The Infinite Banking Concept has become one of the most discussed, and most misunderstood, financial strategies of the last two decades. Depending on who you ask, it’s either a game-changing wealth-building system or a scheme designed to sell whole life insurance.

Neither is accurate.

IBC is a financial strategy that uses dividend-paying whole life insurance from a mutual insurance company as a personal banking system. Instead of storing capital in a traditional bank that pays you next to nothing while lending your money at 7–8%, you build cash value in a policy you control, borrow against it when you need capital, and your money keeps growing even while you use it.

The concept goes by many names. Be Your Own Bank, Bank on Yourself, Cash Flow Banking, Private Family Banking, the Perpetual Wealth Strategy. They all describe the same core idea: controlling the banking function in your life rather than outsourcing it to traditional financial institutions.

This guide is your starting point. We’ll explain what infinite banking is, how it works at a foundational level, and then point you to the right deep dive based on what you’re looking for, whether that’s evaluating whether IBC is right for you, learning how to implement it step by step, or choosing the right company and practitioner.

TL;DR — Infinite Banking in 60 Seconds

- The concept: Use a properly structured whole life insurance policy as your personal banking system instead of relying on traditional banks

- The mechanism: Build cash value, borrow against it for investments or major purchases, repay yourself, and repeat, your cash value keeps compounding even while you borrow against it

- The vehicle: Dividend-paying whole life insurance from a mutual insurance company, designed for maximum cash value growth

- What it replaces: Your bank, not your investments, the question isn’t “whole life vs. the stock market,” it’s “whole life vs. where you currently store and access capital”

- What it requires: Stable income, a 7+ year commitment, financial discipline, and a properly designed policy

Bottom Line: Banks hold over $200 billion in cash value life insurance on their own balance sheets. They don’t follow the advice they give retail customers. Infinite banking lets you use the same playbook, guaranteed growth, tax advantages, and liquidity on demand, at a personal level.

✓ Why Trust This Guide

This guide is written and maintained by Barry Brooksby, Authorized Nelson Nash Infinite Banking Practitioner with 25+ years in financial services, and Steve Gibbs, JD, AEP®, estate planning attorney and co-founder of Insurance & Estates — ranked the #1 life insurance agency on Trustpilot with 280+ verified reviews. Our team has designed and implemented 1,000+ IBC policies since 2017 as an independent agency with access to every major mutual carrier. We practice what we teach — our advisors use infinite banking in their own financial lives.

Table of Contents

What Is the Infinite Banking Concept?

The Infinite Banking Concept was created by Nelson Nash and outlined in his book Becoming Your Own Banker. The core idea is straightforward: instead of depositing your money in a traditional bank where it earns next to nothing, you build your own banking system using a properly structured whole life insurance policy from a mutual insurance company.

Nash recognized something most people overlook, your need for financing during your lifetime is far greater than your need for a death benefit. Every major purchase you make is financed, whether you realize it or not. You either pay interest to a lender, or you pay cash and give up the interest that money would have earned. Either way, there’s a cost. Infinite banking puts you on the other side of that equation.

The concept is so widely adopted by institutions that U.S. banks collectively hold over $200 billion in bank-owned life insurance (BOLI) on their balance sheets. They don’t follow the advice they give retail customers. They buy whole life because the math works for storing and accessing capital. Infinite banking lets you apply the same principles at a personal level.

How Infinite Banking Works

The mechanism that makes infinite banking fundamentally different from any other financial strategy comes down to one concept: your money works in two places at once.

When you borrow against your policy’s cash value, the insurance company lends you money using your cash value as collateral. Your entire cash value balance, including the portion backing your loan, continues compounding with guaranteed interest and dividends. You then deploy that capital into investments, business opportunities, or major purchases, and use the returns to repay your policy loan and repeat the cycle.

No savings account, HELOC, or 401(k) loan does this. When you withdraw from a bank account, that money stops growing. When you tap home equity, your house doesn’t appreciate faster to compensate. With infinite banking, your capital never stops compounding — even while you’re using it elsewhere.

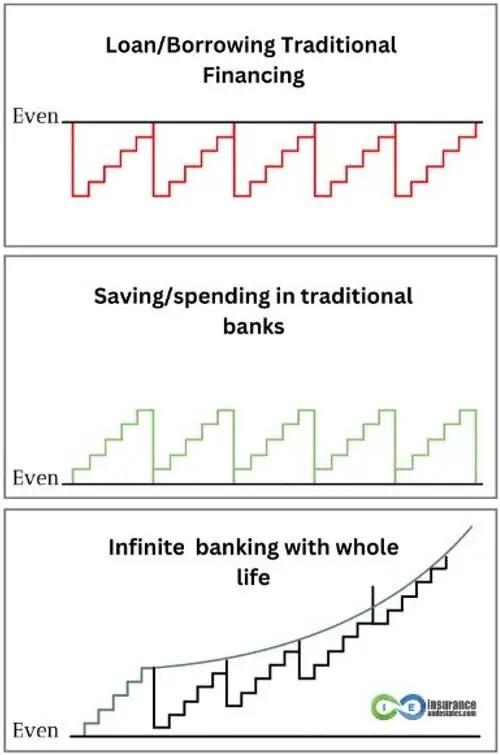

The visual below illustrates why this matters. Traditional financing keeps you perpetually below even, you borrow, dig out, and start over. Saving and spending through a traditional bank gets you back to even, but every major purchase resets your progress. With infinite banking, each borrow-and-repay cycle builds on the last, creating a stair-step pattern above the policy’s guaranteed growth curve.

That’s the full cycle: build cash value, borrow against it, deploy the capital, repay with interest, and repeat from an elevated position. Each cycle builds on the last. You never reset to zero.

For a complete step-by-step implementation walkthrough — including how to structure your policy, fund it strategically, and execute the borrow-and-repay cycle — see our 7-step guide to becoming your own banker.

The Vehicle: Whole Life Insurance from Mutual Companies

Infinite banking requires a specific type of life insurance — not just any policy off the shelf. The vehicle is dividend-paying whole life insurance from a mutual insurance company, designed to maximize cash value growth rather than death benefit.

This distinction matters. A traditional whole life policy emphasizes death benefit, which means more of your premium goes toward insurance costs. A policy designed for infinite banking does the opposite — it minimizes the initial death benefit and directs 60–90% of your premium toward paid-up additions, which flow almost entirely into accessible cash value from year one.

Why whole life and not another product? Three reasons:

- Contractual guarantees. Whole life is the only financial vehicle that provides guaranteed cash value accumulation, a guaranteed death benefit, guaranteed fixed premiums, and a guaranteed minimum interest rate — simultaneously. No market-based product offers this.

- Tax advantages. Under IRC Section 7702, your cash value grows tax-deferred, policy loans are tax-free, and the death benefit passes income-tax-free to beneficiaries. No capital gains taxes, no required minimum distributions.

- Dividend history. The top mutual companies we work with have paid dividends every single year for over 100 years — through the Great Depression, world wars, and every financial crisis in between.

Why a mutual company? Because mutual companies are owned by policyholders, not Wall Street shareholders. When the company profits, those profits return to you through dividends rather than enriching outside investors. This alignment of interests is foundational to how infinite banking works.

Understanding the difference between direct recognition and non-direct recognition companies also matters when you’re actively using policy loans — though policy design matters more than recognition type. For a deeper look at how whole life insurance works as a financial vehicle, start with our complete whole life insurance guide.

What Practitioners Use It For

Infinite banking isn’t a theoretical concept — it’s a system people use to finance the major purchases and investments they’d otherwise fund through traditional banks. The strategy works the same way regardless of the asset: borrow against your policy, deploy the capital, use the returns to repay your loan, and repeat from an elevated position.

The most common applications we see across 1,000+ client implementations:

Real Estate

Real estate is the most popular use case for policy loans. You borrow against your cash value for a down payment, use rental income to repay the loan with interest, and your policy’s cash value keeps compounding the entire time. When the loan is repaid, you have both the property and a larger capital base to deploy again. For a full walkthrough with real numbers, see our guide on using life insurance to buy real estate.

Debt Elimination

Some practitioners use policy loans to consolidate and eliminate high-interest debt — redirecting the interest they’d pay to credit card companies or lenders back into their own banking system. The math works particularly well when you’re replacing 15–25% interest debt with a 5% policy loan while your cash value continues earning 4–6%. For the debt elimination strategy, see our guide on using life insurance to pay off debt.

Business Financing

Business owners use policy loans to finance operations, equipment, inventory, or expansion without traditional bank approval processes. You take a policy loan, lend it to your business, and your business repays you with interest — recapturing payments that would otherwise go to a commercial lender. For business-specific strategy, see our guide on infinite banking for business acquisition.

Major Purchases

Vehicles, education, home improvements — any major purchase you’d normally finance through a bank or pay cash for. With infinite banking, you avoid the bank’s interest spread and avoid the opportunity cost of draining your savings. Your capital keeps compounding while you use it.

Choosing the Right Company

Not every insurance company is suited for infinite banking. You need a mutual company with a long dividend payment history, flexible paid-up additions options, and access through independent agents who understand IBC policy design — not traditional insurance salespeople focused on death benefit.

Based on our analysis of 47+ whole life carriers, the most critical factors aren’t what most people expect. Policy design matters more than company selection, and agent expertise matters more than dividend rates. A poorly designed policy from the top-ranked company will underperform a properly structured policy from a lower-ranked carrier.

For our complete analysis — including company rankings, side-by-side comparisons, and what to ask any agent before working with them — see our Top 10 Best Infinite Banking Companies for 2026.

Is Infinite Banking Right for You?

Infinite banking is a powerful strategy, but it isn’t for everyone — and we’re the first to say so.

It requires stable income, a minimum commitment of roughly $500/month (or 10% of gross income), financial discipline to repay policy loans consistently, and a 7+ year timeline before the strategy hits its stride. If you need every dollar liquid right now or you’re looking for stock-market-beating returns from a life insurance policy, this isn’t your strategy.

But if you’re looking for a system that gives you control of your capital, tax-free access, guaranteed growth, and a death benefit that transfers wealth to the next generation — it’s infrastructure worth building.

Based on our experience, 90% of infinite banking “failures” trace back to poor policy design, not problems with the concept itself. The remaining 10% usually involve people who quit before year 7 or borrow without repaying.

For an honest breakdown of every advantage and limitation — including the real costs, the funding lag, the discipline required, and who should look elsewhere — see our complete pros and cons of infinite banking.

Beyond Conventional IBC: Volume-Based Banking

If infinite banking makes sense to you but you’re wondering how to push it further, two distinct paths open up. Volume-Based Banking is the methodology our team developed for maximizing what infinite banking can do within a single lifetime, pushing more capital through the system, accelerating the compounding cycles, and turning your policy into true financial infrastructure. The covenantal trust is the structure that takes infinite banking from a single-lifetime tool to a multigenerational one, building the legal envelope and the family bank mechanism that lets the structure compound across your children and grandchildren rather than ending with you.

Volume-Based Banking optimizes 100% of your cash flow within your lifetime. The covenantal trust extends the structure beyond it.

[Discover Volume-Based Banking →] [Read the covenantal trust guide →]

Frequently Asked Questions About Infinite Banking

What is the Infinite Banking Concept?

The Infinite Banking Concept is a financial strategy created by Nelson Nash that uses dividend-paying whole life insurance from a mutual insurance company as a personal banking system. Instead of storing capital in traditional banks, you build cash value in a policy you control, borrow against it when you need capital, and your money keeps compounding even while you use it. The concept is also known as Be Your Own Bank, Bank on Yourself, Cash Flow Banking, and the Perpetual Wealth Strategy — they all describe the same core idea of controlling the banking function in your life.

How does infinite banking actually work?

You fund a properly structured whole life policy designed for maximum cash value growth. When you need capital, the insurance company lends you money using your cash value as collateral — your entire cash value balance continues earning guaranteed interest and dividends as though you never borrowed. You deploy that capital into investments, business, or major purchases, then use the returns to repay your policy loan and repeat the cycle. Each cycle builds on the last because your foundation never stops growing. For the full step-by-step process, see our guide to becoming your own banker.

Is infinite banking a scam?

No. Infinite banking is a legitimate financial strategy practiced by professionals for decades, built on dividend-paying whole life insurance from mutual companies that have been in business for 100–180 years. These carriers paid dividends through the Great Depression, two World Wars, and every financial crisis since. What makes people skeptical is usually encountering agents who pitch it as a get-rich-quick scheme or who sell traditional policies not designed for IBC. For an honest assessment of both the advantages and real limitations, see our complete pros and cons of infinite banking.

Is infinite banking better than investing in the stock market?

This is the wrong comparison — and the one conventional advisors want you to make. Infinite banking doesn’t replace your investments. It replaces your bank. Your whole life policy provides guaranteed, tax-free growth on your capital base. You then use policy loans to invest in real estate, stocks, a business, or anything else — while your cash value keeps compounding. The practitioners who build the most wealth don’t choose between IBC and the market. They use IBC to fund investments on better terms, with tax advantages and uninterrupted compounding that a brokerage account can’t offer.

How much money do I need to start infinite banking?

Many people start with $300–$500 per month and scale up as income grows. Moderate funding of $1,000–$2,000 per month allows for meaningful cash value accumulation within 3–5 years. The real question isn’t the minimum — it’s what you can commit to consistently for 7+ years. Based on our experience with 1,000+ implementations, clients who fund at 10–25% of gross income see the strongest results. For details on funding strategy and how to avoid Modified Endowment Contract status, see our implementation guide.

What type of life insurance is used for infinite banking?

Infinite banking uses dividend-paying whole life insurance from a mutual insurance company — not term, not universal life, and not indexed universal life. The policy must be specifically designed for maximum cash value growth through paid-up additions, with 60–90% of premium flowing into accessible cash value rather than insurance costs. This is a fundamentally different design than traditional whole life, which emphasizes death benefit over cash accumulation.

Which company is best for infinite banking?

There’s no universal “best” — it depends on your age, health, income, and goals. However, the company matters less than most people think. Policy design and agent expertise have a far greater impact on results than which carrier you choose. A poorly designed policy from the top-ranked company will underperform a properly structured policy from a lower-ranked one. For our complete analysis of 47+ carriers, see our Top 10 Best Infinite Banking Companies for 2026.

What’s the difference between infinite banking and velocity banking?

They’re completely different strategies solving different problems. Infinite banking uses whole life insurance to build a permanent, tax-advantaged banking system you control. Velocity banking uses a HELOC to accelerate mortgage payoff — it’s a short-term debt elimination tactic dependent on variable interest rates and lender approval. Some practitioners use both simultaneously. For a full comparison, see our guide on infinite banking vs velocity banking.

Next Steps

Get Your Personalized Infinite Banking Illustration

Before committing to any strategy, see what the numbers look like for your specific situation — not a hypothetical case study. Our team will build a custom illustration around your age, health, income, and goals.

- Custom Illustration: Real numbers from real carriers, designed specifically for banking — see your projected cash value, death benefit, and loan capacity year by year

- Independent Advice: We represent 40+ carriers as an independent agency — we find the best fit for you, not us

- Honest Assessment: Whether infinite banking fits your timeline, cash flow, and financial situation

- Lifetime Coaching: Ongoing guidance to optimize your banking system as your situation evolves

- No Obligation: Complimentary session with zero pressure to purchase

“One illustration with your own data is worth more than a hundred articles.”

— Steve Gibbs, Estate Planning Attorney & Author of The Ultimate Asset

Schedule Your Free Strategy Session →

📚 Continue Your Education

- Pros and Cons of Infinite Banking — Honest evaluation of every advantage and limitation

- How to Be Your Own Banker — Step-by-step implementation guide

- Best Infinite Banking Companies for 2026 — Company rankings and practitioner selection

- Volume-Based Banking — Why volume and velocity matter more than rate of return

- Nelson Nash & the Origins of IBC — The man behind the concept

- Whole Life Insurance Guide — Understanding the vehicle

- Infinite Banking Calculators — Run the numbers yourself