TL;DR: Best Convertible Term Life Insurance Companies (2026)

- Penn Mutual — Best overall for wealth builders (converts to dividend-paying whole life)

- MassMutual — Best permanent product access for infinite banking strategies

- Guardian Life — Best for complex health and business situations

- Pacific Life — Best conversion credits and cash benefits

- Protective Life — Best value with high coverage limits

Bottom Line: Most “best convertible term” lists rank companies by price and term length. But conversion only matters if you’re converting into something worth owning. The companies above let you convert to dividend-paying whole life insurance from mutual carriers — not just universal life products with no guarantees.

Why Trust This Guide

With 18+ years in financial services, access to dozens of carriers, and hundreds of conversion cases processed, we evaluate convertible term life insurance differently than comparison sites. We don’t rank by price alone — we rank by what you’re actually converting into, because a cheap term policy that only converts to a mediocre universal life product isn’t a strategy. It’s a dead end. Every recommendation is independently researched and fact-checked by licensed professionals.

Table of Contents

- What Makes a Convertible Term Policy Worth Buying

- Top 5 Best Convertible Term Life Insurance Companies (2026)

- Conversion Feature Comparison Table

- Real Conversion Results: What Actually Happens When You Convert

- Conversion Mistakes That Cost People Coverage

- How to Choose the Right Convertible Term Company

- Honorable Mentions

- Frequently Asked Questions

What Makes a Convertible Term Policy Worth Buying

When most financial platforms recommend term life insurance, they focus on finding the cheapest policy — the “buy term and invest the difference” advice popularized by Dave Ramsey and Suze Orman. But here’s what those rankings miss: conversion is only as valuable as the product you’re converting into.

Most convertible term policies convert to universal life insurance — a product with no guaranteed cash value growth, adjustable premiums that can increase, and a structure that doesn’t support advanced wealth-building strategies. That’s fine for basic permanent coverage, but it’s not a wealth-building tool.

The companies that matter for sophisticated investors are the ones that let you convert to dividend-paying whole life insurance from mutual carriers — policies with guaranteed cash value growth, annual dividends, and the structure needed for strategies like infinite banking.

The Question Nobody Else Is Asking

Before comparing premiums, ask this: What permanent product can I actually convert to?

A convertible term policy from a stock company that only offers universal life conversion is fundamentally different from a convertible term policy from a mutual company that converts to participating whole life. Same feature name. Completely different financial outcomes.

That distinction is the foundation of every ranking on this page.

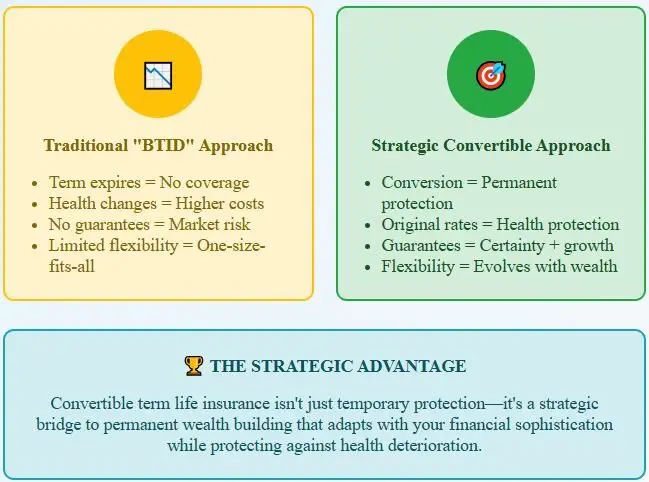

The Original Rate Class Advantage

Convertible term life insurance allows you to convert to permanent coverage at your original health classification regardless of health changes during the term period. If you’re approved as “Super Preferred” at age 35 but develop diabetes or high blood pressure by age 50, you convert at your original rates — not your current health status. This health arbitrage can save tens of thousands in permanent life insurance premiums and may be the difference between getting coverage or being declined entirely.

| Feature | Traditional “BTID” Approach | Strategic Convertible Approach |

|---|---|---|

| When Term Expires | No coverage | Conversion to permanent protection |

| Health Changes | Higher costs or denial | Original rates preserved |

| Guarantees | Market risk on investments | Certainty + guaranteed growth |

| Flexibility | One-size-fits-all | Evolves with wealth |

Top 5 Best Convertible Term Life Insurance Companies (2026)

Our rankings prioritize what matters for long-term wealth building: the quality of permanent products available for conversion, financial strength of mutual carriers, conversion credits, and flexibility. Unlike rankings focused purely on price, we evaluate companies based on what happens after you convert.

Our Evaluation Criteria

- Permanent Product Quality: What can you actually convert to — whole life, UL, or both?

- Mutual vs. Stock Company: Mutual companies align with policyholder interests and pay dividends

- Conversion Age Limits: How long conversion options remain available

- Conversion Credits/Benefits: Financial incentives that reduce permanent policy costs

- Financial Strength: AM Best, S&P, Moody’s, and Fitch ratings for long-term stability

- No-Exam Conversion Limits: Amount convertible without new medical underwriting

1. Penn Mutual — Best Overall for Wealth Builders

![]()

Financial Strength Ratings

- AM Best: A+ (Superior)

- S&P: A+

- Moody’s: Aa3

- Company Type: Mutual

Product: Guaranteed Convertible Term — 10, 15, 20, and 30-year terms starting at $250,000.

Why #1: Penn Mutual is the only company on this list that combines a competitively priced convertible term product with conversion access to industry-leading dividend-paying whole life insurance. As a mutual company, Penn Mutual’s policyholders own the company and share in its profits. They announced a record-breaking $265 million dividend payout in 2026 — the highest in the company’s 175+ year history — with a dividend rate exceeding 6%.

Key Conversion Advantages

- Converts to Whole Life: Access to Penn Mutual’s participating whole life products with guaranteed cash value and dividends

- Annual Premium Credit: Conversion credit equals full year’s term premium

- ACE Underwriting: No-exam coverage up to $5M for ages 20-65

- Automatic Disability Conversion: Unique rider converts to permanent coverage automatically if disabled

- Mutual Company Structure: Policyholder-owned, dividends shared with policyholders

Best For: Investors planning definite conversion to dividend-paying whole life for infinite banking or long-term wealth accumulation. The combination of conversion credits, whole life product quality, and mutual company dividends makes Penn Mutual the clear leader for strategic conversion.

Detailed review available: Penn Mutual insurance analysis.

2. MassMutual — Best Integration with Premium Permanent Products

![]()

Financial Strength Ratings

- AM Best: A++ (Superior)

- S&P: AA+

- Moody’s: Aa3

- Company Type: Mutual

Product: Vantage Term and Direct Term with conversion access to MassMutual’s industry-leading dividend-paying whole life insurance products.

Why #2: MassMutual holds the highest possible financial strength rating (A++) and paid a record $2.5 billion dividend to policyholders. Their whole life products are widely considered the gold standard for cash value accumulation and infinite banking strategies. Converting a MassMutual term policy gives you access to these products without new underwriting.

Key Conversion Advantages

- Top-Tier Whole Life Access: Convert to industry-leading dividend-paying whole life policies

- A++ Financial Strength: Among the highest-rated insurers in America

- Record Dividends: $2.5 billion distributed to policyholders

- No-Exam up to $20M: Industry-leading accelerated underwriting limits

- Age 90 Renewability: Extended coverage options for long-term planning

Best For: Sophisticated investors who want access to the strongest possible permanent life insurance products. Ideal foundation for infinite banking strategies requiring maximum cash value accumulation.

Complete analysis: MassMutual insurance review.

3. Guardian Life — Best for Complex Health and Business Situations

![]()

Financial Strength Ratings

- AM Best: A++ (Superior)

- S&P: AA+

- Moody’s: Aa2

- Company Type: Mutual

Product: Level Term with conversion to Guardian’s whole life products. Note that Guardian’s base conversion benefit covers the first five years; an Extended Conversion Rider (ECR) extends conversion rights for the full term length.

Key Conversion Advantages

- Whole Life Conversion: Convert to Guardian’s participating whole life — a mutual company product with dividends (paid annually since 1868)

- Health Condition Expertise: Specialized underwriting for diabetes, HIV, and other conditions

- Business Owner Focus: Sophisticated underwriting for complex business situations

- Low Complaint Ratios: Superior customer service and claims handling

- Mutual Company Benefits: Policyholder-owned structure aligned with long-term interests

Best For: Business owners with complex health histories or unique underwriting situations who still want access to mutual company whole life products. When other carriers decline coverage, Guardian’s specialized underwriting often finds a path to approval.

In-depth analysis: Guardian Life insurance review.

4. Pacific Life — Best Conversion Credits and Cash Benefits

![]()

Financial Strength Ratings

- AM Best: A+ (Superior)

- S&P: AA-

- Moody’s: Aa3

- Company Type: Mutual Holding

Product: PL Promise Term — 10, 15, 20, 25, and 30-year terms with conversion available during the level-premium period or until age 70, whichever comes first. New pricing released January 2026.

Key Conversion Advantages

- Cash Conversion Credits: Substantial credits reduce permanent policy first-year costs

- Multiple Permanent Options: Access to both whole life and universal life products

- High Customer Satisfaction: Consistently strong J.D. Power ratings

- Flexible Underwriting: No-exam options for ages 18-60 meeting health criteria

- Long-term Stability: Strong financial ratings across all major agencies

Best For: Investors who prioritize conversion credits and want access to a broad range of permanent products. Pacific Life’s generous cash credits at conversion can save thousands on the transition to permanent coverage.

Comprehensive details: Pacific Life insurance review.

5. Protective Life — Best Value with High Coverage Limits

![]()

Financial Strength Ratings

- AM Best: A+ (Superior)

- S&P: AA-

- Moody’s: A1

- Company Type: Stock (subsidiary of Dai-ichi Life)

Product: Classic Choice Term — 10 to 40-year terms (the longest available alongside Banner Life) with coverage up to $50M.

Key Conversion Advantages

- Up to 40-Year Terms: Among the longest level-premium terms available

- Multiple Conversion Options: Six different permanent policy options including whole life and universal life

- $50M Coverage Limits: Substantial capacity for business and estate planning

- Income Provider Option: Unique structured death benefit payout feature

- No-Exam up to $1M: For ages 18-45

Best For: Business owners needing substantial coverage limits at competitive rates with future conversion flexibility. Protective’s 40-year term and $50M limits make it ideal for key person protection and business succession planning where the sheer amount of coverage matters most.

Detailed analysis: Protective Life insurance review.

Beyond the Basics: A Smarter Starting Point

If conventional advice has left you sensing something’s missing, consider this: the best whole life insurance companies offer term riders that can be added directly to a whole life policy. This means you can start with a smaller base whole life policy and attach a term rider for the additional coverage you need — then gradually convert that term rider to paid-up additions as your budget allows.

This approach gives you immediate permanent coverage and affordable term protection in one policy, with built-in flexibility to shift the balance as your income grows. It’s the strategy sophisticated wealth builders use to get the best of both worlds without the limitations of a standalone convertible term policy. Learn more about how this integrates with infinite banking →

Conversion Feature Comparison: Top 5 Companies at a Glance

| Feature | Penn Mutual | MassMutual | Guardian | Pacific Life | Protective |

|---|---|---|---|---|---|

| Converts to Whole Life? | ✓ Participating WL | ✓ Participating WL | ✓ Participating WL | ✓ WL + UL options | ✓ WL + UL (6 options) |

| Company Type | Mutual | Mutual | Mutual | Mutual Holding | Stock |

| Dividends Paid? | ✓ 6%+ rate | ✓ $2.5B total | ✓ Since 1868 | Varies by product | N/A (stock company) |

| Conversion Credits | Annual premium credit | Varies | Varies | Generous cash credits | Varies |

| No-Exam Limits | Up to $5M (ACE) | Up to $20M | Varies | Ages 18-60 | Up to $1M (18-45) |

| Term Lengths | 10, 15, 20, 30 | 10, 15, 20 | 10, 15, 20, 30 | 10, 15, 20, 25, 30 | 10-40 years |

| AM Best Rating | A+ (Superior) | A++ (Superior) | A++ (Superior) | A+ (Superior) | A+ (Superior) |

| Best For | Overall wealth building + IBC | Maximum cash accumulation | Complex health/business | Conversion credit savings | High coverage + long terms |

Conversion features and availability may vary by state and are subject to change. Confirm current details with each carrier before applying. Dividends are not guaranteed.

Real Conversion Results: What Actually Happens When You Convert

Understanding conversion in theory is one thing. Seeing what happens with real clients is another.

Case Study: Health Protection Through Original Rate Class Conversion

Client Profile: 57-year-old female professional

Initial Coverage: 10-year convertible term life insurance policy

Conversion Decision (8 years into term): Converted $1 million of term coverage to whole life insurance

Conversion Results

- Immediate Cash Value Credit: $1,400 credited upon conversion

- Conversion Flexibility: Could convert anywhere from $50,000 to $1,000,000

- Health Protection: Converted at original health classification despite 8 years of potential health changes

- Strategic Timing: Converted near end of 10-year term period for maximum value

Key Takeaway: This client locked in permanent coverage at favorable rates regardless of any health changes over 8 years — something that would have been impossible with a standalone new policy application at age 57.

Note: This case study reflects an actual client outcome. Individual results vary based on carrier, health classification, timing, and specific policy terms.

Case Study: Business Owner Phased Conversion Strategy

Initial Need (Age 35): Business owner needs $5M coverage for key person protection and family income replacement. Starts with a convertible term policy at $180/month.

Phase 1 — Business Growth (Age 45): Company value has increased and tax situation is more complex. Converts $2M to whole life for tax-advantaged cash accumulation while maintaining $3M in term coverage.

Phase 2 — Wealth Optimization (Age 55): Converts remaining term coverage to complete an infinite banking strategy, creating tax-free retirement income and a legacy planning foundation.

Outcome: Total premium outlay over 20 years on the term portion: $43,200. At age 55: $2.8M in death benefits plus $320,000 in accessible cash value. Without conversion options, this phased integration would have required new underwriting at each stage — likely at significantly higher costs or with potential for decline.

Premiums shown are illustrative examples based on typical market rates. Actual rates depend on health, state, and underwriting class. Cash value projections are illustrative and not guaranteed.

Conversion Mistakes That Cost People Coverage

Conversion rights are valuable, but only if you use them correctly. These are the most common mistakes we see — and every one of them is avoidable.

1. Missing the Conversion Deadline

Every convertible term policy has a conversion window defined in the contract. Some carriers allow conversion until age 70. Others restrict it to the first 5 years unless you buy an extended conversion rider (Guardian, for example). Once that window closes, you lose the right entirely — no exceptions, no extensions. If your health has changed, you may not qualify for new coverage at any price.

What to do: Know your policy’s exact conversion deadline. Put it on your calendar a full year before it expires so you have time to plan strategically.

2. Not Checking What You Can Convert To

This is the mistake most comparison sites help people make. You buy the cheapest convertible term from a carrier with great rates, then discover at conversion time that your only option is a universal life product with no guaranteed cash value. If your strategy requires whole life — for infinite banking, for guaranteed growth, for dividends — you need to verify the permanent product options before you buy the term policy.

What to do: Ask specifically: “What permanent products are available for conversion?” and confirm whole life is among them if that’s your goal.

3. Waiting Too Long to Convert

Conversion preserves your original health classification, but your permanent policy premiums are based on your current age at conversion. Converting at 60 costs significantly more than converting at 45, even with the same health rating. Every year you wait increases the permanent premium.

What to do: Don’t wait until the last minute. If you know you want permanent coverage, earlier conversion means lower ongoing premiums and more time for cash value to grow.

4. Converting the Wrong Amount

Most policies allow partial conversion — converting a portion of your term coverage while keeping the rest as term. But some carriers set minimum conversion amounts, and others may restrict how many times you can convert. Converting too little may not create enough cash value to be useful. Converting everything at once may strain your budget.

What to do: Work with an advisor who can model different conversion amounts against your cash flow and long-term goals.

5. Ignoring Carrier Ownership Changes

When an insurance company is acquired, the new owner generally honors existing contractual obligations — including conversion rights. However, the permanent product portfolio available for conversion may change. Banner Life, for example, was acquired by Meiji Yasuda (completed February 2026). While existing policies remain in force, the long-term product landscape may evolve under new ownership.

What to do: If your carrier has been acquired or is pending acquisition, review your conversion options sooner rather than later while the current product lineup is still available.

Key Takeaway: Conversion Rights Are Use-It-or-Lose-It

The conversion feature in your term policy is a contractual right with an expiration date. Unlike most financial decisions, you can’t go back and redo this one. Get the timing, the amount, and the target product right the first time — or work with someone who can help you plan it strategically.

How to Choose the Right Convertible Term Company

Selecting the best convertible term life insurance requires thinking backwards from where you want to end up — not just where you are today.

Start With the Permanent Product

If you plan to eventually convert to whole life for cash accumulation or infinite banking, choose a carrier whose whole life products you’d want to own for decades. Penn Mutual, MassMutual, and Guardian all offer participating whole life from mutual companies. That should narrow your term search considerably.

Evaluate Financial Strength for the Long Term

Conversion rights are only as valuable as the company backing them. Prioritize carriers with A+ or better AM Best ratings and strong secondary ratings. Your conversion may be 10-20 years away — you need confidence the carrier will still be strong when you exercise it.

Compare Conversion Credits

Conversion credits reduce first-year permanent policy premiums and can save thousands. Penn Mutual’s annual premium credit and Pacific Life’s cash credits are among the most generous. Factor these into your total cost of conversion, not just the term premium.

Consider Your Health and Business Situation

If you have health conditions, Guardian Life’s specialized underwriting may get you approved where others decline. If you need $10M+ in coverage for business applications, Protective Life’s $50M limits and 40-year terms provide the most capacity.

Work With Someone Who Understands Conversion Strategy

Digital platforms excel at price comparison, but convertible term life insurance selection is a strategy decision, not a commodity purchase. The right advisor helps you map conversion timing to your financial goals, not just find the lowest monthly premium.

When Professional Guidance Adds Value

Straightforward applications with clear needs can be handled online. But business owners, high-net-worth individuals, and anyone planning a phased conversion strategy benefit from working with advisors who understand both insurance products and advanced financial strategies. The difference between the right and wrong conversion decision can be tens of thousands of dollars over a lifetime.

Honorable Mentions: Other Convertible Term Companies Worth Considering

These companies didn’t make the top 5 for conversion-specific value but remain strong options depending on your situation:

| Company | Best For | Key Note |

|---|---|---|

| Banner Life | Competitive pricing, 40-year terms | Converts to UL only (not whole life). Acquired by Meiji Yasuda, Feb 2026. |

| Prudential | Senior and executive applications | PruFast Track no-exam up to $1M. Strong international capabilities. |

| Lincoln Financial | Digital experience + conversion flexibility | LincXpress no-exam up to $1M for ages 18-60. |

| John Hancock | Wellness incentives | Vitality program rewards healthy behaviors with premium discounts. |

| Principal Financial | Balanced approach | Accelerated underwriting up to $2.5M for ages 18-60. |

A Note on Banner Life

Banner Life has been #1 on most “best convertible term” lists for years — including ours, previously — thanks to competitive pricing, 40-year terms, and conversion until age 70. Those are real advantages. However, Banner’s OPTerm converts only to their Life Step UL (universal life), not whole life. For buyers who simply want affordable term with a permanent option, Banner remains excellent. For buyers planning to convert to participating whole life for infinite banking or wealth building, the mutual carriers above are better aligned. The February 2026 acquisition by Meiji Yasuda also introduces ownership uncertainty worth monitoring.

Frequently Asked Questions About Convertible Term Life Insurance

Can I convert term life insurance to whole life without a medical exam?

A: Yes. That’s the core benefit of convertible term life insurance. You convert to permanent coverage using your original health classification — no new medical exam, no health questions, no underwriting. If you were approved as “Super Preferred” at 35 but developed diabetes by 50, you still convert at your original rating. The key is to confirm your policy includes a conversion privilege and to convert before the deadline in your contract.

What happens if I miss my conversion deadline?

A: You lose the conversion right permanently. There are no extensions or exceptions. If your health has changed, you may face significantly higher premiums on a new policy — or outright denial. This is why knowing your exact conversion deadline is critical. Check your policy contract for the specific language and mark the date well in advance.

How much more does whole life cost after converting from term?

A: Permanent premiums are based on your age at the time of conversion, not your original age when you bought the term policy. A 45-year-old converting a $500,000 policy will pay significantly more than a 35-year-old converting the same amount. However, conversion preserves your health classification, which can offset the age-based increase substantially — especially if your health has declined since you bought the term policy. Some carriers also offer conversion credits that reduce first-year permanent premiums.

Can I convert just part of my term policy?

A: Most carriers allow partial conversion — converting a portion of your term coverage while keeping the rest as term insurance. This is a common strategy for phasing into permanent coverage as your budget allows. Some carriers set minimum conversion amounts (such as $50,000), and some limit how many partial conversions you can make. Check your specific policy terms.

Which companies let you convert to whole life vs. universal life?

A: This varies significantly by carrier and is the most overlooked factor in convertible term selection. Mutual companies like Penn Mutual, MassMutual, and Guardian typically allow conversion to their participating whole life products. Some carriers — like Banner Life — only convert to universal life. If your long-term strategy depends on whole life cash value, guaranteed growth, and dividends, confirm the conversion options before purchasing the term policy.

Is it better to convert my term or buy a new whole life policy?

A: If your health is the same or better than when you bought the term policy, get quotes for a new whole life policy and compare. You may find better options or pricing. If your health has declined, conversion is almost always the better path — it preserves your original health rating, which may save tens of thousands in premiums. Also consider that the best whole life policies offer term riders and paid-up addition flexibility that let you build a comprehensive strategy from day one.

Do conversion credits actually save money?

A: Yes — conversion credits reduce first-year permanent policy premiums and can represent meaningful savings. Penn Mutual offers a credit equal to your annual term premium. Pacific Life provides cash credits at conversion. These aren’t trivial — on a large policy, conversion credits can mean thousands of dollars in first-year savings. Factor credits into your carrier selection alongside premium pricing and permanent product quality.

What happens to my conversion rights if my insurance company is acquired?

A: Generally, the acquiring company honors existing contractual obligations, including conversion rights. Your policy is a legal contract and its terms survive an ownership change. However, the permanent product portfolio available for conversion may evolve under new ownership. Banner Life’s February 2026 acquisition by Meiji Yasuda is a current example — existing policyholders retain their rights, but the long-term product lineup may shift. If your carrier is going through an ownership change, it may be worth reviewing your conversion options sooner rather than later.

Ready to Choose the Right Convertible Term Strategy?

The difference between the right and wrong convertible term decision isn’t the monthly premium — it’s what you’re building toward. Our advisors help you match the right carrier, conversion timing, and permanent product to your actual financial goals.

In Your Complimentary Strategy Session, You’ll Discover:

- ✓ Which convertible term carrier best fits your conversion strategy

- ✓ Whether a term-with-conversion or whole-life-with-term-rider approach makes more sense

- ✓ Optimal conversion timing and phasing strategy

- ✓ How conversion integrates with infinite banking and estate planning

No obligation. Expert guidance from licensed professionals who understand advanced wealth strategies.