When most people hear “life insurance for children,” they picture a small policy to cover the unthinkable. That’s not what this guide is about. We’re going to show you how a properly designed whole life insurance policy for your child or grandchild becomes the foundation of a personal banking system — one that compounds tax-free for decades, funds major purchases without debt, and creates the kind of multi-generational wealth that conventional financial advice simply cannot produce.

If you’ve followed the standard playbook — 529 plans, custodial accounts, maybe a small Gerber policy from Grandma — and something still feels incomplete, you’re in the right place. There’s a reason the wealthiest families in America have been using this strategy for over a century. And there’s a reason Wall Street doesn’t talk about it.

TL;DR: Whole Life Insurance for Children

- What it really is: Financial infrastructure — not just insurance. A properly designed policy becomes your child’s personal banking system.

- How it works: Cash value grows tax-deferred, can be accessed tax-free via policy loans, and the death benefit passes tax-free to heirs.

- Why start young: A policy started at age 4-12 has 50-80 years of uninterrupted compounding. A $6,000/year 10-Pay policy can grow to over $1 million in cash value by age 65, with a death benefit exceeding $3.6 million by age 85.

- Who does this: Major U.S. banks hold billions in whole life insurance on their own balance sheets as Tier 1 capital. Wealthy families like the Rockefellers used this exact strategy to build generational wealth.

- What to avoid: Gerber Grow-Up Plans (8% loan rates, minimal cash value), child term riders (no cash value at all), and any policy not structured for maximum cash value growth.

Bottom Line: The right whole life policy for your child isn’t a cost — it’s the single most powerful wealth-building asset you can create for their future, and it only gets more efficient with time.

Why Trust This Guide

This guide was written by the advisory team at Insurance & Estates, which includes a licensed estate planning attorney and independent advisors with over 18 years of experience designing cash value life insurance policies. We are not affiliated with any single insurance company — we have access to all major mutual carriers and recommend based on client goals, not commissions. Our approach treats whole life insurance as financial infrastructure for Volume-Based Banking, not as a product to be comparison-shopped. Every policy recommendation is backed by actuarial illustrations and tailored to the client’s specific situation. Content is fact-checked by licensed professionals and updated regularly.

Table of Contents

- This Isn’t About the Death Benefit

- Infrastructure, Not a Product: What the Wealthy Actually Do

- How a Properly Designed Children’s Policy Works

- Why Starting Young Changes Everything

- Real Policy Illustrations: What the Numbers Look Like

- Whole Life vs. Gerber vs. Child Term Rider: An Honest Comparison

- The Financial Mentoring Advantage

- The Entrepreneur’s Multi-Generational Tax Strategy

- Common Objections (and Why They Don’t Hold Water for Kids)

- How to Choose the Right Policy and Carrier

- What Your Child Can Do With This Policy

- Frequently Asked Questions

This Isn’t About the Death Benefit

Let’s get this out of the way: no parent buys life insurance for their child hoping to collect a death benefit. If that’s the only reason you’ve been given for considering children’s life insurance, you’ve been given bad advice — or incomplete advice at best.

The real purpose of whole life insurance for children is to create a living financial asset that grows in efficiency every single year. The death benefit is important — it provides an immediate estate and legacy transfer mechanism from day one — but it’s a secondary feature compared to the cash value engine that drives everything else.

Think of it this way: when you purchase a home, the roof matters — but you didn’t buy the house for the roof. You bought it because it appreciates, generates equity, provides shelter, and can be leveraged. A properly designed whole life policy works the same way. The death benefit is the roof. The cash value is the equity. And the infinite banking concept is what turns that equity into a wealth-building engine.

Key Takeaway

The best whole life insurance policy for a child is not focused on the death benefit — it is designed for maximum cash value accumulation, creating a financial asset that becomes more efficient with every passing year.

Infrastructure, Not a Product: What the Wealthy Actually Do

Here’s what most financial content won’t tell you: major U.S. banks hold billions of dollars in cash value life insurance on their own balance sheets. They classify it as Tier 1 capital — the safest asset class in banking. These institutions have unlimited access to every financial instrument on earth, and they choose whole life insurance as a core asset. That should tell you something.

The Rockefeller family didn’t build generational wealth through stock picks. They built a family banking system using whole life insurance, where each generation borrows from the system to fund businesses, investments, and real estate — then repays the system so the next generation can do the same. Walt Disney famously used a policy loan to fund Disneyland when traditional banks turned him down. JC Penney’s whole life policies saved his retail empire during the Great Depression.

This isn’t fringe advice. This is what sophisticated capital management looks like when you strip away the marketing from conventional financial products.

At Insurance & Estates, when we talk about the best whole life insurance for kids, we’re not talking about a $5,000-$50,000 Gerber policy that builds minimal cash value. We’re talking about a policy designed to act as a lifelong banking policy — the first piece of your child’s personal financial infrastructure. When this policy is integrated with Volume-Based Banking principles, it becomes a wealth-building storehouse that fundamentally changes how your child interacts with money for the rest of their life.

Beyond the Basics: Volume-Based Banking

If the concept of using whole life as infrastructure resonates with you — if you’ve sensed that conventional financial advice is missing something fundamental — our Ultimate Asset framework goes deeper into how this becomes a complete wealth-building system, not just insurance. Learn about Volume-Based Banking →

How a Properly Designed Children’s Whole Life Policy Works

The phrase “properly designed” matters enormously here. Not all whole life policies are created equal, and the difference between a policy designed for death benefit and one designed for maximum cash value growth is the difference between a savings account and a wealth-building engine.

A properly designed policy comes from a mutual insurance company (not a stock company), uses paid-up additions to supercharge cash value growth, and is structured as a limited pay policy (typically 10-Pay) so premium payments end while the policy continues compounding for decades.

Here’s what this structure provides:

Guaranteed Cash Value Accumulation

The policy accumulates cash value from day one — a guaranteed, contractual obligation from the insurance company. Unlike market-based accounts, this growth doesn’t depend on economic conditions, stock performance, or government policy changes. The compounding effect means the cash value grows exponentially over time, becoming more and more efficient as your child ages.

Here’s the critical advantage for children: because the cost of insurance is incredibly low for a young, healthy child, a much higher percentage of every premium dollar goes directly into cash value. This is why a policy started at age 4 dramatically outperforms one started at age 35, even if the 35-year-old contributes more annually.

And thanks to the mechanics of whole life, even when a life insurance loan is taken against the cash value, the entire cash value continues to earn interest and dividends. The compounding is never interrupted. This is one of the most misunderstood and underappreciated features in all of finance.

Guaranteed Level Premiums

Your child’s premiums are fixed at issue and will never increase regardless of future health changes, occupation, or lifestyle. When structured as a limited pay policy (such as 10-Pay), premiums are paid for a defined period, after which the policy is fully paid up. No more premium payments are ever due, but the cash value and death benefit continue growing for the rest of your child’s life.

Guaranteed Death Benefit That Grows

The initial death benefit is guaranteed from day one. But with a properly structured participating policy, the death benefit doesn’t stay static — it increases over time as dividends purchase additional paid-up insurance. A policy that starts with an $800,000 death benefit for a 4-year-old can grow to over $5 million by age 85, creating a powerful legacy transfer mechanism for your children’s children.

Tax Advantages (Triple Tax-Free)

This is where properly designed whole life insurance separates itself from virtually every other financial vehicle available. Under IRC Section 7702:

First: Cash value growth is tax-deferred. Your child’s policy grows year after year without triggering any tax liability — no 1099s, no capital gains, no annual tax drag on returns.

Second: Cash value can be accessed tax-free through policy loans. Unlike a 401(k) or traditional IRA where every withdrawal triggers income tax (and potentially penalties), borrowing against cash value is a non-taxable event.

Third: The death benefit passes to beneficiaries income tax-free. This creates an immediate, tax-free estate for the next generation — something a 401(k) simply cannot do.

Compare this to what the financial industry typically recommends: tax-deferred accounts where you’ll eventually pay taxes on the harvest rather than the seed. With whole life, your child may never be taxed on this money — not on the growth, not on the access, not on the transfer.

Dividend Payments and Paid-Up Additions

Mutual insurance companies share profits with policyholders through annual dividends. While dividends are not guaranteed, the best mutual companies have paid dividends consistently for over 100 years — including through the Great Depression, the 2008 financial crisis, and COVID.

When these dividends are used to purchase paid-up additions, they supercharge both the cash value and the death benefit. Paid-up additions allow you to overfund the policy within IRS guidelines, maximizing the tax advantages while accelerating the compounding effect. This is the mechanism that transforms a good policy into an extraordinary one.

Guaranteed Future Insurability Rider

The guaranteed insurability rider allows your child to purchase additional coverage at specific ages and life events — marriage, having children, buying a home — with no medical underwriting required. This means even if your child develops health issues later in life, they have a contractual right to increase their coverage at standard rates. For a child who may one day need significantly more coverage to protect their own family, this rider is invaluable.

Key Takeaway

A properly designed children’s whole life policy provides triple tax-free treatment (tax-deferred growth, tax-free access, tax-free death benefit), guaranteed level premiums, uninterrupted compounding, and the ability to increase coverage regardless of future health — all backed by the financial strength of a mutual insurance company with 100+ years of dividend history.

Why Starting Young Changes Everything

The earlier you start a whole life policy, the more powerful it becomes. This isn’t a marginal difference — it’s exponential.

A policy started at age 4 has approximately 61 years of tax-free compounding before your child reaches traditional retirement age. A policy started at age 35 has 30 years. That’s not “a little less time” — that’s an entirely different mathematical outcome. Due to the nature of compound interest, the first few decades are where the real magic happens, and a childhood-funded policy captures all of it.

There are three specific reasons early start matters:

Cost of insurance is lowest. Because children are young and healthy, the internal cost of insurance within the policy is minimal. This means a higher percentage of every premium dollar flows directly into cash value rather than covering mortality costs. The policy is inherently more efficient.

Compounding duration is maximized. Decades of uninterrupted compound growth — with interest and dividends building on top of prior interest and dividends — creates an exponential growth curve that simply cannot be replicated by starting later, even with higher contributions.

Insurability is locked in permanently. Your child’s health today guarantees their coverage for life. No future diagnosis, lifestyle change, or occupation can affect their policy or their ability to increase coverage through the guaranteed insurability rider.

The Power of Time

Based on our illustrations from A+ rated carriers, a 10-Pay policy started for a 4-year-old with $9,355 in annual premiums (total out-of-pocket: $93,550) can grow to a cash value exceeding $1.1 million and a death benefit over $5 million by age 85. That’s the power of starting early with a properly designed policy. No other financial vehicle can guarantee this kind of outcome in a tax-free environment.

Real Policy Illustrations: What the Numbers Look Like

Theory is important, but numbers tell the real story. Below are three actual whole life insurance illustrations from A+ rated carriers, showing how properly designed children’s policies perform over a lifetime.

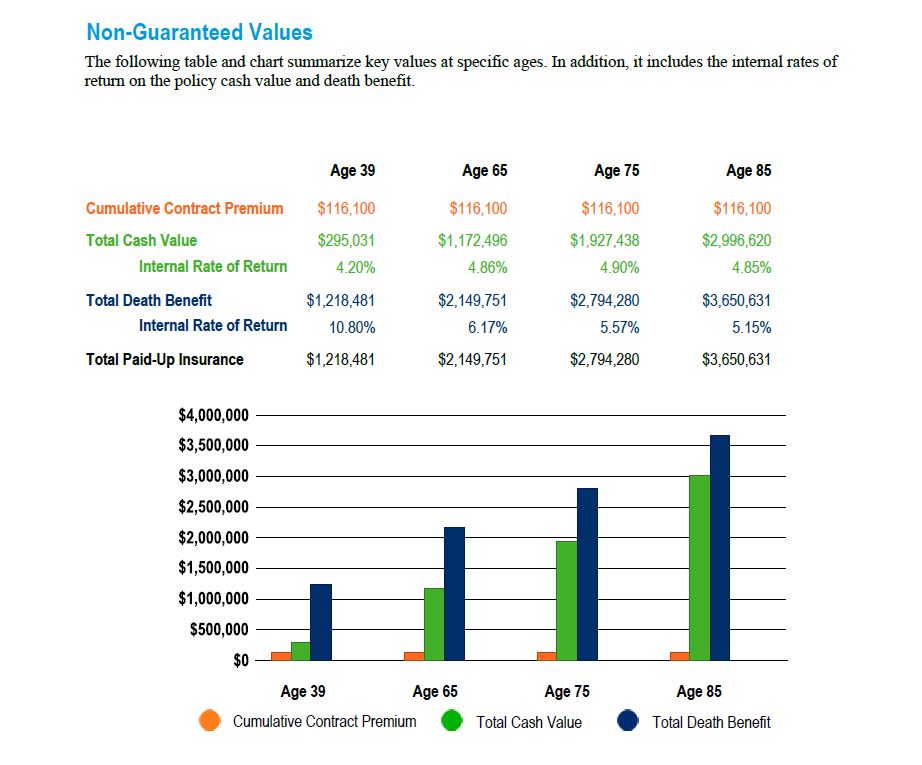

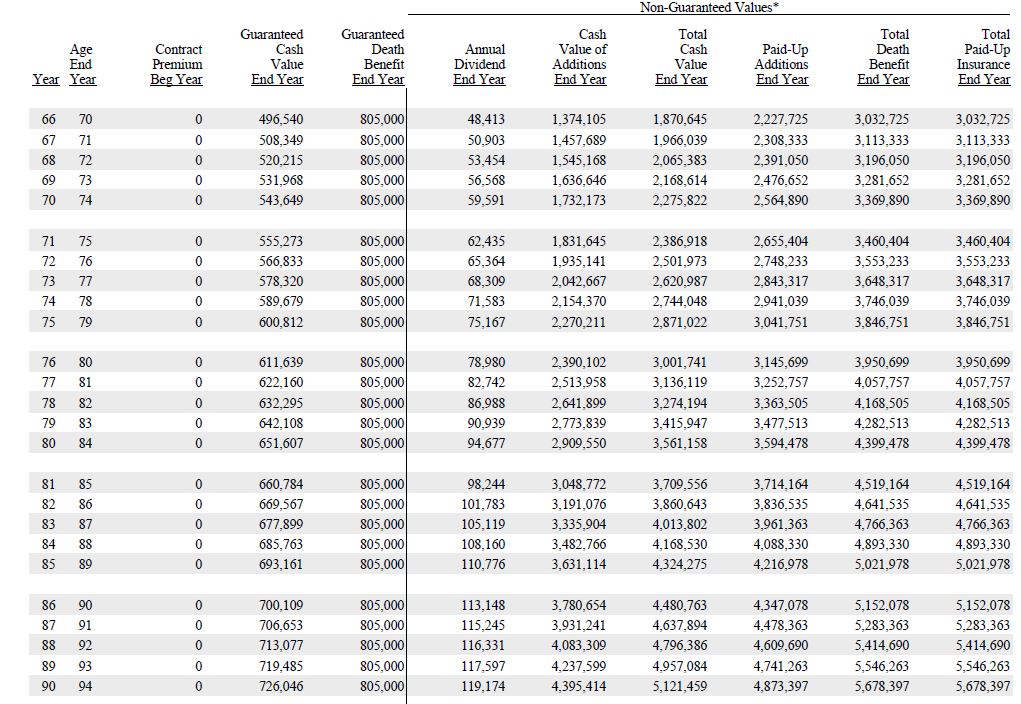

Example 1: 12-Year-Old Male, $11,610/Year 10-Pay Policy

In this illustration, a parent or grandparent contributes $11,610 annually for 10 years into a properly designed whole life policy for a 12-year-old boy. Total premiums paid: $116,100.

The results speak for themselves: $116,100 in total premiums generates over $1.1 million in cash value by age 65 and a death benefit exceeding $3.6 million by age 85. The internal rate of return on the cash value continues improving every year — a characteristic unique to whole life insurance.

THE ULTIMATE FREE DOWNLOAD

The Self Banking Blueprint

A Modern Approach To The Infinite Banking Concept

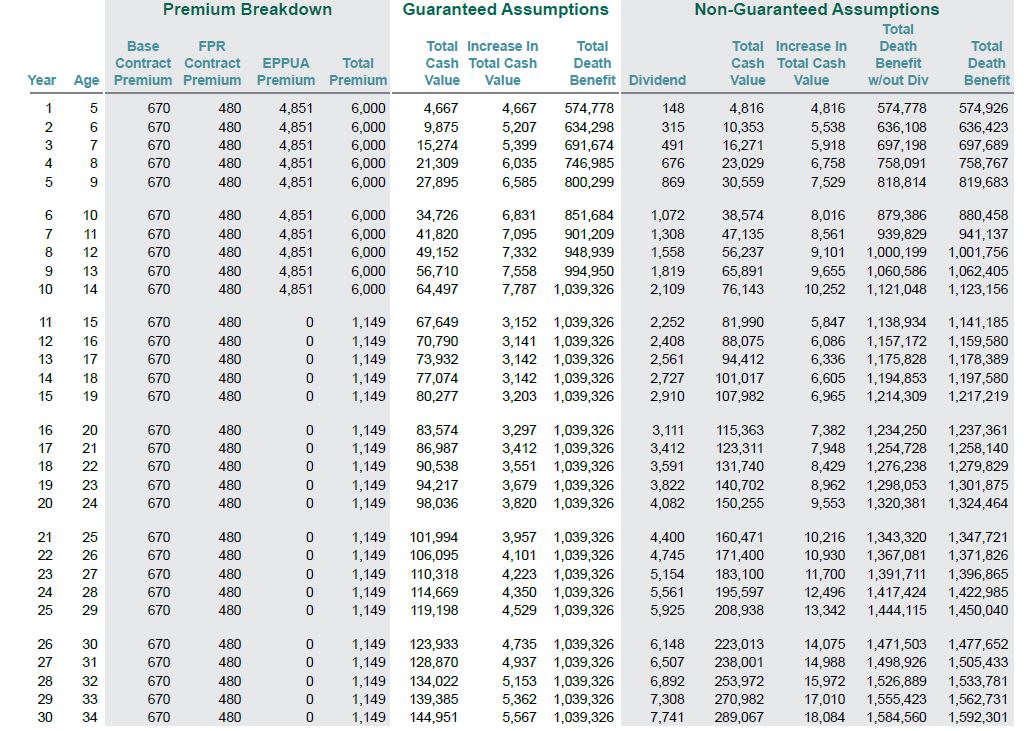

Example 2: The Entrepreneur’s Tax Strategy — $6,000/Year

This example is designed around a specific tax strategy available to business-owning families. We chose $6,000 in annual premiums for a reason:

The Entrepreneur’s Multi-Generational Tax Play

Under current tax law, a parent who owns a business can employ their child (age 12 in some states, age 14 in most) and pay them up to the standard deduction amount in income tax-free earnings. The parent gets the business write-off. The child earns income tax-free. That income can then fund a whole life insurance policy where the cash value grows tax-deferred. Down the road, the child accesses the cash value tax-free via policy loans.

The result: Money that is never taxed — not when earned, not as it grows, and not when accessed. Please consult with your tax advisor for your specific situation.

On this illustration from an A+ rated carrier, a 10-Pay whole life policy with $6,000 annual premiums is designed so that after 10 years, the dividend alone should cover any remaining premium. The policy continues growing and compounding for the rest of the child’s life with no further out-of-pocket costs.

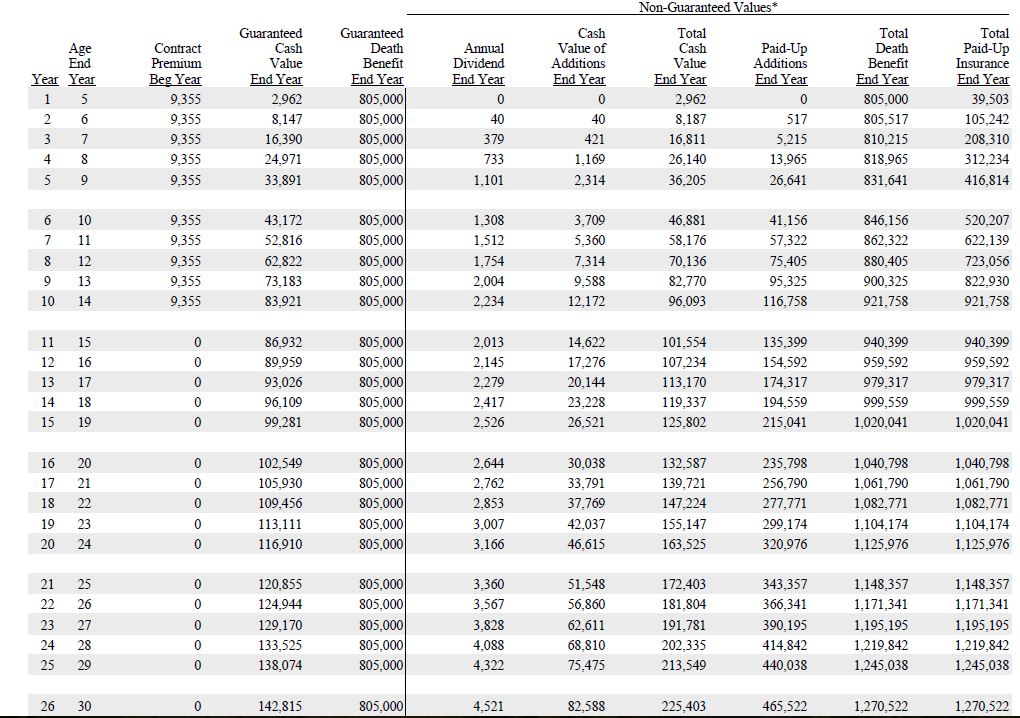

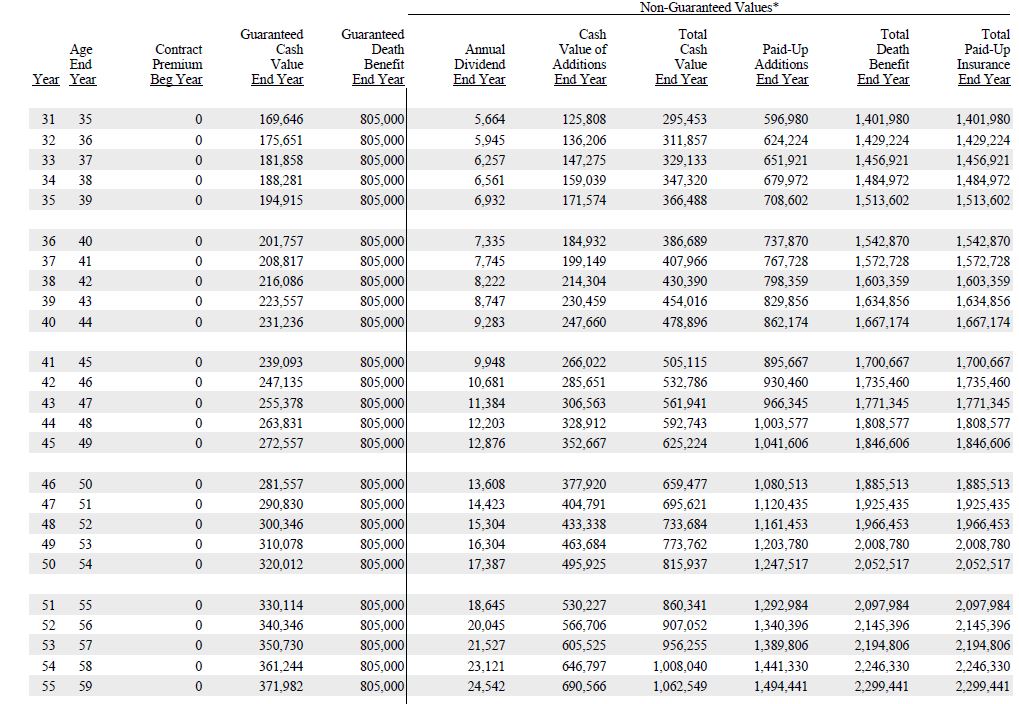

Example 3: 4-Year-Old Male, $9,355/Year 10-Pay ($800K Starting Face Amount)

This illustration shows the full power of starting as early as possible. A properly designed 10-Pay whole life policy for a 4-year-old boy with a guaranteed insurability rider, issued by an A+ rated carrier, with a focus on maximum cash value growth.

Starting face amount: $800,000. Annual premium: $9,355 for 10 years. Total premiums paid: $93,550. After year 10, no more premiums are due.

The policy runs to age 121, at which point the non-guaranteed totals project over $21,000,000 in combined cash value and death benefit.

Ages 5-30

Ages 35-59

Ages 66-90

Whole Life vs. Gerber Grow-Up Plan vs. Child Term Rider: An Honest Comparison

Most parents and grandparents considering life insurance for children end up choosing between three options: a properly designed whole life policy, the Gerber Grow-Up Plan, or a child term rider attached to a parent’s policy. These are fundamentally different products designed for fundamentally different purposes.

| Feature | Properly Designed Whole Life | Gerber Grow-Up Plan | Child Term Rider |

|---|---|---|---|

| Primary Purpose | Financial infrastructure / banking policy | Forced savings with death benefit | Death benefit only |

| Cash Value Growth | ✓ Maximized via paid-up additions | Minimal | ✗ None |

| Policy Loan Rate | ~5% (wash loan with dividends) | 8% | N/A |

| Coverage Amount | No maximum limit | $5,000 – $50,000 | Typically $10,000 – $25,000 |

| Dividends | ✓ Annual dividends from mutual company | ✗ No dividends | ✗ No dividends |

| Paid-Up Additions | ✓ Available (supercharges growth) | ✗ Not available | ✗ Not available |

| Guaranteed Insurability Rider | ✓ Available | Limited (can buy more at adult rate) | May convert at age 25 |

| Death Benefit Growth | ✓ Increases over time via dividends | Doubles at 18, then static | ✗ Static, expires at age 25 |

| Infinite Banking / VBB Capable | ✓ Yes — designed for this | ✗ No (insufficient cash value, high loan rates) | ✗ No (no cash value) |

| Risk Level | Guaranteed (contractual) | Guaranteed (but limited upside) | Expires — coverage risk after 25 |

| Best For | Families building generational wealth and financial infrastructure through Volume-Based Banking | Grandparents wanting an affordable gift with basic coverage | Parents who only need temporary death benefit coverage for a child |

Note: “Properly designed” refers to a participating whole life policy from a mutual insurance company, structured with paid-up additions for maximum cash value growth. Gerber Life is underwritten by Gerber Life Insurance Company. Individual results vary based on carrier, policy design, and premium amount. Dividends are not guaranteed.

The bottom line: the Gerber Grow-Up Plan is well-marketed, but it lacks the structural features necessary for meaningful wealth building. Its 8% loan rate alone makes it impractical for banking purposes compared to the ~5% wash loan rates available from top dividend-paying mutual companies. A child term rider is even more limited — it provides death benefit only, builds zero cash value, and expires when your child enters adulthood.

We do not advocate either the Gerber Grow-Up Plan or child term riders as viable options for families serious about building their child’s financial foundation.

Important Consideration

If you are going to add a child rider to a parent’s policy, choose a mutual company with a rider that can convert to a properly designed permanent policy for maximum cash value growth. The conversion option is where the real value lies — not the rider itself. See our guide on the best convertible term life insurance companies.

The Financial Mentoring Advantage

Here’s a statistic that should concern every parent thinking about generational wealth: research consistently shows that wealth evaporates by the third generation in the vast majority of families. The reason isn’t poor investments or bad luck — it’s because previous generations failed to pass down sound financial principles alongside the wealth itself.

A properly designed whole life policy solves both problems simultaneously. It creates the financial asset and the teaching tool.

When you purchase this policy for your child, you’re not just making a financial decision — you’re creating a hands-on financial education that lasts their entire childhood. Every year, you can review the annual statement together. You can show them how cash value grows, how dividends work, how compound interest operates in a real (not hypothetical) environment. By the time they’re 18, they don’t just inherit a financial asset — they understand how to manage it like a banker, not a consumer.

This is fundamentally different from handing a young adult a brokerage account or 529 balance and hoping they manage it well. The policy itself teaches the principles of banking, compounding, and strategic capital deployment through lived experience.

Your role as a parent doesn’t end at purchasing the policy. The real value is in mentoring your child to understand and leverage their policy to fund their ambitions without falling into the debt traps that define most people’s financial lives. You’re not just giving them money — you’re giving them a different relationship with money entirely.

The Entrepreneur’s Multi-Generational Tax Strategy

For business-owning families, whole life insurance for children presents a tax strategy that is remarkably powerful when structured correctly.

Under current tax law, a parent who operates a business can employ their child (age 12 in some states, age 14 in most) and pay them up to the standard deduction amount — currently around $14,600 — in income tax-free earnings. The parent receives the business deduction. The child earns income with zero federal income tax liability.

That tax-free income can then fund a whole life insurance policy where the cash value grows tax-deferred. Years later, the child accesses the accumulated cash value tax-free through policy loans.

Follow the money: earned tax-free, grows tax-deferred, accessed tax-free, and ultimately transferred via death benefit income tax-free to the next generation. This is a legitimate, multi-generational tax strategy that operates entirely within the existing tax code. Please consult with your tax advisor regarding your specific situation.

For a deeper look at the tax framework behind this strategy, see our guide on IRC 7702 plans explained and our analysis of the three tax buckets.

Common Objections (and Why They Don’t Hold Water for Kids)

You’ve probably heard financial commentators criticize whole life insurance. Some of these objections have merit in certain contexts — but they are particularly misguided when applied to children’s policies. Here’s why:

“Whole life has high fees.” This objection is typically raised by professionals pushing their own fee-based products (the irony is rarely acknowledged). Yes, there are startup costs — just as there are when purchasing real estate or funding a business. But a child’s policy has decades to overcome initial costs and compound. By year 10-15, the internal rate of return on a properly designed policy is competitive with any safe-money alternative, and it only improves from there. Unlike market-based products, there are no ongoing management fees, trading costs, or advisory fees eroding returns year after year.

“You should buy term and invest the difference.” This is perhaps the most commonly repeated advice in personal finance, and it fundamentally misunderstands what we’re building here. We’re not comparing insurance products — we’re comparing financial systems. Term insurance provides a temporary death benefit with zero wealth-building capability. A properly designed whole life policy provides permanent coverage, guaranteed cash value, tax-free access, and a banking infrastructure your child uses for life. For a thorough analysis of this debate, see our guide on buy term invest the difference and whole life vs. term life.

“The rate of return is too low.” This objection compares apples to oranges. Whole life cash value provides a guaranteed, contractual return in a tax-free environment with zero market risk. The cash value chart on a child’s policy shows internal rates of return that are remarkably competitive when you factor in guarantees, tax treatment, and the absence of ongoing fees. Compare that to tax-deferred accounts where you’ll pay income tax on every dollar of growth upon withdrawal. The after-tax, after-fee, risk-adjusted comparison is not even close for many families.

“Just open a 529 or savings account.” A 529 plan serves one purpose: education expenses. A custodial account has limited tax advantages and no asset protection. Neither provides a death benefit, guaranteed growth, or a banking mechanism. They are tools — useful in their specific lane — but they are not infrastructure. See our comparison of alternatives to traditional retirement vehicles for a broader framework on how these tools fit together.

Key Takeaway

Most objections to whole life insurance are based on adult-centric analysis that ignores the unique advantage children have: time. A child’s policy has 50-80 years to compound, making the startup cost objection functionally irrelevant. The relevant question isn’t “what’s the year-one return?” — it’s “what financial system do I want my child to have at age 30, 50, and 70?”

How to Choose the Right Policy and Carrier

Choosing the right carrier and policy structure is the single most important decision in this process. Not all whole life policies are designed the same way, and a policy from the wrong company — or one designed with the wrong priorities — can underperform for decades.

Here’s what to look for:

Mutual insurance company. A mutual company is owned by its policyholders, not shareholders. This means profits are returned to you as dividends rather than paid out to Wall Street investors. This is non-negotiable for a policy designed around cash value growth.

Strong dividend history. Look for companies with 100+ years of consistent dividend payments. Past performance doesn’t guarantee future results, but a century of dividend payments through wars, depressions, and financial crises tells you something about the company’s financial management.

Participating policy with paid-up additions. The policy must be a participating policy that allows dividend reinvestment through paid-up additions. This is the mechanism that supercharges cash value growth beyond the guaranteed rate.

Properly structured for cash value (not death benefit). Many agents design policies to maximize the death benefit (which maximizes their commission). A policy designed for maximum cash value growth looks very different — it uses paid-up additions riders, blended designs, and careful structuring to push as much premium as possible into the cash account while staying within MEC limits.

Competitive loan rates. Since the banking function depends on policy loans, look for carriers offering non-direct recognition or competitive wash loan rates around 5%. This is where Gerber’s 8% loan rate becomes a dealbreaker for anyone planning to use the policy as infrastructure.

Financial strength ratings. Choose a carrier rated A+ or higher by AM Best. See our guide to the top 25 highest rated insurance companies and our top 10 best life insurance companies for specific carrier analysis.

For detailed reviews of specific carriers we work with, see our reviews of Penn Mutual, MassMutual, New York Life, Guardian, Lafayette Life, and Northwestern Mutual.

What Your Child Can Do With This Policy

Starting a whole life insurance policy for your child early creates a substantial personal banking system they can draw on throughout their entire adult life. With proper financial education and mentorship, your child can borrow against the cash value for virtually any purpose while the full balance continues earning interest and dividends:

Your Child’s Personal Banking System Can Fund:

- Education — without student loan debt

- First vehicle — paying yourself back instead of a bank

- Starting a business — with no credit check and no approval process

- Wedding expenses — without credit card debt

- Down payment on a home — while cash value keeps compounding

- Investment opportunities — deploying capital when opportunities arise, on their terms

- Emergency fund — always liquid, always accessible

- Retirement income — tax-free supplemental income for life

The critical difference: every dollar your child borrows from their policy continues to earn interest and dividends in the policy. Unlike a bank withdrawal or 401(k) distribution, the compounding is never interrupted. This is the principle that makes being your own bank so powerful — and it’s why starting in childhood is the ultimate advantage.

For families building long-term wealth strategies, this policy also integrates with broader estate planning objectives, including irrevocable life insurance trusts and wealth-building strategies using cash value life insurance.

A Note for Grandparents

Grandparents are often the ones who initiate these policies, and for good reason. If you’re looking for a gift that lasts a lifetime — one that actually builds wealth rather than collecting dust — a properly designed whole life policy is difficult to beat.

For a dedicated guide on this topic, including specific strategies and illustrations for grandparent-funded policies, see our complete guide to life insurance for grandchildren.

Conclusion

Purchasing whole life insurance for your child isn’t about buying an insurance product. It’s about building the first piece of financial infrastructure that will serve them for their entire life — infrastructure that compounds tax-free, provides tax-free access to capital, creates an immediate estate, teaches financial principles through hands-on experience, and ultimately transfers wealth to the next generation without the IRS taking a cut.

The wealthiest families in America have understood this for generations. Major banks hold billions in whole life insurance because the math works. The question isn’t whether this strategy is sound — it’s whether you’re going to use it for your family.

If you’re ready to stop comparison-shopping small policies and start building real financial infrastructure for your child’s future, we’re here to help you design it correctly.

Build Your Child’s Financial Infrastructure

Our independent advisory team designs whole life policies specifically for maximum cash value growth — not death benefit. We’ll walk you through the illustrations, explain the mechanics, and show you exactly how a properly structured policy becomes the foundation of your child’s wealth-building system.

- ✓ Personalized illustration from A+ rated mutual carriers

- ✓ Policy design focused on maximizing lifetime cash value

- ✓ Integration with Volume-Based Banking and estate planning strategies

- ✓ Full analysis of the entrepreneur tax strategy for business-owning families

Schedule your complimentary 30-minute strategy session and see what the numbers look like for your child.

No obligation. No sales pressure. Just expert guidance from an independent advisory team with access to all major mutual carriers.

THE ULTIMATE FREE DOWNLOAD

The Self Banking Blueprint

A Modern Approach To The Infinite Banking Concept

Frequently Asked Questions About Whole Life Insurance for Children

Is whole life insurance for children worth it?

It depends on what you’re buying and why. A small Gerber policy or child term rider? Marginally useful at best. A properly designed, high-cash-value participating whole life policy from a mutual insurance company? Based on our experience designing hundreds of these policies, it is one of the most powerful wealth-building tools available for children — combining guaranteed cash value growth, triple tax-free treatment, uninterrupted compounding, and a banking function your child can use for their entire life. The key is proper policy design focused on cash value, not death benefit.

How much does whole life insurance for a child cost?

Premiums vary based on the child’s age, the coverage amount, and the policy design. A properly designed 10-Pay policy might range from $3,000-$12,000+ per year depending on your goals. The younger the child, the lower the cost of insurance, which means more of every premium dollar goes directly into cash value. See our whole life insurance cost guide and rates by age chart for detailed breakdowns.

What type of life insurance is best for children?

A participating whole life insurance policy from a mutual insurance company, structured with paid-up additions for maximum cash value growth and designed as a limited pay policy (such as 10-Pay). This structure provides guaranteed cash value, dividends, tax-free access via policy loans, and a growing death benefit — the complete foundation for a personal banking system. Term insurance and non-participating whole life policies lack the cash value and banking features that make this strategy worthwhile.

Is the Gerber Grow-Up Plan a good investment for my child?

The Gerber Grow-Up Plan provides basic whole life coverage at affordable premiums and is heavily marketed to grandparents. However, it builds minimal cash value, does not participate in dividends, charges an 8% loan rate (compared to ~5% from top mutual carriers), and cannot be used effectively as a banking policy. For families whose goal is building meaningful financial infrastructure for their child, a properly designed policy from a top-rated mutual company will significantly outperform the Gerber plan over a lifetime. Read our full Gerber Grow-Up Plan review.

Can my child use the cash value in the policy?

Yes. Once the child reaches the age of majority and ownership transfers, they can borrow against the cash value tax-free for any purpose — education, a vehicle, starting a business, a home down payment, investments, or retirement income. The critical advantage is that the entire cash value continues earning interest and dividends even while borrowed against, so the compounding effect is never interrupted.

What are the tax advantages of whole life insurance for kids?

Whole life insurance for children offers triple tax-free treatment under IRC Section 7702: cash value grows tax-deferred, policy loans provide tax-free access to funds, and the death benefit passes to beneficiaries income tax-free. For business-owning families, children can also earn income tax-free through parental employment and fund the policy with those earnings, creating a scenario where the money may never be taxed at any point.

How is whole life insurance for children different from a 529 plan or savings account?

A 529 plan is limited to qualified education expenses and is tied to market performance. A savings account offers minimal returns with no tax advantages. Whole life insurance provides guaranteed growth, tax-free access for any purpose (not just education), a growing death benefit, creditor protection in most states, and a banking mechanism that allows your child to borrow against the cash value while it continues compounding. They serve different purposes and can complement each other, but whole life provides the infrastructure that other vehicles lack.

What is a “properly designed” whole life policy for a child?

A properly designed policy comes from a mutual insurance company (not a stock company), is structured as a participating policy with dividends, uses paid-up additions to maximize cash value growth, is designed to stay within MEC limits, and includes a guaranteed insurability rider. The policy is designed by an advisor who understands infinite banking mechanics and structures for cash value, not commission.

What happens to a child’s whole life policy when they turn 18?

When the child reaches the age of majority (typically 18), ownership of the policy can transfer to them. If the policy is structured as a 10-Pay, premiums may already be fully paid, meaning the child inherits a fully paid-up, compounding financial asset with no ongoing costs. They then manage the policy’s cash value as their personal banking system for the rest of their life, with the option to increase coverage through the guaranteed insurability rider at life milestones.

Which companies offer the best whole life insurance for children?

The best carrier depends on your specific goals, premium level, and desired policy structure. We work with all major mutual carriers and recommend based on which company offers the best illustration for your situation. Some of the top companies for infinite banking and children’s policies include Penn Mutual, Guardian, MassMutual, New York Life, and Lafayette Life. The right answer requires a personalized illustration — not a ranking list. See our top life insurance companies guide for detailed analysis.

7 comments

May

Is there a cap amount on the face value for our children? One example you used was an 800K on year 1 for the 9K premium. You can do it that high? Thought I was told it can only be so much in comparison to why my policies are, but maybe I misunderstood. thoughts?

Insurance&Estates

Hello May, your question have been forwarded to our product expert Jason Herring and you can also reach out directly to him at jason@insuranceandestates.com.

Best, I&E

lucy

how to choose the right life insurance for 5/11 children ?

Angela

Very interesting article. I’m interested in whole life protection for my grandsons, ages 2, 3, and 4. The article provides much food for thought but I was hoping to see a list of top insurance companies that you would recommend.

Derek

Great article! Once you have a policy set up for your kid, you own the policy and therefore you control the policy, correct? In other words, you can use the banking features just like a policy taken out on yourself, and then you can choose to sign over the policy when your kid is a certain age – if you choose – or you can control it until you die, if that was what you decided to do, right? In other words, even though your kid is the insured, you have complete control as the owner until you relinquish control through paperwork filed with the insurance company giving ownership to someone else (e.g., your kid). Thanks!

Tal S.

Great article…So what are the best high cash value whole life policies for children? Mine are 5, 7, and 14.

Insurance&Estates

Hi Tal,

Thank you for the question. Please be on the lookout for our reply to the contact info you provided.

All the best,

I&E