Jason Herring: 16 years designing IUL, GUL, and whole life policies | Series 6, 63, 65 Licensed

Steve Gibbs: Co-Founder, Insurance & Estates | 18+ years estate planning law | Advanced Estate Planning certification

Guaranteed Universal Life Insurance: What It Is, How It Works, and Whether It Fits

GUL is the most misunderstood product in the universal life family — not because it’s complicated, but because it’s simple. And in an industry that profits from complexity, simplicity gets overlooked.

Guaranteed Universal Life insurance does one thing exceptionally well: it provides a permanent death benefit at a price point closer to term life than any other permanent product on the market. No cash value to manage. No market exposure to monitor. No index allocations to rebalance. Pay the premium, keep the guarantee.

That simplicity is either exactly what you need or completely wrong for your situation. This guide will help you figure out which.

💡 The Short Answer

- GUL is right if: You need a permanent death benefit for estate planning, final expense, or wealth transfer — and you don’t need cash value growth or banking functionality

- GUL is wrong if: You want to accumulate cash value, access tax-free retirement income, or use your policy as a banking tool — those goals require IUL or whole life

- The honest bottom line: GUL is the most affordable permanent life insurance available. But “permanent death benefit at the lowest cost” is a specific goal — not everyone’s goal. If you’re unsure whether you need cash value or just a death benefit, that’s the first conversation to have with a specialist

Why Trust This Guide

Insurance & Estates designs and places GUL, IUL, VUL, and whole life policies across every major carrier. We’re not captive to any single company, and we don’t default to one product type. When a client needs affordable permanent protection without cash value complexity, we design GUL. When they need accumulation or banking infrastructure, we steer them elsewhere. This guide reflects that same approach — honest assessment of what GUL does well and where other products serve you better.

📑 What’s In This Guide

- → What Is Guaranteed Universal Life Insurance?

- → How a GUL Policy Works

- → Pros and Cons of GUL

- → GUL vs. Other Life Insurance Types

- → Cost Considerations and Sample Rates

- → Who Should Consider GUL (And Who Shouldn’t)

- → GUL Riders Worth Considering

- → Best GUL Companies

- → Choosing the Right GUL Policy

- → Application and Underwriting Process

- → Frequently Asked Questions

- → Next Steps

What Is Guaranteed Universal Life Insurance?

Guaranteed Universal Life (GUL) insurance is a type of permanent life insurance that provides a guaranteed death benefit with fixed premiums and minimal or no cash value accumulation. Think of it as the intersection of term life’s affordability and whole life’s permanence — you get lifelong coverage at a price point significantly lower than whole life, because you’re not paying for cash value growth.

The “guaranteed” in GUL refers to two things: your premiums are fixed for the life of the policy, and the death benefit is guaranteed as long as those premiums are paid on time. This is the no-lapse guarantee — and it’s the feature that defines GUL.

GUL currently accounts for roughly 1% of U.S. individual life insurance sales, but it’s projected to grow at the highest rate among universal life products through 2033. That growth is driven by exactly what makes GUL appealing: affordability, simplicity, and the growing demand for permanent coverage without investment complexity.

How a GUL Policy Works

A GUL policy lets you choose a coverage duration — typically to age 90, 95, 100, or 121 — with premiums that remain fixed for that entire period. The longer the guarantee period, the higher the premium, but the certainty of knowing your cost will never change provides real budget planning value.

The No-Lapse Guarantee

This is GUL’s defining feature. As long as you pay your premiums on time, the policy stays in force regardless of what happens to the minimal cash value inside it. With standard universal life, if your cash value drops too low to cover insurance charges, the policy can lapse. GUL’s no-lapse guarantee removes that risk entirely.

The catch: the guarantee is only as strong as your payment consistency. Miss a premium, let a loan accumulate unpaid interest, or underfund the policy, and the no-lapse guarantee can void. Once voided, the minimal cash value likely can’t sustain the policy on its own. This is why we recommend autopay for every GUL client.

Return of Premium Option

Some GUL policies offer a return of premium rider, allowing you to recover some or all paid premiums if you cancel within a specific period. This adds a layer of flexibility — if your circumstances change and you no longer need the death benefit, you’re not walking away empty-handed. Not every carrier offers this rider, and it does increase the premium, but for clients who want an exit strategy built in, it’s worth evaluating.

✅ Key Takeaway — How GUL Works

GUL is permanent coverage on autopilot. Fixed premiums, guaranteed death benefit, no-lapse guarantee, minimal cash value. The simplicity is the point — but that simplicity means GUL is the wrong tool if you need cash value growth, tax-free retirement income, or banking functionality.

Pros and Cons of Guaranteed Universal Life

Pros

Affordability. GUL premiums are significantly lower than whole life or IUL for the same death benefit amount. You’re paying for the death benefit guarantee only — not for cash value accumulation, dividends, or market-linked crediting.

Guaranteed premiums. Your premium is locked in at issue. It won’t increase as you age, if your health changes, or if interest rates shift. For budget planning over decades, this certainty has real value.

Simplicity. No index allocations to choose. No subaccounts to manage. No annual reviews required. No risk of underfunding due to poor market performance. Pay the premium, keep the guarantee. Period.

Customizable coverage duration. Choose guarantee periods to age 90, 95, 100, or 121 based on your planning needs. A shorter guarantee period means lower premiums, which creates options for budget-conscious buyers who still want coverage well beyond typical term lengths.

Cons

Minimal or no cash value. GUL builds little to no accessible cash value. You can’t borrow against it for opportunities, and there’s no meaningful surrender value if you cancel. If you need your policy to do double duty — protection and accumulation — GUL isn’t the tool.

Limited flexibility. Unlike standard universal life or IUL, GUL offers minimal premium flexibility. The trade-off for guaranteed premiums is that you’re locked into a fixed payment. If cash flow becomes tight, you can’t reduce premiums the way you can with IUL (though with IUL, doing so often causes problems of its own).

No growth potential. GUL doesn’t participate in any market upside. For clients whose goal includes tax-free retirement income or long-term wealth accumulation, IUL or properly designed whole life will outperform GUL by every measure except premium cost.

| Advantages of Guaranteed Universal Life Insurance | Disadvantages of Guaranteed Universal Life Insurance |

|---|---|

| Affordability | Limited flexibility |

| Guaranteed premiums | Low or no cash value accumulation |

| Long term coverage (without the complexity of cash value growth) |

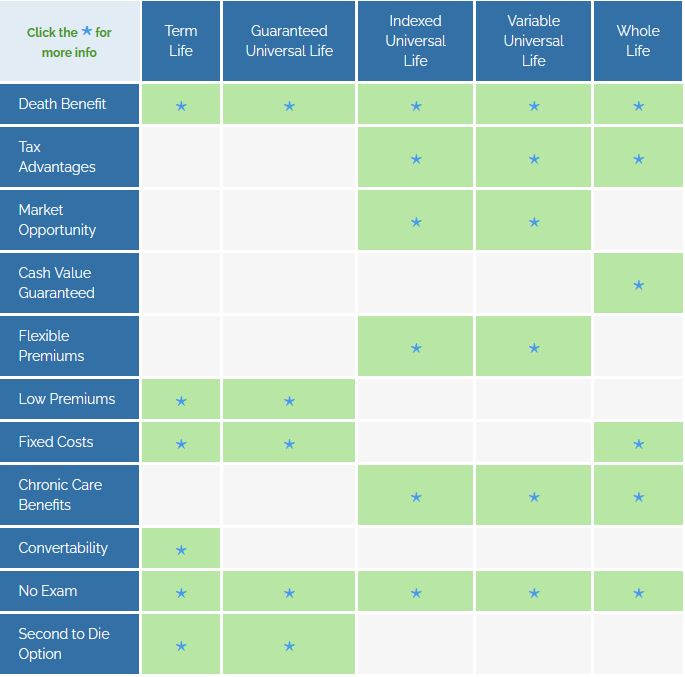

GUL vs. Other Life Insurance Types

GUL occupies a specific niche. Understanding how it compares to other products helps you determine whether it’s the right fit — or whether another product serves your goals better.

GUL vs. Term Life Insurance

Term life insurance is the most affordable death benefit protection available — but it expires. A 20-year term policy covers you for 20 years and then it’s gone. Premiums increase dramatically at renewal, and conversion options have time limits. GUL costs more than term but provides permanent coverage that won’t expire, lapse, or need renewal. If you need coverage beyond age 65-70 (estate planning, final expense, wealth transfer), GUL is often more cost-effective than repeatedly renewing term coverage.

GUL vs. Whole Life Insurance

Whole life insurance provides permanent coverage with guaranteed cash value growth and dividends from mutual companies. Premiums are higher than GUL because you’re paying for that cash value accumulation. If your only goal is a permanent death benefit, GUL gets you there for less money. If you want to use your policy as a financial tool — Volume-Based Banking, infinite banking, or accessing cash value for opportunities — whole life is the only appropriate chassis.

GUL vs. Indexed Universal Life (IUL)

IUL ties cash value growth to a market index with a 0% floor and a cap, designed for tax-free accumulation and retirement income. IUL requires higher premiums, a 15+ year time horizon, consistent funding, and annual monitoring. GUL avoids all of that complexity. If you need cash value growth and tax-free income, IUL is the better product. If you need a permanent death benefit without the overhead, GUL is cleaner and cheaper.

GUL vs. Variable Universal Life (VUL)

VUL invests your cash value directly in market subaccounts — full market gains, full market losses, no floor. VUL is for sophisticated investors who want direct portfolio control inside an insurance wrapper. GUL is the opposite: zero market exposure, zero investment decisions. For most clients comparing GUL and VUL, the goals are so different that if VUL is on your radar, GUL probably isn’t the right product for you (and vice versa).

✅ Key Takeaway — Comparisons

GUL beats term on permanence, beats whole life on price, and beats IUL/VUL on simplicity. But it loses to whole life on cash value growth, loses to IUL on accumulation potential, and loses to VUL on investment upside. Choose GUL when the death benefit is the goal — not the cash value.

Cost Considerations and Sample Rates

GUL premiums are determined by age, gender, health classification, death benefit amount, guarantee period, smoking status, occupation, lifestyle factors, family health history, and the insurance company. The biggest variable is the guarantee period — coverage to age 90 costs significantly less than coverage to age 121.

Sample GUL Premium Rates

The following sample rates are for a GUL policy to age 121 for a male at a preferred plus rate class from A-rated companies and higher. Rates are for informational purposes only and must be qualified.

| Age | $100,000 | $250,000 | $500,000 | $1,000,000 |

|---|---|---|---|---|

| 40 | $879.23 | $1806.41 | $3612.69 | $6545.24 |

| 45 | $1072.89 | $2215.27 | $4430.26 | $7969.30 |

| 50 | $1334.15 | $2764.30 | $5528.46 | $10,183.30 |

| 55 | $1580.46 | $3635.82 | $7271.56 | $13,519.72 |

| 60 | $2017.20 | $4634.69 | $9269.24 | $17,365.04 |

| 65 | $2652.86 | $6420.10 | $12,840.14 | $23,802.49 |

For personalized GUL quotes based on your age, health, and coverage needs, schedule a consultation with one of our Pro Client Guides.

Who Should Consider GUL (And Who Shouldn’t)

GUL fits when:

You need a permanent death benefit for estate planning. Estate planning attorneys — including our co-founder Steve Gibbs — regularly recommend GUL when the planning goal is wealth transfer, estate tax liquidity, or equalizing inheritances among heirs. The death benefit is guaranteed, the cost is predictable, and there’s no investment component to complicate the trust structure.

You want permanent coverage but can’t justify whole life premiums. If your budget doesn’t support whole life’s higher premiums and you don’t need cash value growth, GUL gives you permanent protection at a fraction of the cost.

You’re beyond the ideal window for cash value strategies. If you’re 65+ and need permanent coverage, the time horizon for meaningful cash value accumulation in IUL or whole life is compressed. GUL’s value isn’t in what it accumulates — it’s in the guarantee it provides, regardless of how long you live.

You want simplicity. No annual reviews, no index allocations, no investment decisions, no monitoring. Pay the premium. Keep the guarantee. Done.

GUL doesn’t fit when:

You want to use your policy as a financial tool. Banking strategies, policy loans, cash value access for opportunities — these require whole life’s guaranteed cash values or IUL’s accumulation potential. GUL doesn’t build meaningful cash value, so there’s nothing to borrow against.

You want tax-free retirement income. Life insurance retirement plans (LIRPs) use cash value accumulation and policy loans to create tax-free income in retirement. GUL can’t serve this purpose — IUL or whole life can.

You’re a high earner looking for tax-advantaged accumulation. If you’ve maxed your 401(k) and Roth IRA and want another tax-free growth vehicle, IUL or overfunded whole life is the tool. GUL solves a different problem entirely.

⚠️ Key Takeaway — Right Tool, Right Job

GUL is the most efficient way to buy a permanent death benefit. But if an agent is recommending GUL when you’ve expressed interest in cash value growth, retirement income, or banking strategies, they’re either not listening or they don’t have access to the products that actually serve those goals. The right recommendation starts with your goal — not the product.

Not Sure Whether GUL, IUL, or Whole Life Fits Your Goals?

Our Pro Client Guides will build custom illustrations across product types — GUL, IUL, and whole life — so you can see exactly where the math favors each one for your specific situation.

No pressure, no obligation — just your numbers and an honest assessment of which tool fits.

GUL Riders Worth Considering

GUL’s simplicity extends to its rider options — fewer choices than IUL or whole life, but the ones available can add meaningful protection:

Long-Term Care Rider: Allows you to accelerate a portion of the death benefit to cover long-term care expenses. This is increasingly valuable as long-term care insurance premiums continue to rise. See our full long-term care rider vs. chronic illness rider comparison.

Chronic Illness Rider: Provides early access to the death benefit if you’re diagnosed with a permanent chronic illness. Unlike LTC riders, chronic illness riders typically don’t require you to be in a care facility.

Critical Illness Rider: Allows you to draw from the death benefit for qualifying conditions like heart attack, stroke, or cancer.

Terminal Illness Rider: Provides accelerated access to a portion of the death benefit upon terminal diagnosis. Most carriers include this at no additional cost.

Return of Premium Rider: Recovers some or all paid premiums if you cancel the policy within a specified period. Adds cost but provides an exit strategy.

Accidental Death Benefit Rider: Provides an additional payout if death results from an accident.

Waiver of Monthly Deductions Rider: Covers policy charges if you become disabled (typically after a 6-month waiting period).

Best GUL Companies

We evaluate GUL carriers differently than IUL or VUL — because the product is different. Cash value growth is irrelevant. What matters is the strength of the no-lapse guarantee, premium competitiveness across age ranges, coverage flexibility, and rider options.

Our top GUL carriers include Pacific Life (most customizable, broadest rider options), Protective Life (consistently lowest premiums, simplest coverage), and Penn Mutual (strong return of premium option, full product lineup for future diversification). Lincoln National, Mutual of Omaha, and Foresters Financial also excel in specific niches.

For our complete GUL carrier analysis with detailed comparisons, see our Best Universal Life Insurance Companies guide — GUL section →

Choosing the Right GUL Policy

Not all GUL policies are identical. Here’s what to evaluate when comparing options:

No-lapse guarantee period. This is the single most important feature. Guarantee to age 121 if your goal is lifetime coverage. Shorter guarantee periods (age 90, 95, 100) are cheaper but create risk if you outlive the guarantee.

Premium competitiveness at your age. Carriers price GUL differently across age bands. A company that’s cheapest for a 45-year-old may not be cheapest for a 65-year-old. Compare multiple carriers at your actual issue age.

Return of premium availability. Not all carriers offer this rider. If having an exit strategy matters to you, confirm the rider is available and understand its cost and terms.

Rider compatibility. If you want chronic illness or LTC acceleration riders, verify they’re available with your chosen GUL product and understand how they interact with the death benefit.

Carrier financial strength. You’re entering a relationship that could last 40-50 years. A.M. Best ratings of A (Excellent) or better indicate the carrier can maintain its guarantees through economic downturns.

Application and Underwriting Process

Applying for a GUL policy follows the standard life insurance underwriting process. You’ll provide personal and health information, and a medical exam may be required to assess risk factors.

For applicants with health concerns, simplified underwriting and no-exam options are available from several carriers, though premiums will be higher. Foresters Financial, in particular, offers no-exam GUL for ages 16-55.

An independent advisor can guide you through the underwriting process and shop multiple carriers simultaneously to find the best rate for your health classification — something captive agents at a single company can’t do.

Beyond the Basics: When the Death Benefit Is Just the Starting Point

GUL solves one problem exceptionally well — affordable permanent protection. But if you’re sensing that life insurance can do more than just pay a death benefit, you’re right. For those building a system where your capital works on multiple fronts simultaneously, explore how Volume-Based Banking turns whole life into the foundation of a private banking strategy — and how GUL can complement that foundation as the most cost-efficient way to add additional death benefit coverage.

Frequently Asked Questions

What is guaranteed universal life insurance?

How much does guaranteed universal life insurance cost?

Is guaranteed universal life insurance worth it?

What is a no-lapse guarantee?

What happens if I stop paying GUL premiums?

Is GUL better than term life insurance?

Is GUL better than whole life insurance?

Which companies offer the best GUL policies?

Next Steps

See What GUL Looks Like With Your Numbers

The only way to know whether GUL is the right fit is to see a custom quote built around your age, health, and coverage goals — and to compare it side by side with IUL and whole life so you can see exactly what each product delivers for your premium dollar.

- Custom GUL Quotes: Compare premiums from multiple A-rated carriers at your actual age and health class

- Side-by-Side Comparison: GUL vs. whole life vs. IUL — see what each product delivers for your dollar

- Honest Assessment: Whether GUL, another product, or a combination fits your goals

- No Obligation: Complimentary session with zero pressure to purchase

One quote with your own numbers is worth more than a hundred comparison articles.