While many people purchase whole life insurance for the death benefit that it provides, there are other features that can make these flexible financial vehicles enticing, too. For instance, with permanent dividend paying whole life insurance policies, there is a cash value account where the funds are allowed to grow on a tax-deferred basis.

This cash value accumulation, in turn, could be used as an additional retirement savings vehicle and/or source of liquidity for emergencies, higher-interest debt payoff, or even supplementing retirement income.

It is important to know the pros and cons of whole life insurance policies because not all policies are the same, and neither are the insurance companies that offer them. So, it is important to understand how different categories of insurers work, and why one may be more beneficial than another.

Click the following to jump to the ↪section on the top mutual insurance companies.↩

Mutual versus Stock Insurance Companies

Most whole life insurance companies are as either stock or mutual. (There are a few exceptions called fraternal insurers). These categories are dependent on how the companies are owned. Both stock and mutual insurance companies earn income by collecting premiums from their policy holders. But the investing strategies of the companies can differ.

Stock Insurance Companies

Stock insurance companies are “owned” by their stockholders. A stock insurer may earmark its profits to pay off debt and/or to reinvest in the company. Like companies in other industries, though, another goal of a stock life insurance companies is to generate a profit for their shareholders.

As such, stock insurers tend to have more of a focus on shorter-term results with higher-yielding – and oftentimes potentially riskier – assets. In the case of stock insurers, the customers (i.e., the policyholders) do not share directly in profits (or losses) that are attained by the company.

There are more stock insurance companies at this time than there are mutual insurers in the United States. (Although, this is not the case worldwide). Some of these stock companies include:

- MetLife

- Prudential

- Allstate

- Ohio National

There are pros and cons to stock insurance companies. Some of the benefits can include:

- Their ability to raise money quickly. When a stock insurance company needs capital, it can typically just issue more shares of stock.

- These insurers are oftentimes able to “unlock” value and access new sources of capital. This can in turn make it easier to fund rapid growth.

- Source

On the downside, however, stock insurers do not always put their customers (i.e., policy holders) interests’ first. Rather, they are generally in business to cater to their stockholders – who are a significant source of capital for the companies.

As a policy holder of a stock insurance company, then, you won’t receive policy dividends like you could through a mutual insurer. These dividends instead are paid out to the company’s stockholders.

Mutual Insurance Companies

Mutual insurance companies are essentially owned by their policyholders. That means that the policyholders have a right to vote on the board of directors, as well as to share in the company’s profits. In fact, the sole purpose of mutual insurance companies is to provide insurance coverage for its policyholder members.

The first mutuals came about in the late 17th century in England. Benjamin Franklin established the Philadelphia Contributionship for the Insurance of Houses From Loss by Fire as the first U.S. mutual insurer in 1752.

These types of insurers invest in portfolios that may contain mutual funds. The profits that are returned to policyholders of mutual whole life insurance companies can come in the form of dividends or reduction in policy premiums.

Not all policies that are offered by mutual insurance companies pay dividends to the policy holders, though. While dividends are actually never guaranteed, permanent participating policies – which are also oftentimes referred to as “par” policies – allow policy holders to participate in the profits of the insurance company.

There are several different ways that dividends from a whole life insurance policy may be received, including:

- Direct cash payment

- An addition to the cash value of the policy (which can add to the tax-deferred growth in the account)

- As payment to purchase additional paid up life insurance coverage

Because mutual insurance companies are not traded on stock exchanges, they do not have to be quite as “aggressive” on having to reach short-term profit targets for their shareholders. With that in mind, mutual insurers can instead focus more on attaining longer-term benefits by investing in less risky assets.

Unlike stock insurance companies, mutual insurers are not listed on stock exchanges. However, should a mutual company convert over to being a stock company – in a process that is known as “demutualization” – that could change. It is up to federal law to determine whether or not an insurance company may be a mutual insurer.

Mutual versus Stock Life Insurance Companies

| Mutual Life Insurance Companies | Stock Life Insurance Companies |

|---|---|

| Company is owned by its policy holders | Company is owned by its stockholders |

| Policy holders have the right to vote on the company’s management | Stockholders vote on the company’s Board of Directors and management team |

| Raise capital by issuing debt or borrowing from policy holders | Raise capital by issuing more shares of stock |

| Pay dividends to policy holders (note that dividend payments are not guaranteed) | Profits typically go to shareholders in the form of dividends and/or increased stock price |

| Invest in less risky assets with more of a long-term profit goal | Invest in riskier assets with a focus on short-term profits for shareholders |

| Share the profits of the company with policy holders in the form of dividends and/or lower premiums on policies | Share the profits with stockholders, oftentimes in the form of stock dividends |

Top 8 Mutual Life Insurance Companies

Although some mutual whole life insurance companies have “demutualized” over the past couple of decades, there are still many large, financially stable mutual life insurance companies in the marketplace. Many of these have been in the industry for more than a century, and have a long history of paying out consistent dividends to policy holders throughout the years.

The top mutual insurers operating in the United States include the following:

Penn Mutual Life Insurance Company

New York Life Insurance Company

The Guardian Life Insurance Company of America

Penn Mutual Life Insurance Company

![]()

![]() Penn Mutual was initially founded, chartered, and opened for business in Philadelphia in 1849. It was in that same year that the company declared its very first dividend. By 1920, the company’s life insurance in force reached $1 billion.

Penn Mutual was initially founded, chartered, and opened for business in Philadelphia in 1849. It was in that same year that the company declared its very first dividend. By 1920, the company’s life insurance in force reached $1 billion.

There are a number of insurance and financial product offerings available through Penn Mutual, including:

- Whole life insurance

- Survivorship whole life

- Indexed universal life

- Survivorship indexed universal life

- Variable universal life / Protection universal life

- Guaranteed universal life

- Current assumption universal life

- Convertible term life

- Non-convertible term life

- Variable annuities

- Fixed annuities

- Single premium immediate annuities (SPIAs)

- Indexed annuities

Penn Mutual has consistently paid out dividends to its whole life insurance policyholders for decades, with a dividend of 5.75% declared for 2022. As of the end of the third quarter of 2021, the company held nearly $25 billion in total assets. Source.

Penn Mutual is considered to be strong and stable financially and it has a good reputation for paying out its policy holders’ claims. This is reflected in the high ratings the company has received from the rating agencies.

Penn Mutual Life Insurance Company Ratings

Penn Mutual’s A+ Superior rating, which was reaffirmed in March 2021, ranks the second highest out of 15 possible ratings.

A+ (Strong) from Standard & Poor’s

Penn Mutual’s Strong rating, which was reaffirmed in December 2021, ranks fifth out of 22 possible ratings.

Penn Mutual’s Aa3 High Quality rating, which was reaffirmed in April 2021, ranks the fourth highest out of 21 possible ratings.

AA (Very High Quality) from Kroll Bond Rating Agency

Penn Mutual’s AA Very High Quality rating, which was reaffirmed in November 2021, ranks the third highest out of 22 ratings, and includes a stable outlook.

Source: Penn Mutual Life Insurance. https://pennmutual.com/about-us/financial-strength/ratings

In addition to its strong financial ratings, Penn Mutual Life Insurance Company has also earned a score of 93 (out of 100) on the Comdex Life Insurer Financial Profile. This reflects the insurer’s excellent standing within the life insurance industry.

Lafayette Life

![]()

![]() For more than 115 years, The Lafayette Life Insurance Company has provided life insurance, annuity, retirement and business planning solutions to individuals, families, and small to medium sized businesses.

For more than 115 years, The Lafayette Life Insurance Company has provided life insurance, annuity, retirement and business planning solutions to individuals, families, and small to medium sized businesses.

The products and financial vehicles that are offered through Lafayette Life include both term and whole life insurance policies, as well as immediate and fixed indexed annuities.

Lafayette Life is a member of Western & Southern Financial Group, a Cincinnati-based diversified family of financial services companies. Initially started in 1905, the company is today on the Fortune 500 list.

Even given the many challenges that were faced in 2020 – including the COVID-19 pandemic and a highly volatile stock market and economy – Lafayette Life prevailed financially.

Annualized sales in life insurance premiums grew 30%, and the sale of new policies increased 45% over the previous year. In addition, the operating income from the life insurance and annuity business at Lafayette Life reached a record $61.4.

Lafayette Life is built on a good, solid foundation of financial strength, along with offering quality products and services, as well as a commitment to excellence. For year-end 2020, the company held total invested assets in excess of $6.4 billion, and total assets of $6.510 billion.

With total revenue of over $684 million, Lafayette Life amassed policy holder benefit payments, interest credited, and paid dividends to policy holders in the amount of just under $548 million in total. Source.

Because it is there when its policy holders and beneficiaries need this company, Lafayette Life has earned high ratings from the insurer ratings agencies. These ratings include a(n):

The Lafayette Life Insurance Company Financial Strength Ratings

| Agency | Rating |

|---|---|

| A.M. Best | A+ (Superior) |

| Standard & Poor’s | AA- (Very Strong) |

| Fitch | AA (Very Strong) |

| Comdex Ranking | 96 out of 100 |

Source: Lafayette Life. Company Ratings. Financial Strength. https://www.westernsouthern.com/-/media/files/lafayette/ll-2290.pdf

In keeping with the company’s tradition of paying out dividends on its whole life policies – which it has done consistently since its founding in 1905 – Lafayette Life also expensed record dividends of $73.3 million in 2020. (At that time of this resource, Lafayette Life anticipated 2021 figures to be in the same or similar range).

Foresters Financial Insurance Company

![]()

![]() For nearly 100 years, Foresters Financial has been helping families build and protect their financial security. This company was initially founded in 1874, when Foresters set out to provide access to life insurance to average, working families.

For nearly 100 years, Foresters Financial has been helping families build and protect their financial security. This company was initially founded in 1874, when Foresters set out to provide access to life insurance to average, working families.

Today, the company has approximately 3 million clients and members in the United States and Canada, as well as in the United Kingdom. Throughout the past century and a half, Foresters Financial has remained true to its commitment to help improve family wellbeing.

With that in mind, every year the company invests millions of dollars that go towards supporting causes that enrich the lives of families and communities.

Products that are offered through Foresters include the following:

- Term life insurance

- Whole life insurance

- Universal life insurance

Just some of the financial highlights for the year 2020 include:

- Total Annualized Weighted Sales (in the United States) of $85 million

- Total Annualized Weighted Sales (in Canada) of $62.2 million

- Total Annualized Weighted Sales (in the United Kingdom) of 48.0 lira

- Total Premiums generated of $1.2 billion

- Certificates and Contracts in Force of 2.8 million

Foresters is known for its strong financial foundation, as well as its positive reputation for being there when policy holders and beneficiaries are ready to make good on their claims. Due in large part to these factors, the company has earned a financial strength rating of A from A.M. Best. Source.

Ever since the year 1874, Foresters has had a history of regularly paying a dividend to its policy holders. In 2021, the company announced a $24.4 million dividend payout for the year 2020, for its participating U.S. certificate holders. This figure was consistent with the $24.4 million that had been disbursed in 2019. The dividend rate for 2020 was 5.8%.

Even during a year of uncertainty – due to the COVID-19 pandemic and economic turmoil – this mutual whole life insurance provider continued to “reward” its policy holders / owners with the continuation of dividend payments.

MassMutual

![]()

![]() MassMutual whole life insurance is one of our favorites. The company has been helping individuals and families grow and protect wealth since 1851. The company has always been managed with a focus on long-term interests and stable, conservative growth.

MassMutual whole life insurance is one of our favorites. The company has been helping individuals and families grow and protect wealth since 1851. The company has always been managed with a focus on long-term interests and stable, conservative growth.

MassMutual offers a wide range of financial products and services, including:

- Life Insurance (term, whole life, universal life, and variable universal life insurance coverage)

- Disability income insurance

- Long-term care coverage (as well as combination life insurance / long-term care)

- Annuities (fixed, indexed, and variable annuities)

- Individual Retirement Accounts

- Mutual Funds

- Exchange Traded Funds (ETFs)

- Unit Investment Trusts (UITs)

- 529 College Savings Plans

- Advisory and Trust Services

Although they are not guaranteed, MassMutual has paid out whole life insurance dividends to its eligible participating policy holders every year since 1869. The insurer has a current dividend of 6.0%, which ranks it as #1 in 2022. Overall, MassMutual has a 15-year average dividend payout of over 7%.

As of year-end 2020, the company paid out more than $6 billion in just insurance and annuity benefit payments, along with $1.7 billion in policy holder dividends in 2020.

With $222 billion in total invested assets and roughly $29 billion in total adjusted capital (as of December 31, 2020), MassMutual is considered strong and stable by the insurer ratings agencies. This mutual insurer is also ranked as #123 on the Fortune 500 list. Source.

MassMutual Financial Strength Ratings

| Rating Agency: | Rating |

|---|---|

| A.M. Best Company | A++ (Superior) |

| Fitch Ratings | AA+ (Very Strong) |

| Moody’s Investors Service | Aa3 (High Quality) |

| Standard & Poor’s | AA (Very Strong) |

New York Life Insurance Company

![]()

![]() New York Life Insurance Company began its operations in 1845, and even through some extremely challenging financial and economic times in the U.S., this insurer has remained committed to its policy holders. This company is the largest mutual insurance company in the United States, and is one of the largest life insurance companies in the world.

New York Life Insurance Company began its operations in 1845, and even through some extremely challenging financial and economic times in the U.S., this insurer has remained committed to its policy holders. This company is the largest mutual insurance company in the United States, and is one of the largest life insurance companies in the world.

Products and services that are available through New York Life include the following:

- Life Insurance (term life, whole life, universal life, and variable universal life)

- Long-term care insurance

- Annuities

- Supplemental disability insurance

- Mutual funds

- ETFs (Exchange traded funds)

- 529 college savings plans

- Estate planning

- Wealth management

- Employee benefits and other types of protection for businesses

New York Life Insurance Company and its subsidiaries, New York Life Insurance and Annuity Corporation, Life Insurance Company of North America and New York Life Group Insurance Company of NY have earned the highest financial strength ratings that are currently awarded to any life insurance by the major rating agencies.

NY Life Ratings

The current ratings (as of early 2022) for these companies include:

| Rating Agency | Financial Strength Rating | Date of Latest Action |

|---|---|---|

| A.M. Best | A++ | October 13, 2021 |

| Fitch Ratings | AAA | November 4, 2021 |

| Moody’s Investors Service | Aaa | February 10, 2021 |

| Standard & Poor’s | AA+ | December 18, 2019 |

Source: https://www.newyorklife.com/about/our-strength/what-rating-agencies-say

New York Life has declared an estimated dividend of $1.9 billion for the year. As with other mutual whole life insurance companies, even though dividends are not guaranteed, 2023 will be the 169th consecutive year that the New York Life Board of Directors has declared a dividend. This is in line with the company’s history of rising policy holder benefits throughout the years.

The company has paid in excess of $1 billion in dividends to its whole life insurance clients every year since 1990, and more than $44 billion in total dividend payouts over that time. Even though the recent COVID-19 pandemic, New York Life Insurance Company has maintained a position of incredible strength, which is due in large part to its focus business strategy, as well as the company’s long-term investment perspective, and resolute commitment to mutuality.

Policy Owner Benefits and Dividends (in Billions)

| 2020 | $12.4 |

| 2019 | $11.5 |

| 2018 | $11.1 |

| 2017 | $10.6 |

| 2016 | $10.1 |

Source: https://www.newyorklife.com/report-to-policy-owners/mutuality-dividends#

The Guardian Life Insurance Company of America

![]()

![]() The Guardian Life Insurance Company has been in the business of helping its customers for more than 160 years. Today, this insurer has approximately 29 million clients who have their health, wealth, and life protected by the Guardian. Today, this insurer is a Fortune 250 mutual company.

The Guardian Life Insurance Company has been in the business of helping its customers for more than 160 years. Today, this insurer has approximately 29 million clients who have their health, wealth, and life protected by the Guardian. Today, this insurer is a Fortune 250 mutual company.

Guardian Life offers a wide range of different products and services, such as:

- Life Insurance

- Disability Insurance

- Dental Insurance

- Vision Insurance

- Accident Insurance

- Critical Illness Insurance

- Cancer Insurance

- Hospital Indemnity Coverage

- Annuities

- IRAs (Individual Retirement Accounts)

- Investments / Brokerage Accounts

As a mutual whole life insurance provider, Guardian Life is owned by its policy holders, so the insurer is not accountable to stockholders and other types of outside investors. Rather, it rewards its qualified policy holders by paying out dividends, which it has done consistently throughout its 161-year history.

For 2022, Guardian Life announced that its Board of Directors approved a $1.13 billion dividend allocation to its eligible individual whole life insurance policy holders, which is the largest dividend in the company’s existence. The dividend interest rate will be 5.65% in 2022, and is consistent with the rate in 2021. Source.

The dividend that is being paid out by Guardian Life is driven primarily by its strong long-term investment focus, as well as its sound underwriting, prudent expense management, and earnings from complementary businesses.

In 2023, Guardian Life paid its policyholders a dividend for the 162nd time. The company’s dividend rate came in at 5.75% for a total payment of $1.26 billion.

The company has approximately $722 billion of life insurance in force, including whole life insurance, Given its extremely stable foundation, The Guardian is strong in terms of its financial strength ratings, too, with the following marks from the insurer ratings agencies:

The Guardian Life Insurance Company’s Financial Strength Ratings

| Agency | Rating |

|---|---|

| Moody’s Investors Service | Aa2 (Excellent) |

| A.M. Best Company | A++ (Superior) |

| Standard & Poor’s | AA+ (Very Strong) |

| Fitch | AA+ (Very Strong) |

| COMDEX | 99 out of 100 |

Source: Financial Highlights and Ratings. https://guardianlife.com/financial-highlights

The company’s focus on helping to prepare its customers for the future has been a key driver for the Guardian to deliver outstanding results, as well as to continue providing excellent customer service.

Just some of the accolades that have recently been received by Guardian Life include:

- Recognition by J.D. Power for the 12th consecutive year for providing “An outstanding customer service experience” for phone support.

- Extended capabilities for customers to protect their families with disability insurance for non-working spouses and the introduction of a first of its kind care conversion rider to term life insurance.

Northwestern Mutual

![]()

![]() Northwestern Mutual began operating in the 1850s in the United States, and it paid out its first death benefit claims in 1859, following a train collision in Johnson Creek, Wisconsin, when two of the company’s policy holders were killed in the accident.

Northwestern Mutual began operating in the 1850s in the United States, and it paid out its first death benefit claims in 1859, following a train collision in Johnson Creek, Wisconsin, when two of the company’s policy holders were killed in the accident.

Today, Northwestern Mutual possesses a $260 billion portfolio – a portfolio that has grown consistently throughout the years, and that is a major contributor to the company’s unsurpassed financial strength and policy holder dividends. Source.

This mutual whole life insurance provider is considered to be among the strongest in terms of financial stability, and it has earned the highest financial strength ratings that are awarded to any U.S. life insurers by all of the major ratings agencies, including a(n):

Financial Strength Ratings for Northwestern Mutual

| Agency | Rating |

|---|---|

| A.M. Best | A++ |

| Fitch Ratings | AAA |

| Moody’s Investors Service | Aaa |

| S&P Global Ratings | AA+ |

Source: Our Commitment to Financial Strength https://northwesternmutual.com/financial-information/

Northwestern Mutual has also earned numerous awards and recognition. It is a Fortune 500 Company, and was named one of the “World’s Most Admired Company” in its industry, according to FORTUNE Magazine’s annual survey (published in February 2021). In addition, as #90 on the list of the Fortune 500 companies, Northwestern Mutual is among America’s most premier companies.

The products that are offered through Northwestern Mutual include:

- Life Insurance

- Disability Insurance

- Long-Term Care Insurance

- Income Annuities (Fixed and Variable)

- Investments

- Private Wealth Management

- Advisory Programs

- Private Client Services

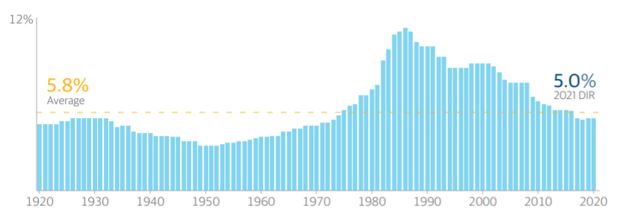

As a mutual whole life insurance provider, Northwestern Mutual focuses on its policy holders. Over the past century, the company has averaged 5.8% on its dividend interest rate, which is declared annually by its Board of Trustees.

Northwestern Mutual’s General Account portfolio is an important contributor to policy holder dividends. This contribution is reflected in the company’s dividend interest rate, or DIR, which is declared annually for whole life insurance policies by the Board of Trustees, and it reflects General Account investment earnings in recent years.

100 Years of Northwestern Mutual’s Dividend Interest Rate

1920 – 2020

Note: For years prior to 1982, the dividend interest rate (DIR) reflects the highest applicable dividend interest rate across all traditional permanent life insurance policies. After 1982, the graph above reflects the dividend interest rate for unborrowed funds for most traditional permanent life insurance policies with direct recognition.

Source: https://www.northwesternmutual.com/assets/pdf/financial-reports/investment-report.pdf

Even though whole life insurance policy dividends are not guaranteed, many of the large mutual insurers have consistently paid them for decades – and some for over a century.

And, while the dividend investment rate (DIR) is just one of the many factors to keep in mind when considering the purchase of life insurance, comparing this rate to the yields of common high-quality, low-risk fixed-income financial vehicles can help to provide a useful perspective.

Comparison of Northwestern Mutual’s Dividend Interest Rate (DIR) with Other Common “Safe” Financial Vehicles

| Northwestern Mutual Dividend Investment Rate (DIR) | 5% |

| Money Market | 0.10% |

| 5-Year Certificate of Deposit (CD) | 0.48% |

| U.S. Municipal Bonds | 1.27% |

| 10-Year Treasury Bond | 1.41% |

| U.S. Corporate Bonds | 1.76% |

Sources: The Wall Street Journal; Bloomberg Barclay’s Municipal Bond Index; Bloomberg; Bloomberg Barclays AA Rated Index as of February 28, 2021.

Northwestern Mutual Annual Investment Report. https://www.northwesternmutual.com/assets/pdf/financial-reports/investment-report.pdf

Even when comparing the historical dividend rates of six of the top whole life, dividend paying mutual insurers over the past 20 years – a time period where many years showed historically low interest rates – the payouts were quite impressive, particularly in comparison to rates on other safe alternatives.

20-Year Historical Dividend Rates

From Top Mutual Whole Life Insurance Companies

| Company | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Ameritas | 5.45 | 5.35 | 5.25 | 5.25 | 5.15 | 5.00 | 5.00 | 5.00 | ? | ? | ? |

| MetLife | 5.50 | 5.25 | 5.25 | 5.10 | 5.00 | 4.7 | 4.7 | 4.7 | ? | ? | ? |

| New York Life | 5.80 | 5.90 | 6.00 | 6.20 | 6.20 | 6.30 | 6.10 | 6.00 | 6.10 | 5.8 | 1.9 |

| Northwestern Mutual | 5.85 | 5.60 | 5.60 | 5.60 | 5.45 | 5.00 | 4.90 | 5.00 | 5.00 | 5.00 | 5.00 |

| Minnesota Life | 6.00 | 4.75 | 5.00 | 5.25 | 5.00 | 5.00 | 5.00 | ? | ? | ? | ? |

| National Life Group | 6.00 | 5.75 | 5.75 | 5.75 | 5.75 | 5.75 | 5.25 | ? | ? | ? | ? |

| Ohio National | 6.15 | 6.00 | 6.00 | 6.00 | 6.00 | 5.75 | 5.40 | 5.40 | 5.2 | 4.7 | ? |

| Foresters | 6.32 | 6.70 | 6.65 | 6.75 | 6.60 | 6.40 | 6.23 | 6.23 | 5.58 | ? | ? |

| Penn Mutual | 6.34 | 6.34 | 6.34 | 6.34 | 6.34 | 6.34 | 6.34 | 6.10 | 6.10 | 5.75 | 5.75 |

| Guardian | 6.95 | 6.65 | 6.25 | 6.05 | 6.05 | 5.85 | 5.85 | 5.85 | 5.65 | 5.65 | 5.65 |

OneAmerica

![]()

![]() The products and services that are offered by OneAmerica include:

The products and services that are offered by OneAmerica include:

- Life Insurance

- Annuities

- Long-Term Care insurance

- Workplace Benefit Plans

- Workplace Retirement Plans

- Securities

- Disability Income Insurance

- Retirement Services

- Group Ancillary Products (such as EAP and Travel Assistance)

OneAmerica has been active in the insurance arena for more than 140 years. During that time, the company has grown and expanded, and it is today considered one of the fastest-growing mutual insurance holding companies in the United States.

In August 2021, A.M. Best affirmed the A+ (Superior) financial strength rating for OneAmerica companies American United Life Insurance Company (AUL), as well as its affiliate company, The State Life Insurance Company. Source.

As a mutual insurance company, OneAmerica has a long history of paying out dividends to its policy holders. Recently, its board of directors approved an estimated dividend allocation of more than $27.3 million to its eligible whole life insurance policy holders in 2022.

Even despite the tough challenges that have been faced since the beginning of the COVID-19 pandemic, which hit the U.S. in early 2020, OneAmerica / AUL, as well as many other mutual insurance companies have continued to take care of and reward their owners / policy holders – and many intend to keep doing so in the future.

How to Customize a Whole Life Insurance Strategy for Your Objectives

Choosing the right whole life insurance policy (and company) can be somewhat overwhelming. There are many different options to consider both in terms of the benefits that you are seeking, as well as the financial strength and claims paying ability of the insurance carrier.

Because committing to the wrong policy could divert your short- and long-term financial outcomes, it is recommended that you first go over your specific situation with a life insurance specialist who can help you with narrowing down the right option for you.

If you would like to set up a time to discuss your particular needs and potential solutions, feel free to contact Insurance and Estates at (877) 787-7558. Or, you can send us an email with any questions via our secure online contact form by going to info@insuranceandestates.com. We look forward to assisting you.