Ready to implement infinite banking? This is the step-by-step framework.

This guide walks you through exactly how to build and operate your own banking system using a properly structured high cash value whole life insurance policy — from choosing the right vehicle to integrating it into your estate plan.

If you’re still evaluating whether IBC is right for you, start with our infinite banking guide or our honest pros and cons.

TL;DR — How to Be Your Own Banker

- The vehicle: High cash value whole life insurance from a mutual company, designed with 60-90% of premium flowing into paid-up additions

- The framework: 7 steps — choose the vehicle, add riders, fund strategically, borrow against cash value, repay with discipline, repeat and compound, integrate into estate planning

- The key mechanic: Your cash value keeps compounding even while you borrow against it — borrow, deploy, repay, repeat from an elevated position

- The timeline: Access to 90%+ of cash value from day one, but plan for 3-5 years of capitalization before significant deployment

- The discipline: You must repay policy loans consistently — this is what separates practitioners from people who just bought a whole life policy

Bottom Line: Infinite banking changes where your money flows. This guide shows you exactly how to build the system, step by step.

Why Trust This Guide

This guide was written and reviewed by the team at Insurance & Estates — ranked the #1 life insurance agency on Trustpilot with 280+ verified reviews. Our team brings 70+ years of combined experience in estate planning, financial services, and infinite banking policy design. Since 2017, we’ve designed and implemented 1,000+ IBC policies as independent brokers (not captive agents), giving us access to every major mutual carrier including Penn Mutual, MassMutual, and Guardian. We practice what we teach — our advisors use infinite banking in their own financial lives.

Table of Contents

- How to Be Your Own Banker in 7 Steps

- Real-World Example: How Infinite Banking Works

- Next Steps to Becoming Your Own Banker

- Frequently Asked Questions

How to Be Your Own Banker in 7 Steps

This 7-step framework for building your own banking system using whole life insurance will show you how to achieve financial independence outside of traditional banks, Wall Street volatility, and the typical financial constraints most Americans face today.

The 7-Step Framework:

- Step 1: Choose the Right Financial Vehicle

- Step 2: Add Riders That Maximize Cash Value Growth

- Step 3: Fund Your Banking System

- Step 4: Borrow From Your Policy

- Step 5: Pay Yourself Back

- Step 6: Repeat and Compound

- Step 7: Build It Into Your Estate Plan

Step 1: What Type of Life Insurance Works Best for Personal Banking?

The most effective vehicle for implementing the infinite banking strategy is high cash value whole life insurance from a mutual insurance company. This specific type of dividend-paying whole life policy differs significantly from traditional whole life insurance in its design approach. While conventional policies emphasize death benefits, a policy structured for personal banking prioritizes early cash value accumulation.

These aren’t obscure financial instruments. Companies like Bank of America, Wells Fargo, and JPMorgan collectively hold billions in cash value life insurance. They use it the same way you will: guaranteed growth, tax advantages, and liquidity on demand.

Paid-Up Additions: The Key to Early Cash Value Growth

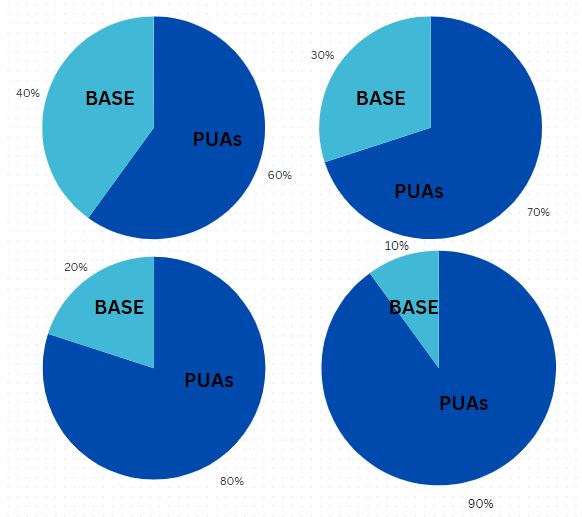

The primary method for achieving rapid cash value growth is designing your policy with a higher proportion of paid-up additions (PUAs) versus base premium. The greater the percentage allocated to paid-up additions, the faster your early cash value grows. Popular whole life policy designs typically feature PUA-to-base premium ratios of 60/40, 70/30, 80/20, and sometimes even 90/10 for maximum early cash value accumulation.

We say “typically” because at Insurance and Estates, we’ve helped clients across 50 states implement this strategy, and each situation requires a tailored approach.

Section 7702: Your Tax Advantage Foundation

One of the most compelling benefits of using dividend-paying whole life insurance for your personal banking system comes from the tax advantages provided under IRC Section 7702.

Under this code section, neither policy interest accrued nor dividends paid are reported as taxable income. Your cash value grows tax-deferred and can be accessed tax-free through policy loans, creating a powerful tax-advantaged financial tool.

As tax strategist Tom Wheelwright of Rich Dad Advisor fame explains, the tax code is a series of incentives. Thanks to IRC 7702, cash value life insurance represents one such financially strategic incentive.

Many carriers offer quality cash value policies, but our experience shows that selecting from the top dividend-paying whole life insurance companies provides the best foundation for an infinite banking strategy.

Balancing Cash Value and Death Benefit for Optimal Banking Performance

The primary objective of an infinite banking policy is maximizing cash value while minimizing the initial death benefit. This strategic approach ensures that more of your premium payments flow directly into your accessible cash value.

This policy design approach actually reduces commissions for us as agents.

And we’re perfectly comfortable with that, as our primary mission is serving our clients’ best interests above our own.

Some clients may desire a substantial death benefit from the beginning. While a “banking policy” isn’t initially designed to provide a large death benefit (though it will grow significantly over your lifetime), you can obtain additional coverage through the strategic life insurance riders we’ll discuss next.

Step 2: Which Life Insurance Riders Maximize Cash Value Growth?

A properly designed high cash value whole life insurance policy may include several of these powerful riders to maximize early cash value growth and policy flexibility:

Paid-Up Additions Rider: The Cash Value Accelerator

Paid-up additions are essentially additional insurance coverage that’s fully paid for upon purchase.

The Paid-Up Additions Rider allows you as the policy owner to purchase additional death benefit while simultaneously increasing your policy’s cash value growth rate.

This rider becomes particularly powerful when you direct your annual dividends from participating life insurance companies toward purchasing more paid-up additions, creating an exponential compound growth effect.

Life Insurance Supplement Rider: Strategic Blending

The Life Insurance Supplement Rider (LISR) strategically blends lower-cost term life insurance with permanent life insurance. The term portion gradually decreases as you make payments, eventually leaving you with only permanent coverage.

Additional Life Insurance Rider: Enhanced Premium Capacity

The Additional Life Insurance Rider (ALIR) enables you to make increased premium payments to purchase additional participating paid-up life insurance, enhancing both your policy’s death benefit protection and cash value accumulation potential.

Term Life Rider: Flexible Protection Enhancement

Not to be confused with the LISR mentioned above, the Term Life Rider (or Renewable Term Rider) provides straightforward term life insurance that can be converted to permanent life insurance in the future if you choose. Adding the term rider to your policy allows you to overfund your policy and remain within IRS guidelines.

This rider is an excellent option for young families implementing infinite banking who need substantial death benefit protection immediately. It offers additional coverage that can be converted to permanent insurance as your financial position strengthens.

Guaranteed Insurability Rider: Future-Proofing Your Coverage

The Guaranteed Insurability Rider (GIR) might not immediately increase your cash value growth, but it provides the valuable guarantee that you can purchase additional insurance in the future without answering health questions or taking medical exams.

This option is particularly valuable when considering life insurance for children, as it guarantees their ability to increase coverage regardless of future health conditions.

Step 3: How Much Should You Fund Your Infinite Banking Policy?

With your policy properly structured, it’s time to fund it strategically. The optimal approach is to overfund your policy to the maximum point possible without triggering modified endowment contract (MEC) status.

The IRS has established guidelines that prevent excessive contributions to life insurance policies to prevent their use as pure tax shelters. While we want to avoid MEC status, we also aim to maximize early cash value accumulation by utilizing the strategic riders mentioned above.

Depending on your situation, you may qualify for backdating your policy to save age, allowing you to contribute more money in the first year than would otherwise be permitted.

The Vital “Capitalization Period”

As time passes, your policy’s cash value will steadily increase. In Nelson Nash’s foundational book, Becoming Your Own Banker©, he recommends dedicating several years to this capitalization phase before major utilization.

The good news? A properly structured insurance policy begins accumulating cash value almost immediately. Depending on your policy design, you should have access to 90% or more of your cash value from day one, providing liquidity while your banking system grows.

How Much Should You Contribute?

There’s no single right answer — it depends on your income, goals, and financial situation. But here are general guidelines based on our experience with hundreds of clients:

- Starting out: Many clients begin with $300–$500/month and scale up over time as income grows

- Moderate funding: $1,000–$2,000/month allows for meaningful cash value accumulation within 3–5 years

- Aggressive capitalization: $25,000+ annually for those who want to deploy capital quickly — this is where the strategy really accelerates

As Nelson Nash taught, the more capital inside the system, the more powerful it becomes. The goal isn’t to save 10% of your income in someone else’s bank. It’s to route as much of your income as possible through a system you own and control.

Step 4: How Do You Borrow From Your Life Insurance Policy?

Having guided clients through real estate acquisitions, business financing, and major purchases using policy loans, the pattern is clear: those who treat their policy like a bank outperform those who treat it like a savings account.

Important: For an authentic banking policy to function optimally, always borrow from the policy rather than withdrawing money.

When you withdraw, you permanently reduce your cash value.

When you borrow from the insurance company using your cash value as collateral, your cash value continues growing inside your policy.

As your policy accumulates substantial cash value, you can leverage that value as collateral through policy loans. The insurance company lends you money secured by your cash value, and you can deploy those funds however you choose.

The key advantage: when you use your cash value as collateral and take out a policy loan, the money in your account continues growing through uninterrupted compound interest.

This means your money works for you in two places simultaneously — continuing to grow within your policy while also being deployed for investments, business, or major purchases.

Strategic Uses for Policy Loans

Acquire Cash-Flowing Assets

Real estate stands out as a premier cash-flowing asset. Real estate investments can generate regular income while offering additional tax advantages. This scenario perfectly showcases the infinite banking concept in action.

At its core, infinite banking involves lending yourself money and systematically recapturing that capital. When you use a policy loan for a real estate down payment, you can then direct the monthly cash flow from that property toward repaying your policy loan with interest.

Pro tip: Don’t shortchange yourself here. Charge yourself the current interest rate that a traditional lender would charge you. Remember, you wear two hats — the banker and the investor.

As you use your property’s cash flow to repay your loan with interest, you simultaneously increase your policy’s death benefit and accelerate cash value growth. This creates even more opportunities for personal financing in the future, making it one of the most powerful real estate wealth-building strategies available.

Finance Your Business Operations

Another strategic application for policy loans is financing your business operations. Take a policy loan, then lend that money to your business. Your business then repays you with interest.

This approach allows you to recapture your own interest payments while replenishing your policy. Plus, your business may be eligible to deduct the interest payments, creating an additional financial advantage.

Self-Finance Major Purchases

Why deplete your savings or finance through traditional banks when purchasing vehicles, funding education, or making other significant investments? Instead, use your banking policy to self-finance these expenses.

This strategy allows you to recapture the interest you would have paid to financial institutions or recover the opportunity cost of paying cash without recouping your capital.

The greatest advantage of personal financing is your position as the banker. You determine the interest rate for repayment and the terms of your loan. However, to maximize the infinite banking strategy’s benefits, consistently repaying your policy loans with interest is essential.

Beyond Policy Loans: Cash Value Lines of Credit (CVLOC)

Standard policy loans aren’t your only option. Some practitioners also use a Cash Value Line of Credit (CVLOC) — an arrangement where a third-party lender provides a line of credit secured by your policy’s cash value. The advantage is potentially lower interest rates than a standard policy loan, plus the convenience of a revolving credit line you can draw from as needed.

CVLOCs work particularly well when you own multiple policies and want consolidated access to your capital without taking individual loans from each carrier. The lender uses your policies as collateral, and because it’s a cash-secured loan, it typically doesn’t appear on your credit report.

Not every situation calls for a CVLOC — standard policy loans work well for most practitioners. But as your banking system grows, it’s worth knowing this tool exists.

Step 5: Why Is Paying Yourself Back the Key to Infinite Banking?

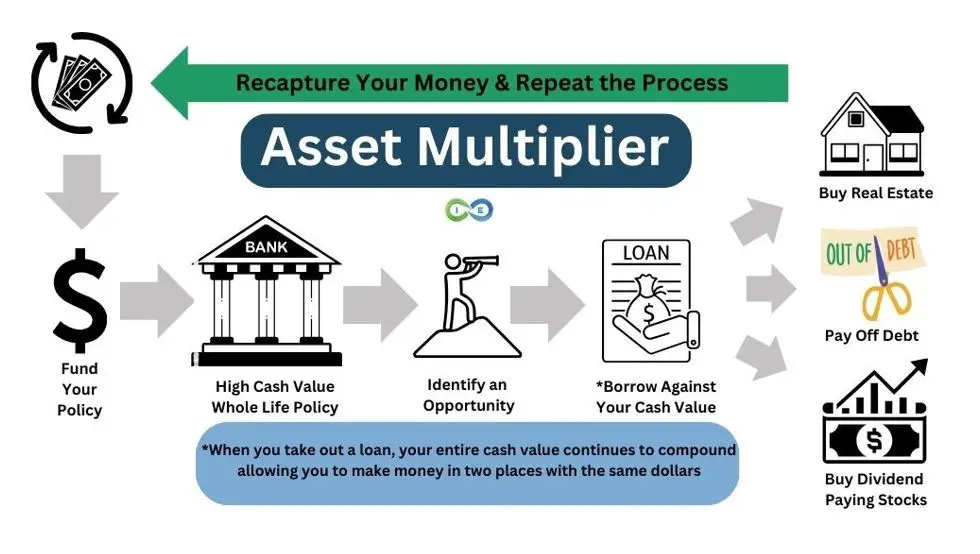

Successfully implementing the infinite banking strategy requires discipline, particularly when it comes to recapturing both principal and interest on your policy loans. We call this process the “Asset Multiplier Blueprint” — the goal is to use your life insurance asset to buy more assets.

In our experience, this step separates successful infinite banking practitioners from those who abandon the strategy. The math only works if you pay yourself back. For those with the discipline to consistently execute this vital step, the growth potential of your banking policy is virtually unlimited.

As Nelson Nash would say, failing to repay yourself is essentially “stealing the peas” — taking goods out the back door of your own store without paying retail price.

Loan repayment forms the cornerstone of this financial strategy because it’s the systematic action that generates exceptional long-term returns throughout your lifetime. As you continue developing your banking policy, you accumulate an increasingly substantial cash reserve that can provide tax-free income through strategic policy loans.

A Note on “Paying Interest to Yourself”

You’ll hear this phrase everywhere in the infinite banking world, and we want to be precise about how it works because honesty matters more than marketing.

When you take a policy loan, the money comes from the insurance company’s general fund — not directly from your cash value. Your cash value is collateral. The interest you pay on the loan goes back into the general fund, not into your policy’s cash value column.

So how does the “pay yourself” idea work? Because you’re a policyholder of a mutual insurance company, you’re a co-owner. The general fund’s profits — including from loan interest — get distributed back to policyholders through dividends. You don’t pay interest “to yourself” in a direct, dollar-for-dollar sense. But the interest stays within a system you own a piece of, rather than enriching a bank where you’re just a customer number.

The more accurate way to think about it: your banking system earns 4–6% on the full balance while you borrow at 5%. The net cost of borrowing is minimal — and your capital never stops compounding. That’s the real advantage, not a marketing slogan.

Step 6: How Does Infinite Banking Create Compounding Wealth?

After repaying your policy loan, don’t let your capital sit idle. Repeat the process: borrow, deploy, repay with interest, then borrow again. Each cycle expands your available capital base.

This is where infinite banking separates from conventional financing.

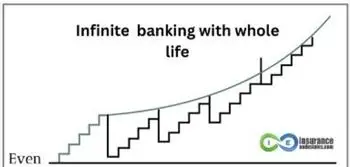

The Stair-Step Effect vs. Starting Over

With a traditional bank loan or HELOC, you deplete your capital to make a purchase. You start at zero (or negative) and spend years climbing back. Once you pay off the loan, you have the asset but no capital. Want to make another move? Start over. Back to zero.

With infinite banking, you never start over. Your cash value keeps growing even while you borrow against it. When you repay the loan with interest, your policy’s value jumps higher than before. The next loan starts from that elevated position, not from zero.

Each loan-and-repayment cycle builds on the last. You never reset to zero.

The chart above shows this stair-step pattern. The curved line represents your policy’s guaranteed growth. The stair-steps represent each borrow-repay cycle pushing your capital base higher. Over time, the gap between where you’d be with conventional financing and where you are with infinite banking becomes massive.

This is why the strategy rewards patience and discipline. Early cycles feel modest. But 10, 15, 20 years in, the compounding becomes undeniable.

Step 7: How Does Infinite Banking Fit Into Estate Planning?

After successfully implementing your infinite banking strategy throughout your lifetime, you’ll have built a substantial estate to transfer to future generations.

Effective estate planning becomes essential for maximizing the legacy you leave to your family.

There are numerous strategies for accomplishing this, both during your lifetime and after your passing. The critical factor is planning proactively so your family can benefit from the full results of your disciplined financial approach.

With a properly structured estate plan, continuously growing cash value, and a guaranteed death benefit passing to your beneficiaries, you’ll be positioned to create a multi-generational financial legacy. What if your parents had taught you these principles? Your financial life might look completely different. By adopting infinite banking, you model self-reliance for your children and grandchildren — breaking free from Wall Street’s volatility and building something that endures.

Policies for young family members lock in low premiums and decades of compounding growth, ensuring generational wealth isn’t just a concept but a reality.

Real-World Example: How Infinite Banking Works

Theory is one thing. Let’s look at how this works with real numbers. Consider John, a real estate investor who used the infinite banking concept to build wealth.

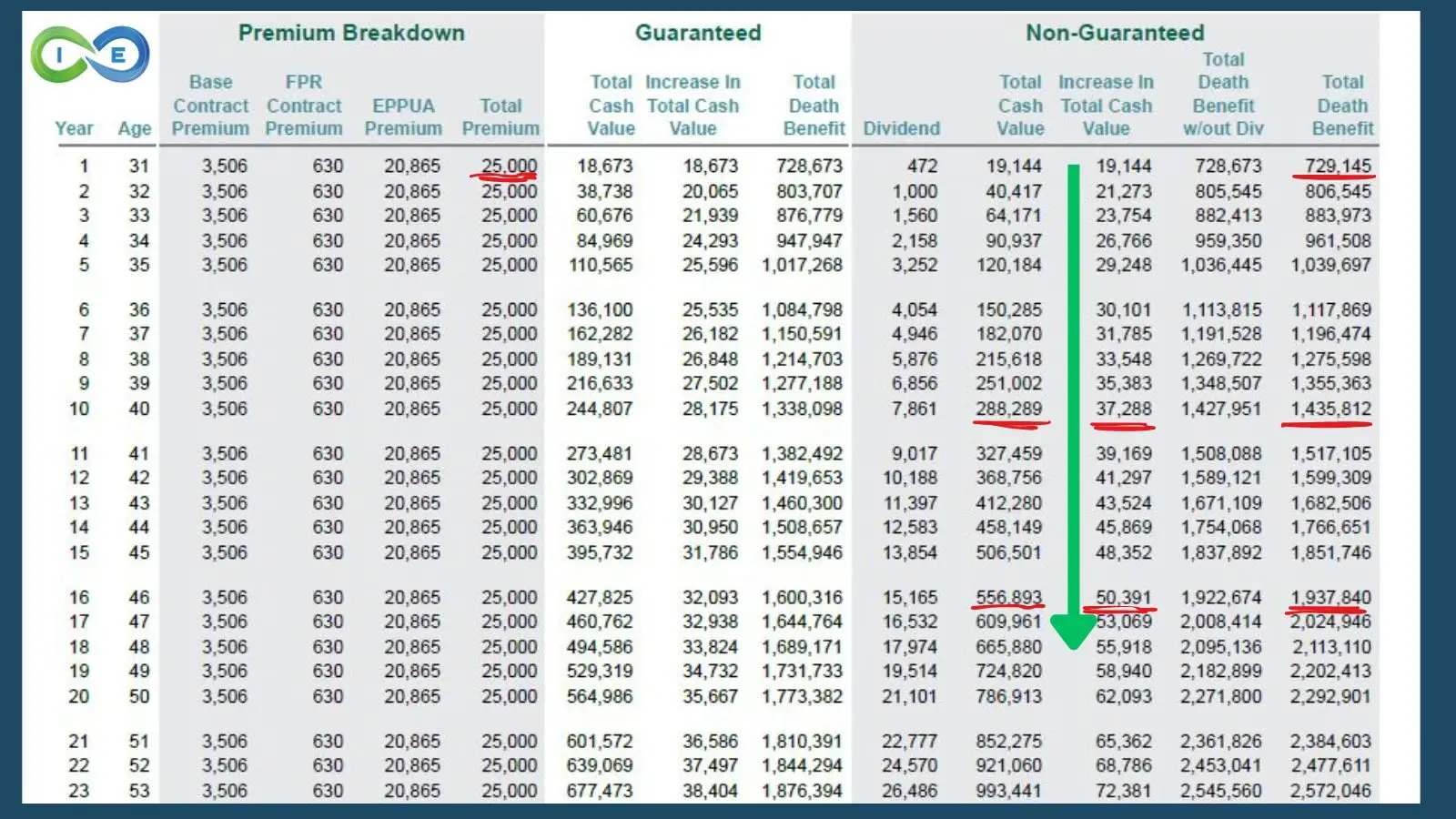

Step 1: John started by funding a high cash value whole life policy with $25,000 per year, structured for maximum cash value growth.

As you can see from this actual policy illustration, each $25,000 annual premium is strategically allocated:

- $3,506 to the base contract premium

- $630 to the Flexible Premium Rider

- $20,865 to the Enhanced Paid-Up Additions Rider

That’s over 83% of the premium going directly toward cash value growth — not insurance costs. This is what a properly designed banking policy looks like in practice.

Step 2: By year 4, John’s cash value had grown to approximately $90,937 (as shown in the “Total Cash Value” column under non-guaranteed values). This rapid cash accumulation happened even though he’d only paid in $100,000 total ($25,000 × 4 years).

Step 3: John borrowed $70,000 against his policy as a down payment on a $300,000 rental property. He could access nearly 80% of his cash value for the investment.

Step 4: While his $70,000 was deployed in real estate, his entire cash value continued earning dividends and interest inside the policy. By year 10, his cash value would grow to $288,289 even with his loan outstanding.

Step 5: John used the $2,000 monthly rental income to:

- Pay the mortgage on the property ($1,200)

- Repay his policy loan with interest ($800)

Result after 5 years:

- John’s policy loan was fully repaid

- His cash value had grown to approximately $150,000 (around year 6–7 in the illustration)

- His rental property had appreciated to $350,000

- His death benefit exceeded $1.4 million by year 10 — substantial protection for his family

- John was now ready to repeat the process with an even larger loan from an elevated capital base

Look at the long-term growth potential: by year 20, John’s policy would have a cash value of nearly $787,000 and a death benefit of $2.3 million — all from $25,000 annual premiums. This is the Asset Multiplier in action: the same dollars working in two places simultaneously while creating multiple streams of wealth.

Note: This example uses actual policy illustration numbers. The non-guaranteed values assume dividends will be paid at the current scale. Dividends are not guaranteed, but most mutual insurance companies we work with have consistently paid dividends every year for over 100 years. Individual results will vary based on policy design, funding level, and investment outcomes.

Beyond the Basics: Volume-Based Banking

If infinite banking makes sense to you but you’re wondering how to maximize it — how to push more capital through the system, accelerate the compounding cycles, and turn your policy into true financial infrastructure — you’re ready for the next level.

Volume-Based Banking builds on everything in this guide and shows you how the volume and velocity of capital flowing through your system matters more than the rate of return. It’s the framework that separates people who own a policy from people who operate a banking system.

Next Steps to Becoming Your Own Banker

If you’re ready to explore how infinite banking could work for your specific situation, here’s how to get started:

Schedule Your Free Infinite Banking Strategy Session

Our team will walk you through a personalized policy illustration based on your age, health, income, and goals. You’ll see exactly how the numbers work for your situation — with zero obligation.

- Custom Illustration: Real numbers from real carriers, designed specifically for banking

- Independent Advice: We represent 40+ carriers — we find the best fit for you, not us

- Lifetime Coaching: Ongoing guidance to optimize your banking system as your situation evolves

- No Obligation: Complimentary session with zero pressure to purchase

Don’t accept theoretical examples. Look at your own numbers.

— Barry Brooksby, Certified Infinite Banking Practitioner

Frequently Asked Questions About Being Your Own Bank

For foundational questions about what infinite banking is and whether it’s right for you, see our infinite banking guide and pros and cons. Below are implementation-specific questions.

How long before I can start borrowing from my policy?

With a properly designed policy, you typically have access to 90% or more of your cash value from day one. However, most practitioners recommend a dedicated capitalization period of 3–5 years before taking significant loans. This allows your cash value base to grow large enough that loans don’t strain the policy.

Do I actually pay interest to myself?

Not directly — and we want to be precise about this because honesty matters more than marketing. When you take a policy loan, the money comes from the insurance company’s general fund, not from your cash value. Your cash value is collateral. The interest you pay goes back to the general fund. However, because mutual insurance companies distribute profits to policyholders through dividends, you do indirectly benefit from the interest paid into the general fund. The more accurate way to think about it: you’re borrowing at 5% from your own system while that system keeps earning 4–6% on the full balance — and the interest you pay stays within a mutual company you co-own as a policyholder, rather than enriching a bank you have no stake in.

What happens if I don’t pay back my policy loan?

Policy loans have no required payment schedule and you can’t default in the traditional sense. However, not repaying defeats the purpose of infinite banking. Unpaid loans accrue interest, reduce your death benefit, and if the loan balance exceeds your cash value, the policy can lapse — which triggers a taxable event. As Nelson Nash said, don’t “steal the peas” from your own store.

Can I use infinite banking for real estate?

Yes — real estate is one of the most common applications. You borrow against your policy’s cash value to fund down payments, renovations, or entire purchases. Your cash value continues growing at dividend rates while you deploy the capital into real estate. When rental income or a sale returns your capital, you repay the policy loan and repeat the cycle. For a detailed walkthrough, see our guide on using life insurance to buy real estate.

Can I use infinite banking for my kids’ college?

Yes, and in many ways it’s more flexible than a 529 plan. If your child decides not to go to college, gets a scholarship, or wants to start a business instead, a 529 hits you with penalties and restrictions. With infinite banking, there are no restrictions on how you use the money — tuition, housing, a gap year, entrepreneurship. No penalties if plans change. Start the policy when your children are young, let cash value build for 15-18 years, then use policy loans for education while the policy keeps compounding.

How much should I fund my policy?

There’s no single right answer — it depends on your income, goals, and financial situation. Many clients begin with $300–$500/month and scale up. Moderate funding of $1,000–$2,000/month allows meaningful cash value accumulation within 3–5 years. Aggressive capitalization of $25,000+ annually is where the strategy really accelerates. The key: fund as aggressively as your cash flow allows without crossing the MEC line.

What’s the difference between a regular whole life policy and one designed for banking?

Traditional whole life insurance maximizes the death benefit, which means more of your premium goes toward insurance costs. A policy designed for banking does the opposite: it minimizes the initial death benefit and maximizes early cash value through paid-up additions. In a properly designed banking policy, 60–90% of your premium flows into cash value from year one. This means you have access to more of your money sooner, which is the whole point if you’re using it as a bank.

What are the biggest mistakes people make with infinite banking?

Based on our experience with 1,000+ implementations, the most common mistakes are: working with a traditional insurance agent who doesn’t understand IBC policy design (this is the #1 cause of disappointment), quitting before year 7 when the policy hits its stride, borrowing without a repayment plan, and comparing policy returns to stock market returns instead of comparing to bank savings rates. The vast majority of “failures” trace back to poor policy design — not problems with the concept itself. Working with a specialist who understands proper policy structuring eliminates most of these risks.

Which companies are best for infinite banking?

Not all insurance companies are suited for infinite banking. You need a mutual company (owned by policyholders, not shareholders) with a long dividend payment history, flexible paid-up additions options, and independent broker access. Our team analyzes 47+ whole life carriers and maintains annual rankings based on actual long-term cash value performance — not just dividend rates. For our current analysis, see our guide to the best infinite banking companies.

25 comments

Camille BeBroker

Great insights on how we can use whole life insurance for financial independence! I’ve always been curious about real estate as a route to financial freedom, but your article opened my eyes to the potential of being your own banker. The way you connected Nash, Ramsey, and Kiyosaki’s philosophies was enlightening.

I was particularly intrigued by the idea of having more control over financial assets and leveraging them for greater benefit. How sustainable is this approach in the long-term?

Thanks for breaking down a complex topic into digestible content. Would love to hear more about the practical first steps for beginners looking to dive into this concept. Looking forward to more of your writing!

lee

if i wanted to build my own house and was planning to pay cash for it, how can i lend the money to myself and then pay myself back and write off the interest, without having to claim the interest payments as income also????

Insurance&Estates

No, you cannot write off interest payments you make on a whole life insurance policy loan that’s used to build your personal residence. The IRS doesn’t allow deductions for interest paid on policy loans except in very specific business scenarios. If you own a construction business and use the policy loan funds for business purposes rather than personal use, you may have a potential path to deducting the interest. You would want to consult a tax expert before doing anything.

Jarrell

How much does it take to start being your own bank?

Insurance&Estates

Hi Jarrell,

There are various ways to go about setting up a policy. You can design the infinite banking policy so that the base premium is something you believe you can reasonably pay in good seasons and in bad, when money is flowing or when things are tight. You can then have the paid up addition portion of the policy be 3-4 times as high, so that if you choose to fund the policy with more money you can. This policy design provides a lot of flexibility.

I recommend that if you’re interested in Infinite Banking, connect with either Denise@insuranceandestates.com or Barry@insuranceandestates.com by emailing or scheduling on their respective calendar there.

To your success!

Steve Gibbs for I&E

Steven Gibbs is a licensed insurance agent, and the following agent

license numbers of Steven Gibbs are provided as required by state law:

Resident License; AZ agent #17508301,

Non-resident Licenses: TX agent #2273189, CA agent #0K10610,

LA agent #769583, MA agent #2049963, MN agent #40563357,

UT agent #655544.

Matthew Curotto l

I have so many questions. Who can I talk to, to get answers and understanding?

Steven Gibbs

Hello Matthew, thanks for connecting. We have numerous webinars and videos on our website and 100’s of articles on our blog covering virtually every aspect of this strategy.

When you’re ready, you can also reach out to Denise Boisvert to schedule a call by emailing her at denise@insuranceandestates.com.

Best, Steve Gibbs for I&E

Steven Gibbs is a licensed insurance agent, and the following agent

license numbers of Steven Gibbs are provided as required by state law:

Resident License; AZ agent #17508301,

Non-resident Licenses: TX agent #2273189, CA agent #0K10610,

LA agent #769583, MA agent #2049963, MN agent #40563357,

UT agent #655544.

lawrence jeffords

interested in be your own banker policy

SJG

Hello Lawrence and thanks for inquiring. A great next step is to email Denise Boisvert at denise@insuranceandestates.com to request a call.

Best, Steve Gibbs for I&E

Steven Gibbs is a licensed insurance agent, and the following agent

license numbers of Steven Gibbs are provided as required by state law:

Resident License; AZ agent #17508301,

Non-resident Licenses: TX agent #2273189, CA agent #0K10610,

LA agent #769583, MA agent #2049963, MN agent #40563357,

UT agent #655544.

Jared

I feel like there’s a catch.. surely I don’t just buy a policy and have access to all that money to do with as I please.. right?

SJG

Hey Jared, there isn’t really a catch except that a best practice for any cash value policy is arguably to “let it bake”. Loans are typically available early on at about 90% of cash value in most cases. However, policy loans do have interest rates to consider, notwithstanding these rates (5-7% currently) are somewhat nominal when compared to other bank rates. Point being, this is an asset with easy leverage capability. There isn’t anything mysterious about cash value life insurance (see IRS Code 7702); however, “do as I please with it” isn’t accurate either. Become a student of this asset. We get call from folks in other countries asking for it and it isn’t available there.

Best, Steve Gibbs for I&E

Steven Gibbs is a licensed insurance agent, and the following agent

license numbers of Steven Gibbs are provided as required by state law:

Resident License; AZ agent #17508301,

Non-resident Licenses: TX agent #2273189, CA agent #0K10610,

LA agent #769583, MA agent #2049963, MN agent #40563357,

UT agent #655544.

Mariyah Rojas

I’m 22 years old and I want to become my own bank. I feel as thought a step by step guide would be more helpful than the step by step process provide. Although There was just a update I hope 2023 update would have better detailed information. So that more motivated young people like myself, can have the online resources that we need to achieve our goals.

SJG

Hello and thanks for your comment and insight. We’ve done some education on the 7702 updates so that would be the biggest take away for 2022-2023. Also, we are always seeking to bring things current in terms of our high cash value pages and articles.

Best, Steve Gibbs for I&E

Steven Gibbs is a licensed insurance agent, and the following agent

license numbers of Steven Gibbs are provided as required by state law:

Resident License; AZ agent #17508301,

Non-resident Licenses: TX agent #2273189, CA agent #0K10610,

LA agent #769583, MA agent #2049963, MN agent #40563357,

UT agent #655544.

Osagie Agboh

I will like to explore the option of BYOB through whole like Ins.

I think it is a great idea!

SJG

Hi Osagie, thanks for connecting! It looks like one of our IBC experts connected with you.

To your success!

I&E Pro Team

Eugene

Hi

How to incorporate this into a family trust thing,or it’s just a one man thing?

Insurance&Estates

Hello, this strategy can be utilized with and compliments a family trust in a number of ways. For starters, the life insurance death benefit could be directed to the trust for dynasty planning purposes and death benefit proceeds are far more flexible and offer tax advantages vs. other kinds of accounts. A great next step would be to schedule a discussion by connecting with Barry Brooksby at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Lawrence

Hi, I want to get my daughter started with this. She is 19 years old and my other son is 14, will they be to qualify? thanks

Insurance&Estates

Hello Lawrence, a great first step is to request a call from Barry Brooksby by emailing him at barry@insuranceandestates.com.

Best, Steve

Nik Catalina

How does this work for people at or above a certain age? Are there companies that will issue whole life policies to aged individuals … or is there a cut-off age ? I imagine the premiums would be high ? Please adivise Thanks

Insurance&Estates

Hello Nik, this can work at older ages depending upon health and other factors. Your best first step is to connect with Barry Brooksby by emailing him to request a call at barry@insuranceandestates.com.

Best, Steve

carla domino

Do you have your lecture on video ,I’m hearing impaired and will need close capture.

Insurance&Estates

Hello Carla and thank you for inquiring. At this point I do not have a close caption version of the lecture and apologize for this. I will work on getting this one updated for you. In the meantime, if you haven’t already I invite you to check out our blog page and search “be your own bank” at the top of the page to get an article on this topic also.

Best, Steve Gibbs for I&E

Vincent F Malfa

Do you have software for being own banker

Insurance&Estates

Hello Vincent, thanks for reading and commenting. Yes we like Truth Concepts software for IBC design and financial comparisons, etc. You can google search them directly.

Best,

Steve Gibbs for I&E