Becoming Your Own Banker with Life Insurance: The Complete Framework

As part of our comprehensive series on the infinite banking concept, we’re breaking down exactly how banking with life insurance works and why being your own bank is becoming a popular financial strategy for wealth-building.

Note: We are not suggesting that you are literally creating a banking institution or becoming a licensed banker. Rather, this concept revolves around taking control of your money by adopting the mindset and strategies that banks use to build wealth. This banking on yourself approach helps you achieve financial independence outside traditional banking systems.

The following 7-step blueprint for building your own banking system using whole life insurance will demonstrate how you can achieve financial freedom independent from traditional banks, Wall Street fluctuations, and the typical financial constraints many Americans face today.

The 7-Step Framework to Creating Your Own Private Banking System:

- Step 1: High Cash Value Whole Life Insurance

- Step 2: Strategic Life Insurance Riders

- Step 3: Fund Your Banking System

- Step 4: Finance Your Own Purchases

- Step 5: Recapture Your Money with Interest

- Step 6: Repeat the Process

- Step 7: Strategic Estate Planning

THE ULTIMATE FREE DOWNLOAD

The Self Banking Blueprint

A Modern Approach To The Infinite Banking Concept

Step 1: High Cash Value Whole Life Insurance – The Foundation of Your Banking System

The most effective vehicle we’ve identified for implementing the infinite banking strategy is high cash value whole life insurance from a mutual insurance company. This specific type of dividend-paying whole life policy differs significantly from traditional whole life insurance in its design approach. While conventional policies emphasize death benefits, a policy structured for personal banking prioritizes early cash value accumulation.

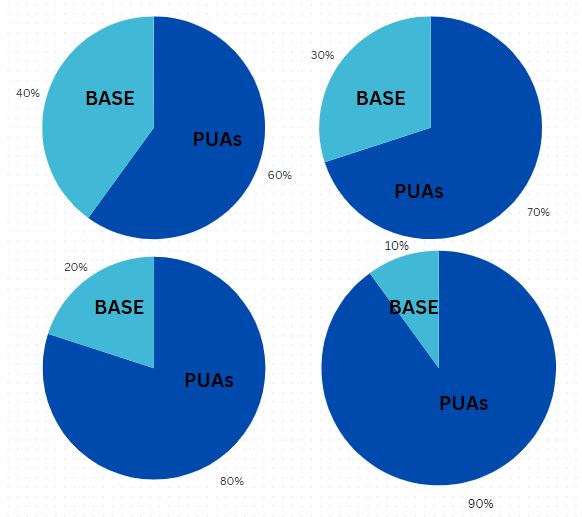

Paid-Up Additions: The Key to Early Cash Value Growth

The primary method for achieving rapid cash value growth is designing your policy with a higher proportion of paid-up additions (PUAs) versus base premium. The greater the percentage allocated to paid-up additions, the faster your early cash value grows. Popular whole life policy designs typically feature PUA/Base premium ratios of 60/40, 70/30, 80/20, and sometimes even 90/10 for maximum early cash value accumulation.

Section 7702: Your Tax Advantage Foundation

One of the most compelling benefits of using dividend-paying whole life insurance for your personal banking system comes from the tax advantages provided under IRC section 7702.

Under this code section, neither policy interest accrued nor dividends paid are reported as taxable income. Your cash value grows tax-deferred and can be accessed tax-free through policy loans, creating a powerful tax-advantaged financial tool.

As tax strategist Tom Wheelwright of Rich Dad Advisor fame explains, the tax code is a series of incentives. Thanks to IRC 7702, cash value life insurance represents one such financially strategic incentive.

Many carriers offer quality cash value policies, but our experience shows that selecting from the top dividend-paying whole life insurance companies typically provides the best foundation for an infinite banking strategy.

We say “typically” because at insuranceandestates.com, we recognize that each individual has unique financial goals and objectives. While participating whole life insurance frequently meets these diverse needs, in rare occasions indexed universal life insurance might be more appropriate.

Balancing Cash Value and Death Benefit for Optimal Banking Performance

The primary objective of an infinite banking policy is maximizing cash value while minimizing the initial death benefit. This strategic approach ensures that more of your premium payments flow directly into your accessible cash value.

This policy design approach actually reduces commissions for us as agents.

And we’re perfectly comfortable with that approach, as our primary mission is serving our clients’ best interests above our own.

Some clients may desire a substantial death benefit from the beginning. While a “banking policy” isn’t initially designed to provide a large death benefit (though it will grow significantly over your lifetime), you can obtain additional coverage through the strategic life insurance riders we’ll discuss next.

Step 2: Strategic Life Insurance Riders – Customize Your Banking Policy

A properly designed high cash value whole life insurance policy may include several of these powerful riders to maximize early cash value growth and policy flexibility:

Paid-Up Additions Rider: The Cash Value Accelerator

Paid-up additions are essentially additional insurance coverage that’s fully paid for upon purchase.

The Paid-Up Additions Rider allows you as the policy owner to purchase additional death benefit while simultaneously increasing your policy’s cash value growth rate.

This rider becomes particularly powerful when you direct your annual dividends from participating life insurance companies toward purchasing more paid-up additions, creating an exponential compound growth effect.

Life Insurance Supplement Rider: Strategic Blending

The Life Insurance Supplement Rider (LISR) strategically blends lower-cost term life insurance with permanent life insurance. The term portion gradually decreases as you make payments, eventually leaving you with only permanent coverage.

Additional Life Insurance Rider: Enhanced Premium Capacity

The Additional Life Insurance Rider (ALIR) enables you to make increased premium payments to purchase additional participating paid-up life insurance, enhancing both your policy’s death benefit protection and cash value accumulation potential.

Term Life Rider: Flexible Protection Enhancement

Not to be confused with the LISR mentioned above, the Term Life Rider (or Renewable Term Rider) provides straightforward term life insurance that can be converted to permanent life insurance in the future if you choose. Adding the term rider to your policy allows you to overfund your policy and remain in the IRS guidelines.

This rider is an excellent option for young families implementing infinite banking who need substantial death benefit protection immediately. It offers additional coverage that can be converted to permanent insurance as your financial position strengthens.

Guaranteed Insurability Rider: Future-Proofing Your Coverage

The Guaranteed Insurability Rider (GIR) might not immediately increase your cash value growth, but it provides the valuable guarantee that you can purchase additional insurance in the future without answering health questions or taking medical exams.

This option is particularly valuable when considering life insurance for children, as it guarantees their ability to increase coverage regardless of future health conditions.

Step 3: Fund Your Banking System – Strategic Capitalization

With your policy properly structured, it’s time to fund it strategically. The optimal approach is to over-fund your policy to the maximum point possible without triggering modified endowment contract (MEC) status.

The IRS has established guidelines that prevent excessive contributions to life insurance policies to prevent their use as pure tax shelters. While we want to avoid MEC status, we also aim to maximize early cash value accumulation by utilizing the strategic riders mentioned above.

Depending on your situation, you may qualify for backdating your policy to save age, allowing you to contribute more money in the first year than would otherwise be permitted.

The Vital “Capitalization Period”

As time passes, your policy’s cash value will steadily increase. In Nelson Nash’s foundational book, Becoming Your Own Banker©, he recommends dedicating several years to this capitalization phase before major utilization.

The good news? A properly structured insurance policy begins accumulating cash value almost immediately. Depending on your policy design, you should have access to 90% or more of your cash value from day one, providing liquidity while your banking system grows.

Step 4: Finance Your Purchases – Putting Your Banking System to Work

Important Note: For an authentic banking policy to function optimally, always borrow from the policy rather than withdrawing money.

When you withdraw, you permanently reduce your cash value.

When you borrow from the insurance company using your cash value as collateral, your cash value continues growing inside your policy.

This is where the infinite banking strategy becomes truly exciting and demonstrates why life insurance can be a powerful investment vehicle.

As your policy accumulates substantial cash value, you can leverage that value as collateral through policy loans. The insurance company lends you money secured by your cash value, and you can deploy those funds however you choose.

The key advantage: when you use your cash value as collateral and take out a policy loan, the money in your account continues growing through uninterrupted compound interest.

This means your money works for you in two ways simultaneously – continuing to grow within your policy while also being deployed for various financial objectives.

Strategic Uses for Policy Loans

Acquire Cash-Flowing Assets

Real estate stands out as a premier cash-flowing asset. Real estate investments can generate regular income while offering additional tax advantages. This scenario perfectly showcases the infinite banking concept in action.

At its core, infinite banking involves lending yourself money and systematically recapturing that capital. When you use a policy loan for a real estate down payment, you can then direct the monthly cash flow from that property toward repaying your policy loan with interest.

Pro tip: Don’t shortchange yourself here. Charge yourself the current interest rate that a traditional lender would charge you. Remember you wear two hats, the banker and the investor.

As you use your property’s cash flow to repay your loan with interest, you simultaneously increase your policy’s death benefit and accelerate cash value growth.

This process creates even more opportunities for personal financing in the future, making it one of the most powerful real estate wealth-building strategies available.

Finance Your Business Operations

Another strategic application for policy loans is financing your business operations. Take a policy loan, then lend that money to your business. Your business then repays you with interest for the loan.

This approach allows you to recapture your own interest payments while replenishing your policy. Plus, your business may be eligible to deduct the interest payments, creating an additional financial advantage. A true win-win arrangement!

Self-Finance Major Purchases

Why deplete your savings or finance through traditional banks when purchasing vehicles, funding education, or making other significant investments? Instead, use your banking policy to self-finance these expenses.

This strategy allows you to recapture the interest you would have paid to financial institutions or recover the opportunity cost of paying cash without recouping your capital.

The greatest advantage of personal financing is your position as the banker. You determine the interest rate for repayment and the terms of your loan. However, to maximize the infinite banking strategy’s benefits, consistently repaying your policy loans with interest is highly recommended.

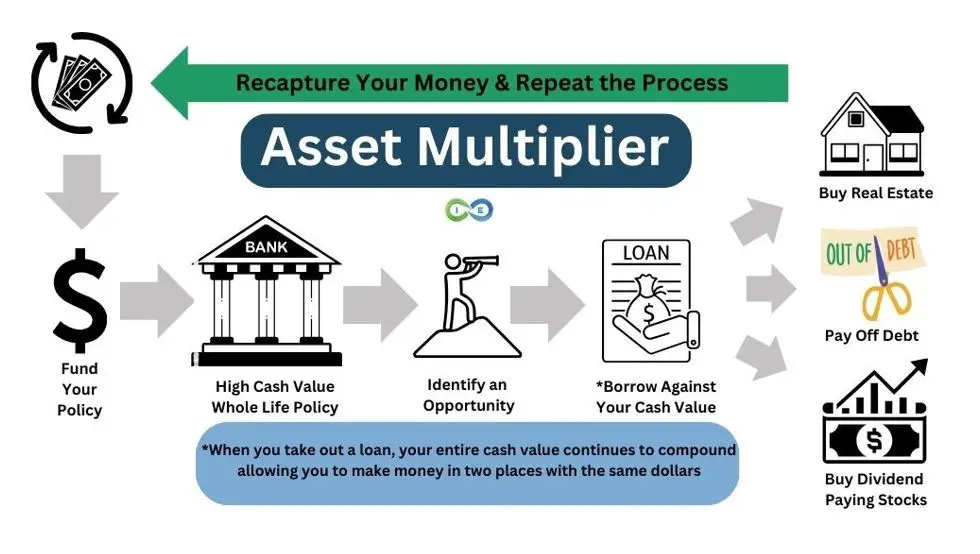

Step 5: Recapture Your Money with Interest – Building Your Banking System

Successfully implementing the infinite banking strategy requires discipline, particularly when it comes to recapturing both principal and interest on your policy loans. We call this process the “asset multiplier blueprint” and the goal is to use your life insurance asset to buy more assets.

For those with the discipline to consistently execute this vital step, the growth potential of your banking policy is virtually unlimited.

This step represents perhaps the most vital component of becoming your own banker. If you fail to repay yourself, you’re essentially “stealing the peas” as Nelson Nash would say.

Loan repayment forms the cornerstone of this financial strategy because it’s the systematic action that generates exceptional long-term returns throughout your lifetime.

As you continue developing your banking policy, you accumulate an increasingly substantial cash reserve that can provide tax-free income through strategic policy loans.

Understanding the Banking Interest Advantage

One primary revenue stream for traditional banks is the interest spread. You deposit funds with a bank, and they pay you interest—currently averaging around 0.49% at most major institutions as of June 2023.

Not exactly impressive.

The bank then lends your money at significantly higher rates. Even with a modest 5% lending rate, the bank’s profit margin is over 10 times greater than what they pay you. Would a 1,000% return on your money sound appealing?

Through infinite banking, instead of the bank capturing all these profits, you—as borrower, lender, and banker—keep all the financial benefits traditionally reserved for banks using the fractional reserve system.

What happens to your life insurance policy when you consistently recapture both principal and interest? It experiences compounding growth!

Another significant advantage: life insurance creditor and bankruptcy protection, depending on your state of residence.

If you live in a state with favorable insurance protection laws, your policy’s cash value may be sheltered from creditors, providing additional financial security.

Step 6: Repeat Steps 1-5 Infinitely – Creating Money Momentum

After repaying your policy loan, don’t allow your capital to sit idle. Instead, repeat steps 1-5 continuously. With each cycle through this process, your available capital base expands, creating increasingly powerful financial leverage.

This active approach stands in stark contrast to parking your money in government-designed retirement vehicles and putting your financial life on hold. That’s why we consider the 401k plan problematic in certain aspects.

By implementing infinite banking, you can enhance your life now while building for the future. This creates powerful money momentum, shifting your focus from constantly working for money to having your money consistently working for you.

Step 7: Strategic Estate Planning – Creating a Lasting Legacy

After successfully implementing your infinite banking strategy throughout your lifetime, you’ll have built a substantial estate to transfer to future generations.

Effective estate planning becomes essential for maximizing the legacy you leave to your family.

There are numerous strategies for accomplishing this, both during your lifetime and after your passing. The critical factor is planning proactively so your family can benefit from the full results of your disciplined financial approach.

With a properly structured estate plan, continuously growing cash value, and a guaranteed death benefit passing to your beneficiaries, you’ll be positioned to create a multi-generational financial legacy.

THE ULTIMATE FREE DOWNLOAD

The Self Banking Blueprint

A Modern Approach To The Infinite Banking Concept

Frequently Asked Questions About Infinite Banking

What is the infinite banking concept?

The infinite banking concept is a financial strategy that uses specially designed whole life insurance policies to create your own personal banking system. It allows you to borrow against your policy’s cash value while the full value continues to grow uninterrupted, essentially letting you use the same dollar in two places simultaneously.

Is infinite banking only for wealthy people?

No, infinite banking can be implemented at various financial levels. While having more capital allows for faster growth, many people start with modest monthly premiums and grow their banking system over time. The concept is about changing how you manage your money, not how much money you have.

What’s the difference between a traditional whole life policy and one designed for infinite banking?

Traditional whole life policies focus primarily on the death benefit, while policies designed for infinite banking are structured to maximize early cash value growth through paid-up additions and specialized riders. This design allows for greater liquidity and usable cash value in the early years of the policy.

Will borrowing from my policy reduce my death benefit?

Any outstanding policy loans at the time of death will reduce the death benefit paid to your beneficiaries. However, by implementing a disciplined loan repayment strategy with interest (as outlined in the infinite banking concept), you can actually increase your death benefit over time.

What happens if I don’t repay my policy loans?

While policy loans don’t require repayment on a set schedule (unlike bank loans), not repaying them means missing the important ‘recapture’ phase of infinite banking. Outstanding loans will accrue interest and potentially reduce your death benefit. For the strategy to work optimally, disciplined loan repayment with interest is essential.

How does infinite banking compare to investing in the stock market?

Unlike stock market investments, properly structured whole life insurance provides guaranteed growth, tax advantages, and protection from market volatility. While potential returns might be lower than aggressive stock investments, infinite banking offers predictability, access to capital without market timing concerns, and unique advantages like uninterrupted compound growth even while utilizing your money elsewhere.

How long does it take to build a substantial banking system?

The timeframe depends on your funding strategy, policy design, and usage patterns. With proper design, you’ll have access to cash value almost immediately, but most practitioners recommend a dedicated capitalization period of 3-7 years before making major policy loans. Substantial banking systems typically develop over 10-20 years of consistent implementation.

Ready to Take Control of Your Financial Future?

Schedule your complimentary infinite banking strategy session today and discover how becoming your own banker could transform your approach to building wealth.

42 comments

Jay Roe

Is there a way to roll a 401K into an insurance policy with minimal tax penalty?

Steven Gibbs

Hello Jay,

Great question, there isn’t a way to “roll” a 401(k) into an insurance policy; however, we do have people that want to pay now vs. facing the tax exposure later. This relates to the “pay taxes on the seed vs the harvest” question. This kind of decisions should be carefully considered with an expert and also perhaps discussed with your tax advisor. There are qualified annuities that you could roll over a 401(k) into, however. If you’re interested, our expert Jason Herring is very experienced in helping people with strategic tax moves and you can request a call from him by emailing jason@insuranceandestates.com.

Best, Steve Gibbs for I&E

Steven Gibbs is a licensed insurance agent, and the following agent

license numbers of Steven Gibbs are provided as required by state law:

Resident License; AZ agent #17508301,

Non-resident Licenses: TX agent #2273189, CA agent #0K10610,

LA agent #769583, MA agent #2049963, MN agent #40563357,

UT agent #655544.

Zakee Richardson

How long do I have to wait before I can take a loan out for investments.

Insurance&Estates

Your wait time would depend upon your policy design, premiums, etc. To get a concrete idea, you can have illustrations run for your personal scenario. A great start is to connect and request a call with Barry Brooksby at barry@insuranceandestates.com.

Best, Steve Gibbs, for I&E

Chuck

I have a mature term life insurance policy that went from $60.00 a month for 20 years after that it went to $350.00 a month. During this time I went on disability and due to that fact is was able to keep getting the coverage at no cost to me. I have some cash saved in the bank I want to place it in the life Insurance policy to shield it from any court orders for payment a creditors , Leon’s. I live in Mississippi, hypothetically speaking, thanks

Insurance&Estates

Hi Chuck, thanks for connecting. Unfortunately your situation with the expiration of term coverage is all too common based upon some flawed “advice” out there to cash in whole life policies. That said, if you’re looking for creditor protection a good first stop may be an attorney. If you’d like to pursue a policy go ahead and request a call with one of our experts by emailing Barry at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Darrell V. Salu

Working on saving a lump sum. Looking for an investment opportunity. This makes sense but don’t know anything about life insurance . Would like to connect with someone who could explain it to me in lamens terms and how to get started in something like this. Sincerely thank you so much!!!

Insurance&Estates

Hello Darrell, thanks for connecting. A great first step is to watch any of our webinars at insuranceandestates.com/webinars and when you do so, you can access Barry’s calendar to schedule a 1 to 1 call to take next steps.

Best, Steve Gibbs for I&E

Joe

How do you make “buy investment property” sound like it’s just on the shelf at the corner market? I mean when you purchase a property to make money from, it takes a great amount of work to find a property that is selling under the market value. If you expect to turn a monthly profit immediately off a newly purchased property, then you will never buy a property. So how do you just buy income property so easily? With no money to start with or no income other than what you hope to get?

Insurance&Estates

Hello Joe, when we’re speaking about real estate investment, at this point we are directing the message at active real estate investors. Yes, your point is well taken that acquiring real estate takes discipline and expertise. In the future we may be offering some webinars and training to help folks who want to get started.

Best, Steve Gibbs for I&E

Joe

I have no money or insurance policy, and no income. Is it possible to obtain a life insurance policy that i can immediately start living off of, and pay for the policy with those living expenses?

Insurance&Estates

Hello Joe, if have you no money that can be tricky and even “high cash value” policies generally need to mature before they provide enough cash to begin paying expenses from. If you can deposit of lump sum initially, your goal may be possible.

You can with our team of experts by emailing Barry Brooksby at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Casey Werner

How do I open a infinite bank account

Insurance&Estates

Hello Casey, a great first step is to request a call from Barry Brooksby, our IBC expert, at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Tyde McIntosh

At some point, assuming there is no plan for legacy, can the cash inside the policy be used to create a tax free income?

Insurance&Estates

Hello Tyde, yes this is a strategy often utilized for LIRP (Life Insurance Retirement Planning) where there are planned distributions (via policy loans) beginning at a certain age. To get illustrations to see exactly how this would work, go ahead and request a call be emailing Barry Brooksby at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Walter Rauch

I am seventy four years old. I have a old whole life of 15,000. I was thinking of opening up a life insurance policy, and removing it 10,000 at a time from the stocks, every year. What riders would I need to put in place. And would this be a good Idea now at my age?

Insurance&Estates

Hello Walter, your best first step is to connect with one of our IBC experts to have your policy and situation evaluated in detail. You can connect with Barry Brooksby as a first step by e-mailing him at barry@insuranceandestates.com and I will also forward your request to him.

Best, Steve Gibbs for I&E

Eric

This seems like one of those things that is good in theory but not in practice. Why? Allocating to a policy with high fees, opportunity cost between policy returns and market returns, risk of income changing when the person first adopts the strategy so they’re not able to meet policy obligations, risk of cash flowing asset not cash flowing as expected etc. Life insurance always sounds good in a vacuum but life is far from that regardless of net worth.

Insurance&Estates

Hello Eric, I’m just responding to caution our readers. Your commentary is typical of those who peddle market based investments as a one size fits all solution. Interesting that you say “life insurance always sounds good” which is untrue. For some people such as the young without families, it doesn’t. You also seem to take as a given that market based returns are “always” preferable to life insurance policy cash value returns which is also untrue due to inherent risk and inherent lack of predictability. When we counsel folks about permanent whole life options, we do not compare the “return” to a market based investments. However, this is irrelevant for the same reason I don’t hail eating vegetables and ridicule drinking water. As an estate planner, my opinion is that folks need both. That said, I can make a strong case that the 20 year moving average nearly always used to tout Wall Street is a misleading approach. How about the cost for mutual funds? In any event, I suggest you be careful with blanket statements that fail to consider the unique circumstances of every person, as I’m assuming you value the concept of being a trusted advisor. As an estate planner, I’ve observed the power of life insurance for many. For these folks, including myself, whole life insurance rises to the top of one’s most valuable assets.

Best, Steve Gibbs for I&E

Eugene

I’m just learning about the infinite banking potential, but not sure if a whole life policy is out of my budget. It looks like a great way to create security for my family while generating wealth (which also creates security).

Insurance&Estates

Hi Eugene, thank you for you comment and I agree, a powerful safe bucket wealth building vehicle. If you’d like to look more closely it this with our IBC expert Barry Brooksby, go ahead and reach out to him at barry@insuranceandestates.com.

Best, Steve Gibbs, for I&E

Ben

I have a soon to be 8 year old UIL policy, funded with a large single premium. My question is: Can I get one for my wife without triggering MEC?

Insurance&Estates

Hello Ben, thanks for commenting. Jason Herring can help you with IUL question and you can reach him directly at jason@insuranceandestates.com.

Best, I&E

Nicholas A Reed

I have read Nash’s book and maybe I need to go back and look at it again, but I am not sure I understand his examples. He shows a person deposits $5000 a year for the first sevens years for premiums and funding the plan and then takes out a car loan every 4 years and pays that back w/interest but after the 7 years, he shows no premiums being paid. Is that because the dividends are paying the premium along with the interest? I probably need to go back and read it again, but I didn’t understand that.

Thanks

Matthew Hamilton

So the policy illustration you’ve described is most likely a 7 pay policy. So that is to say that the owner would only pay for 7 years. At that time, they want to start taking loans every 4 years. The part that’s murky for me is if when you take a loan, if it opens up the policy for OP or extra repayments, or if you can only put back in what you took out. I’m not sure how your supposed to get extra interest into your policy.

Insurance&Estates

Hello Matthew, I understand your confusion. The short answer is, how much money you can repay to your policy is governed by the MEC limits which are typically calculated by the insurance company annually. So, depending on your policy design and paid up additions contributed each year, you may be able to pay in extra over and above the amount taken as a policy loan. It may be helpful to run some scenarios with our IBC expert Barry Brooksby and you can connect with him at barry@insuranceandestates.com.

Insurance&Estates

Hello Nicholas, thanks for your great questions. Your inquiry was forwarded to Jason Herring today; however, please feel free to connect with him at jason@insuranceandestates.com.

Best, I&E

Chantal

Hi. My son is currently overseas serving in the military. I am very much interested in a whole life policy that allows for the infinite banking strategy for him to set him on the right track for when he is ready to invest. Would he be able to start a policy while he is serving? Thanks.

Insurance&Estates

Hello Chantal, thanks for reading and commenting. We’ve forwarded your comment to Jason Herring, so if he hasn’t reached out yet, feel free to connect with him at jason@insuranceandestates.com.

Best, I&E

WeFactor

Thanks for sharing this article. I want to create my own private banking system. This article will surely help me to create it easily. This article is very good and useful site. I’ll definitely follow what you said here.

Wilson

I also think that the important thing is to plan ahead so that your family can receive the full extent of your disciplined work.I also think that by doing this, we can avoid issues as well. Thanks for sharing this article.

Insurance&Estates

Thanks for commenting and we agree that planning ahead is key.

Best, I&E

Ken Chan

Will this strategy work in other countries? I want to do the same thing here in asia.

Insurance&Estates

Hello Ken, there are some possibilities available for folks in other countries. I suggest you connect with Jason Herring if you haven’t already done so. He is available at jason@insuranceandestates.com.

Best,

Steve Gibbs for I&E

John

Would my life insurance that I have been paying into in the military for 16yrs work the same way? I am wanting to start my own business and need capital to invest to get started.

Insurance&Estates

Hi John, thanks for reading and commenting. I can’t say for sure what possibilities may be available because we have no knowledge of your military policy. for a more detailed discussion, you can contact Jason Herring at jason@insuranceandestates.com.

Best,

Steve Gibbs for I&E

Kevin

If I want to set a policy up to buy a car are there limitations about loan off your policy. Example Could I put 20,000 in today and then loan 17000 tomorrow to pay for a car? Is there a designated time the policy must exist before loaning off of it?

Insurance&Estates

Hi Kevin, great question…the short and general answer is that a policy will need some time to accrue cash value and mature before offering the cash for loan purposes. However, this availability of cash in the policy can be expedited in some cases depending on the strategy. Your example is perhaps a bit ambitious…$20,000 and $17,000 loan tomorrow doesn’t leave much to cover the base and cost of insurance. To put together some actual numbers, I suggest that you follow up with jason@insuranceandestates.com who has substantial expertise in designing IBC policies.

Best, Steve Gibbs for I&E

KIMIO OSAWA

Hi

Your method is working for someone like me living overseas?

I heard many similiar concepts but only people in the US and Canada?

Insurance&Estates

Kimio,

You will need to be in the United States in order to obtain a policy. You can read our article on foreign nationals and non us residents for more information on getting US life insurance as a non resident.

Sincerely,

I&E