Co-authored by Denise Boisvert, Debt Elimination Specialist with 15+ years experience, and the Insurance & Estates advisory team.

Most homeowners think they have two choices with their mortgage: keep making payments for 30 years, or throw extra money at the principal and hope to shave off a few years. But there’s a third option that changes the equation entirely — and a fourth that most financial advisors won’t tell you about.

Using a high cash value whole life insurance policy in conjunction with the infinite banking concept you can either accelerate your mortgage payoff by a decade or more without increasing your monthly payments, or you can keep your mortgage as a strategic tool and build liquid wealth that gives you more control than a paid-off house ever could.

This guide walks you through both paths with real numbers so you can decide which one fits your situation — or whether a combination of both is the smartest move.

TL;DR: Two Paths for Your Mortgage Using Whole Life Insurance

- Path 1 — Accelerate Payoff: Use policy loans to make lump sum principal payments, cutting a 30-year mortgage to 13–15 years without increasing monthly payments

- Path 2 — Build Liquid Wealth: Keep your mortgage and redirect extra payments into cash value, creating an opportunity fund that outperforms trapped home equity

- Home equity doesn’t increase your home’s appreciation rate — a paid-off house and a mortgaged house appreciate identically

- The “investor’s definition” of debt-free: liquid assets exceed all liabilities, not mortgage balance equals zero

- Bottom Line: The right path depends on your income stability, investment appetite, and whether you want to eliminate debt or leverage it

Table of Contents

- The Mortgage Trap Most Americans Face

- Two Paths: Accelerate Payoff vs. Build Liquid Wealth

- Path 1: Pay Off Your Mortgage in Half the Time

- Path 2: Keep Your Mortgage, Build Wealth Instead

- Which Path Is Right for You?

- Side-by-Side: Both Paths vs. Traditional Methods

- What Happens After: Two Post-Payoff Scenarios

- Common Questions About Mortgage Strategies with Whole Life

The Mortgage Trap Most Americans Face

When you make a traditional mortgage payment, you’re essentially renting your home from the bank for the first 10–15 years. Your hard-earned money benefits the lender far more than your own wealth.

Interest-Heavy Payments

In a conventional 30-year mortgage, approximately 70–80% of your early payments go toward interest, not principal. On a $250,000 mortgage at 4.5%, your first monthly payment of $1,267 includes only $267 toward principal and $1,000 toward interest. After years of payments, you’re barely closer to owning your home outright.

The Illiquidity Trap

The equity you do build is locked in your property, inaccessible without significant hurdles — applying for a HELOC (requiring qualification, credit checks, and closing costs), refinancing (incurring fees and potentially a new 30-year term), or selling your home entirely. This lack of liquidity limits your ability to respond to emergencies or seize investment opportunities.

The Opportunity Cost

Every dollar sent to the mortgage company is a dollar that could be growing elsewhere. Traditional financial advice fixates on “getting out of debt” without acknowledging the wealth-building potential of those funds. Many homeowners overlook mortgage-related opportunity costs, missing chances to grow assets that could outpace their mortgage interest.

Two Paths: Accelerate Payoff vs. Build Liquid Wealth

Both strategies use the same tool — a properly structured high cash value whole life insurance policy. The difference is what you do with the cash value once it accumulates.

| Path 1: Accelerate Payoff | Path 2: Build Liquid Wealth | |

|---|---|---|

| Goal | Eliminate mortgage in 13–15 years | Build $500K+ liquid opportunity fund |

| Strategy | Policy loans → lump sum principal payments | Keep mortgage, redirect extra payments into policy |

| Best For | Homeowners who want debt-free peace of mind + wealth building | Investors who want maximum liquidity and asset acquisition potential |

| Risk Profile | Lower — eliminates debt while building asset | Moderate — requires discipline to deploy capital productively |

| Liquidity | Cash value accessible throughout, grows after payoff | Full liquidity maintained at all times |

Many homeowners start with Path 1 and transition to Path 2 after payoff. Others choose Path 2 from the start because they understand that a mortgage at 5% is a profitable tool when your capital earns more elsewhere. Let’s look at how each works with real numbers.

Path 1: Pay Off Your Mortgage in Half the Time

This is the strategy Denise teaches clients every day. Instead of making extra monthly payments or refinancing to a shorter term, you use policy loans from your whole life insurance to make strategic lump sum payments directly against your principal — slashing years off your mortgage without increasing your monthly outflow.

How It Works

The strategy unfolds in three phases. First, you redirect discretionary income into a properly designed policy with paid-up additions to accelerate cash value growth. Second, as your policy’s cash value grows tax-free, you maintain complete access to these funds — unlike home equity. Third, once sufficient cash value accumulates, you borrow against your policy to make lump sum payments directly to your mortgage principal. Your cash value continues earning interest and dividends while the principal payments slash your mortgage term.

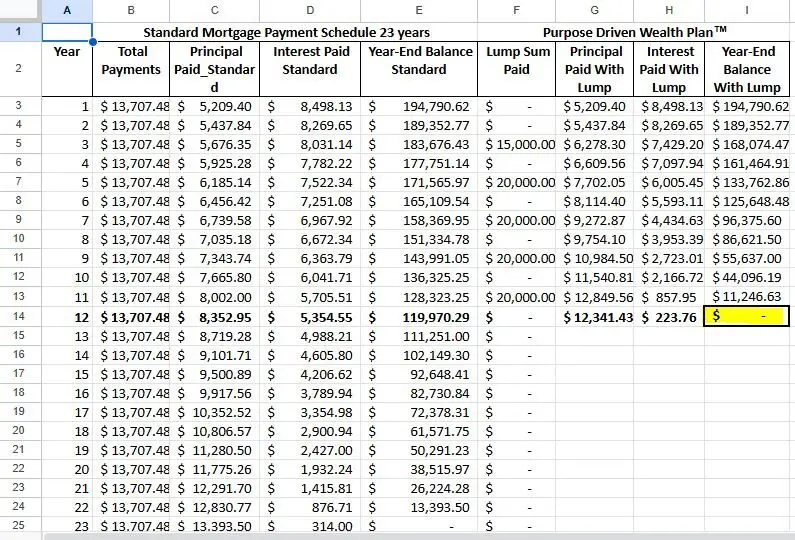

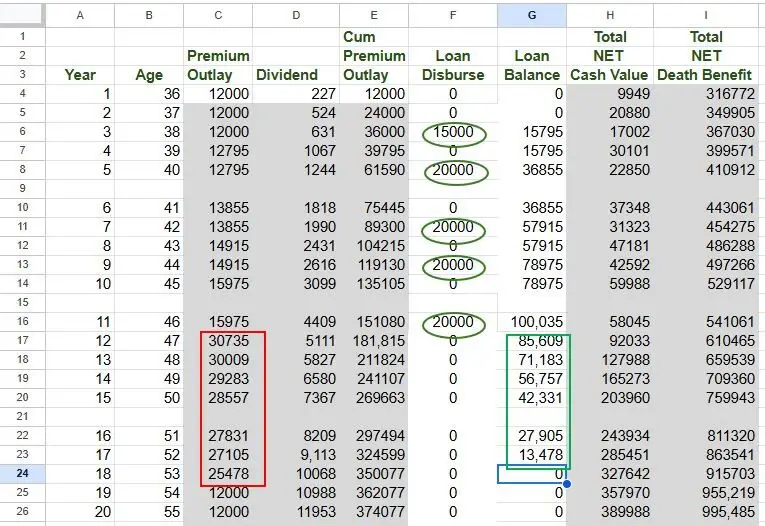

Real Numbers: A $195,000 Mortgage

Starting scenario: $195,000 mortgage balance, 23 years remaining, $1,100 monthly payment ($13,707 annually).

With a properly structured policy, the homeowner executes the following moves:

| Policy Year | Lump Sum to Principal | Impact |

|---|---|---|

| Year 3 | $15,000 | First principal reduction, saves years of interest |

| Year 5 | $20,000 | Mortgage balance dropping faster than amortization schedule |

| Year 7 | $20,000 | Principal-to-interest ratio shifts dramatically in your favor |

| Year 9 | $20,000 | Mortgage payoff within sight |

| Year 11 | $20,000 | Final lump sum — mortgage eliminated |

The Results

Traditional schedule (after 12 years): approximately $120,000 still owed, 11 years of payments remaining.

Path 1 strategy: Mortgage paid off in 13 years, saving 10 years of payments (~$137,000) and eliminating tens of thousands in interest — all while building a cash value asset that continues growing after the mortgage is gone.

Case Study: Sarah’s $300,000 Mortgage

Sarah, a 40-year-old teacher, had a $300,000 mortgage at 4% over 30 years with a $1,432 monthly payment. Frustrated by slow equity growth, she started a whole life policy contributing $10,000 annually. By year 4, her cash value reached $38,000, and she borrowed $20,000 to reduce her principal. She repeated this every 2–3 years. By year 14, her mortgage was paid off — saving 16 years and approximately $170,000 in payments. Her cash value hit $150,000 by age 55, offering tax-free income potential.

Path 2: Keep Your Mortgage, Build Liquid Wealth Instead

Path 2 flips the conventional wisdom entirely. Instead of rushing to eliminate your mortgage, you keep it as a strategic tool and direct extra capital into your whole life policy — building liquid wealth that gives you financial control a paid-off house never can.

Why Your Home Equity Earns Zero Return

This is the concept that changes everything: your home appreciates based on market conditions, not your equity position.

Consider two identical homes in the same neighborhood, both valued at $300,000. Home A has a $200,000 mortgage (33% equity). Home B is owned free and clear (100% equity). If property values increase by 5% over the year, both homes appreciate to $315,000 regardless of equity. The owner of Home A gains $15,000 with $100,000 tied up. The owner of Home B gains the same $15,000 with $300,000 tied up.

Paying down your mortgage faster doesn’t increase your home’s rate of appreciation. It simply converts liquid cash into illiquid equity without improving the asset’s performance.

Would You Fire a Profitable Employee?

Imagine you’re a business owner with an employee you pay $40,000 per year. That employee generates $80,000 in annual returns. Would you fire that employee to “save” the salary expense? Of course not.

Your mortgage works the same way. When you have a mortgage at 5% interest and you’re earning higher returns on capital in your whole life policy, your mortgage isn’t a burden — it’s a profitable employee. By rushing to pay it off, you’re eliminating the opportunity to earn returns on that capital.

The Real Definition of “Out of Debt”

Most people define “out of debt” as owing nothing. Wealthy individuals use a different definition based on their balance sheet.

Person A: $500,000 home, fully paid off. $50,000 in savings. Liquid assets: $50,000.

Person B: $500,000 home with $400,000 mortgage. $450,000 in whole life cash value. Liquid assets: $450,000.

Both have $550,000 in net worth. But Person B can borrow up to $400,000 against their policy tomorrow to acquire an income-producing asset — without selling anything, without bank approval, and while their full cash value continues compounding. Person A’s equity is trapped, earning zero return, accessible only by selling or refinancing.

Real-World Proof: The 2008 Housing Crisis

In December 2007, a financial strategist refinanced his $1.5 million residence at 100% loan-to-value, extracting all equity and placing it into liquid cash value life insurance policies.

By 2008, his home’s market value dropped to $1.1 million — a $400,000 decline. But he didn’t lose money. The $400,000 he extracted was safely positioned in his policies, continuing to earn returns while he used policy earnings to make mortgage payments comfortably.

Homeowners who lost properties during 2008–2010 weren’t those with high loan-to-value ratios and liquid reserves. They were those who lost income, had equity trapped in declining homes, and couldn’t access capital when they needed it most.

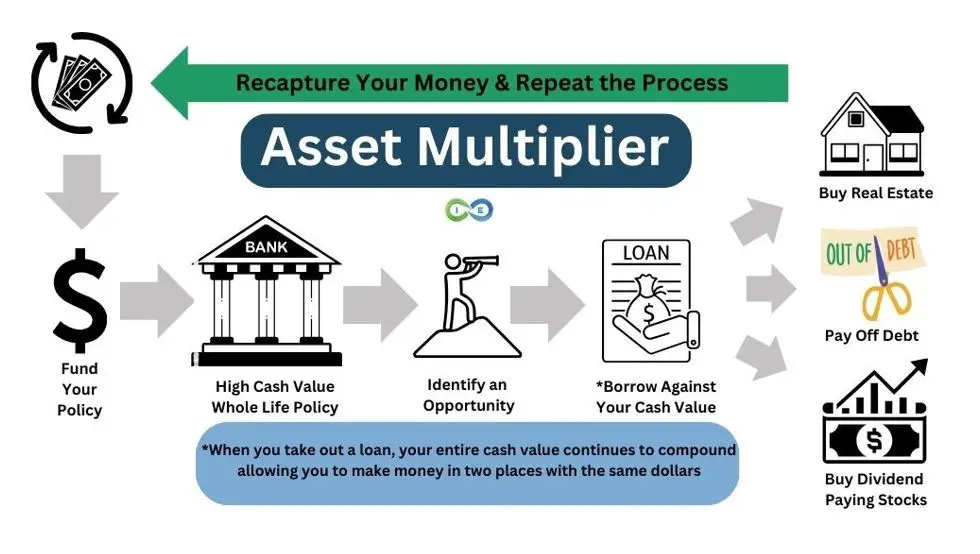

The Asset Multiplier Approach

This is where Path 2 creates exponential results. You use your policy’s cash value as an opportunity fund to acquire income-producing assets through the Asset Multiplier Blueprint:

First, fund your policy over time, building your opportunity fund. Then, take a loan against your cash value to purchase income-producing assets like rental properties or businesses. Use the income from those assets to repay the policy loan and continue funding the policy. Then repeat. This allows you to own multiple appreciating assets simultaneously — your home, your policy’s growing death benefit and cash value, and income-producing real estate.

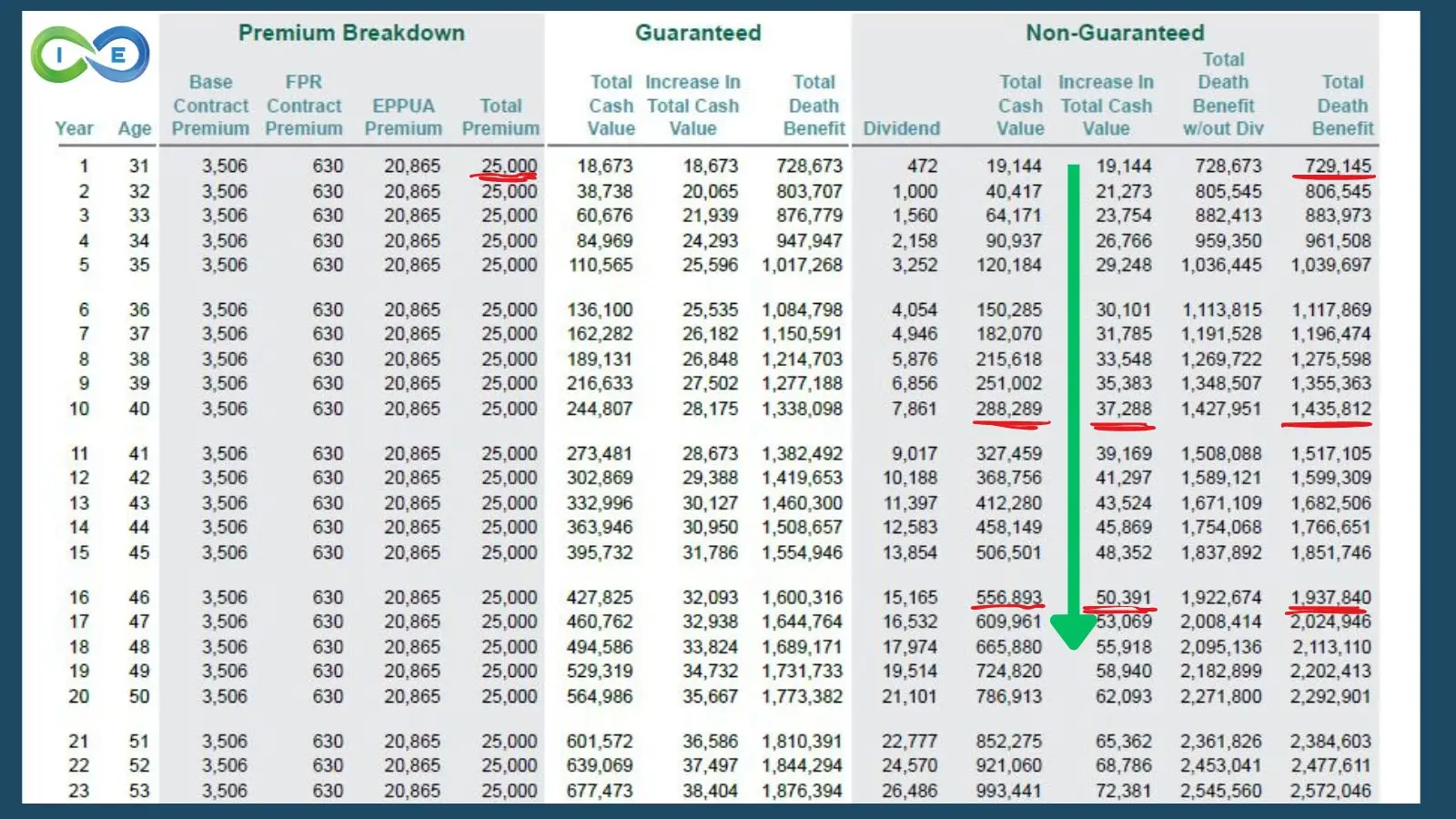

Path 2 in Action: Chris’s $25,000 Annual Policy

Chris, age 30, funds a whole life policy at $25,000 per year instead of making extra mortgage payments.

| Year | Age | Total Cash Value | Total Death Benefit | Milestone |

|---|---|---|---|---|

| 1 | 31 | $19,144 | $729,145 | Day-1 death benefit covers most mortgages |

| 5 | 35 | $120,184 | $1,039,697 | Cash value crosses $100K; death benefit exceeds $1M |

| 10 | 40 | $288,289 | $1,435,812 | Opportunity fund ready for first rental property acquisition |

| 15 | 45 | $506,501 | $1,851,746 | Cash value exceeds typical mortgage balance |

| 20 | 50 | $786,913 | $2,292,901 | Liquid wealth approaching $800K |

| 23 | 53 | $993,441 | $2,572,046 | Cash value approaches $1M — home appreciated separately the entire time |

| Key Insight: By year 15, Chris has $506K in liquid, accessible capital he can borrow against to acquire income-producing assets — versus the same $506K trapped in home equity earning 0% and accessible only by selling or refinancing. His death benefit also provides a $1.85M permission slip to spend other assets while still leaving an inheritance.

Illustration based on actual carrier data for a healthy male, age 31, preferred plus rate class. Includes non-guaranteed dividends based on current scale. Your results will vary based on age, health, and carrier selection. |

||||

Which Path Is Right for You?

The right path depends on your situation, not a one-size-fits-all rule. Here’s a framework to help you decide:

| Your Situation | Best Path | Why |

|---|---|---|

| Stable income, want debt gone, value peace of mind | Path 1 | You build a wealth asset while eliminating your largest liability |

| Active investor, want to acquire income-producing assets | Path 2 | Liquid capital lets you seize opportunities a paid-off house can’t |

| Young (under 40), long time horizon, higher risk tolerance | Path 2 | Compound time magnifies the Asset Multiplier approach |

| Nearing retirement, want to reduce fixed expenses | Path 1 | Eliminating the payment frees cash flow for retirement spending |

| High mortgage rate (6%+), lower policy loan rate | Path 1 | The rate spread favors eliminating the higher-cost debt |

| Low mortgage rate (under 5%), want maximum optionality | Path 2 | Your cheap debt is a “profitable employee” — keep it working |

| Want the best of both worlds | Path 1 → Path 2 | Accelerate payoff first, then redirect mortgage payments into policy for wealth building |

Side-by-Side: Both Paths vs. Traditional Methods

| Method | Time Saved | Monthly Cost Increase | Liquidity | Wealth Built | Death Benefit |

|---|---|---|---|---|---|

| Biweekly Payments | 4–5 years | ~8% | Locked in home | None | None |

| Extra Principal ($500/mo) | 8–10 years | ~30–50% | Locked in home | None | None |

| 15-Year Refinance | 15 years | 30–50% | Locked in home | None | None |

| Path 1: Accelerate Payoff | 15–17 years | None | Full access | Significant | ✓ Growing |

| Path 2: Build Liquid Wealth | 0 (strategic) | None | Full access | Maximum | ✓ Growing |

| Best For: Traditional methods trade liquidity for debt reduction. Path 1 eliminates debt while preserving liquidity and building wealth. Path 2 maximizes wealth building and optionality for active investors willing to maintain strategic debt. Both paths include a growing death benefit that traditional methods cannot provide. | |||||

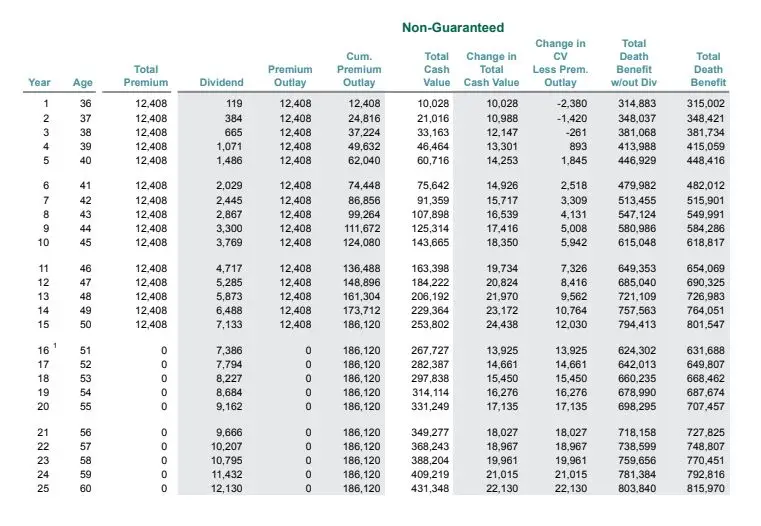

What Happens After: Two Post-Payoff Scenarios

Once your mortgage is paid off through Path 1, your whole life policy offers two compelling next moves:

Option A: Never Repay Policy Loans

Concerned about the ~$100,000 in policy loans from the payoff example? You don’t need to repay them. Your cash value and death benefit continue growing. By age 60: cash value reaches approximately $470,000 and death benefit exceeds $1,000,000. You’ve paid off your home and built significant wealth even with outstanding loans.

Option B: Redirect Mortgage Payments into the Policy

For greater impact, redirect your $1,100 monthly mortgage payment to repay policy loans. By age 60: cash value reaches approximately $578,000 and death benefit exceeds $1,200,000. This transitions seamlessly to tax-free retirement income via policy loans.

Common Questions About Mortgage Strategies with Whole Life

How do I use a whole life policy to pay off my mortgage faster?

You fund a properly structured whole life policy for several years to build cash value, then borrow against that cash value to make lump sum payments directly to your mortgage principal. These principal reductions slash years off your mortgage because they eliminate the future interest those dollars would have generated. Your cash value continues earning dividends on the full amount even while borrowed against — so your money works in two places simultaneously.

Should I pay off my mortgage early or build cash value instead?

It depends on your mortgage rate, age, income stability, and investment appetite. If you want peace of mind and are nearing retirement, accelerating payoff (Path 1) makes sense. If you’re younger with a low-rate mortgage and want to acquire income-producing assets, building liquid wealth (Path 2) often creates more total wealth over time. Many people start with Path 1 and transition to Path 2 after payoff.

Does paying down my mortgage faster increase my home’s value?

No. Your home appreciates based on market conditions, not your equity position. Two identical homes — one mortgaged, one paid off — appreciate at exactly the same rate. Extra principal payments convert liquid cash into illiquid equity without improving the asset’s return. This is one of the most misunderstood concepts in personal finance.

What happens to my policy loans after the mortgage is paid off?

You have options. You can repay them using redirected mortgage payments, which accelerates your cash value growth significantly. Or you can leave them outstanding — your policy continues compounding on the full cash value regardless. Outstanding loans reduce your death benefit but don’t reduce your wealth or your policy’s growth trajectory.

Is it better to get a 15-year mortgage or a 30-year with whole life?

In most cases, the 30-year mortgage combined with a whole life policy outperforms the 15-year mortgage. The lower monthly payment on the 30-year frees up cash to fund your policy. Over 20–30 years, the compounding cash value and growing death benefit typically exceed the interest savings from the shorter mortgage — while maintaining full liquidity the entire time. The 15-year mortgage locks you into higher payments with zero flexibility.

How much cash value do I need before making my first lump sum payment?

Generally, you want your cash value to be near or above total premiums paid before taking your first loan, which typically occurs around year 3–5 depending on policy design. The first lump sum is usually $15,000–$20,000 — enough to make a meaningful dent in principal. Your advisor will help you time this based on your specific policy performance and mortgage balance.

What if I sell my house before the mortgage is paid off?

Your whole life policy is completely portable — it has nothing to do with your property. If you sell, apply proceeds to your next home or redirect funds to other goals. Your policy remains intact with full cash value access. This is a major advantage over traditional payoff methods that leave your investment locked inside a specific property.

Can I use this strategy if I already have a mortgage?

Absolutely. Most clients start this strategy with an existing mortgage. You don’t need to refinance or modify your current loan. You simply begin funding a whole life policy alongside your existing payments, and once cash value builds sufficiently, you start making lump sum principal payments (Path 1) or deploying capital into income-producing assets (Path 2). The strategy works regardless of where you are in your mortgage term.

Ready to See Which Path Works for Your Mortgage?

Before choosing between accelerating your payoff or building liquid wealth, get a personalized analysis from Denise Boisvert. She’ll show you exactly how both paths could work with your specific mortgage, income, and financial goals — so you can make the right decision with real numbers, not guesswork.

- ✓ See your personalized mortgage payoff timeline for Path 1

- ✓ Compare projected wealth accumulation for Path 2

- ✓ Discover which approach — or combination — fits your situation

- ✓ Get a customized policy design recommendation from an independent advisor

No obligation. No sales pressure. Just expert guidance to help you determine which mortgage strategy builds the most wealth for your family.

Go Deeper with Denise’s Book: Designing a Debt-Free Life

Discover how to use high cash value life insurance as a tax-free strategy for financial freedom — including the complete mortgage elimination playbook.

- ✓ Eliminate credit card debt without cutting your lifestyle

- ✓ Wipe out your mortgage years early with no extra income

- ✓ Fund major purchases without using traditional banks

- ✓ Create generational wealth with tax-free growth