourself first” — make your policy premium the first obligation each month, just as you would a mortgage payment. By treating the premium as non-negotiable, you build the infrastructure systematically while still covering your other expenses.

Sources of funding during the debt elimination phase:

- Redirected excess debt payments (the core of the minimum payment strategy)

- Tax refunds and bonuses — lump sum additions to PUA riders accelerate cash value

- Income from eliminated debts — as each debt is paid off, its minimum payment rolls into the policy

- Side income or pay increases — any new cash flow goes to the policy first

The goal is to reach full policy funding capacity as quickly as possible, because the sooner the policy is fully capitalized, the more powerful the banking function becomes. For those interested in how this connects to mortgage strategy specifically, see our dedicated guide on paying off your mortgage early with infinite banking.

Is Borrowing From Life Insurance to Pay Off Debt Right for You?

This strategy is powerful, but it’s not for everyone. Here’s an honest assessment:

This approach works well for you if:

- You have stable income with positive cash flow margin (paying more than minimums on debt)

- You’re willing to commit to a 3-5 year strategy rather than looking for a quick fix

- You want to eliminate debt AND build a lasting financial asset

- You value building a system over just solving a temporary problem

- You can commit to consistent premium payments (even at reduced levels during tight months)

This approach is NOT right for you if:

- You’re spending 100% of income on minimum payments with no margin to redirect

- You need all debt eliminated within 12 months (this is a 3-5 year approach)

- You’re looking for a quick fix rather than building infrastructure

- You don’t have the financial discipline to manage policy loans responsibly

- You have urgent, immediate financial needs that preclude any premium commitment

If you’re not sure which category you fall into, start with a conversation. Our team can review your specific numbers and tell you honestly whether this strategy makes sense for your situation — or whether you need to address other financial fundamentals first.

Ready to Turn Debt Payments Into Wealth?

Denise Boisvert, featured in the video above, has helped clients like Lenny erase $30,000 in credit card debt using whole life insurance and the Infinite Banking Concept. Schedule a session with her to discover how you can do the same.

- ✓ Get a custom debt elimination plan using a high-cash-value policy

- ✓ Learn how to pay off credit cards, auto loans, or student loans faster

- ✓ See your personalized numbers — how long to eliminate all debt while building wealth

- ✓ Understand the policy design that makes the 10:1 flexibility safety valve work

No obligation. No pressure. Just an honest assessment of whether this strategy fits your situation.

THE ULTIMATE FREE DOWNLOAD

The Self Banking Blueprint

A Modern Approach To The Infinite Banking Concept

Frequently Asked Questions

Can you borrow from life insurance to pay off debt?

Yes — if you have a permanent life insurance policy (whole life or universal life) with accumulated cash value, you can take a policy loan against that cash value and use the funds for any purpose, including paying off credit cards, auto loans, student loans, or other debt. Policy loans don’t require a credit check, have no fixed repayment schedule, and your cash value continues earning interest and dividends while the loan is outstanding. For a full breakdown, see our guide on borrowing against life insurance.

Does life insurance pay off debt when you die?

Yes. Life insurance beneficiaries receive the death benefit income tax-free and can use it to pay off any outstanding debts — mortgages, credit cards, student loans, medical bills, or other obligations. However, the death benefit is not legally required to go toward debt. Beneficiaries choose how to use the funds. For a detailed guide on what happens to specific types of debt after death, see our article on what happens to your debt when you die.

Should I cash out my life insurance to pay off debt?

In most cases, no. Cashing out (surrendering) a policy permanently destroys the asset — you lose the death benefit, the tax-advantaged compounding, the creditor protection, and the banking function. Borrowing against the policy is different: the policy stays in force, cash value keeps compounding, and the death benefit remains (minus outstanding loan). If you’re considering surrendering a policy, consult with an advisor first — there may be a better option, including a 1035 exchange to a more efficient policy.

How is this different from debt consolidation?

Debt consolidation replaces multiple debts with one larger debt at (hopefully) a lower interest rate. It reduces complexity but doesn’t build anything — when the consolidation loan is paid off, you have zero debt and zero assets. The IBC debt strategy eliminates debt AND builds a tax-free, compounding financial asset simultaneously. The policy remains yours after the debt is gone, providing a banking system for all future major purchases and a growing death benefit for your family.

How long does it take to pay off debt with this strategy?

Typically 3-5 years for consumer debt (credit cards, auto loans, personal loans), depending on the total amount, your cash flow margin, and how aggressively you fund the policy. Mortgage payoff using this strategy takes longer but follows the same principles — see our dedicated guide on paying off your mortgage early with infinite banking.

Can I use infinite banking to pay off my mortgage?

Yes. Many practitioners use IBC policy loans to make strategic lump-sum principal payments on their mortgage, dramatically reducing the loan term while cash value continues compounding. The strategy is particularly effective for mortgages because of the large dollar amounts and long timelines involved. We’ve written a comprehensive guide on this specific application: Pay Off Your Mortgage Early With Infinite Banking.

What if I don’t have a whole life insurance policy yet?

That’s where most people start. You don’t need an existing policy to begin this strategy — in fact, the policy is designed from scratch specifically for your debt elimination and wealth-building goals. The key is working with an advisor who understands infinite banking policy design and can structure the PUA-to-base premium ratio for maximum early cash value while maintaining flexibility.

What kind of life insurance works for this strategy?

A participating whole life insurance policy from a mutual insurance company, structured with a high paid-up additions rider for maximum cash value growth. The policy must stay within MEC limits to maintain tax-free loan access. Term life insurance does NOT work for this strategy — it has no cash value component.

Is there a tax impact when I borrow from my policy to pay off debt?

No — as long as the policy is not classified as a Modified Endowment Contract (MEC), policy loans are not a taxable event. You’re borrowing against your cash value, not withdrawing it, so there is no income tax triggered. This is one of the major advantages over cashing out a 401(k) or taking a taxable withdrawal from other accounts to pay off debt. For a full overview of life insurance tax treatment, see our guide on is life insurance taxable.

How much cash value do I need before I can start paying off debt?

With a properly designed policy (high PUA-to-base ratio), you can typically begin taking policy loans within 6-12 months. In a policy where 90% of the premium goes to paid-up additions, a $1,000/month premium could generate $6,000-7,000+ in accessible cash value by the end of the first year. You don’t need to wait until you have enough to pay off ALL debt — the strategy is sequential, starting with the smallest or highest-interest balance first.