Most insurance companies keep your cash value when you die, paying only the death benefit to your beneficiaries—but this isn’t the full story. With expert policy design focused on growing both cash value and death benefit simultaneously, your beneficiaries can receive significantly more than the original face amount. Our specialized approach ensures your whole life insurance policy becomes a powerful wealth transfer vehicle, not just a death benefit check.

TL;DR: What Happens to Whole Life Cash Value at Death

- Standard policies: Insurance company keeps cash value, pays only death benefit

- Properly designed policies: Death benefit GROWS to include cash value accumulation

- Key strategy: Paid-up additions (PUAs) increase BOTH cash value AND death benefit

- Real example: $500K policy can become $1.5-2.5M legacy over 30 years

- Bottom Line: Policy design determines whether your family gets the cash value—not the insurance company

Table of Contents

- Cash Value vs. Death Benefit: What’s the Difference?

- What Happens to Whole Life Cash Value When You Die?

- Standard Policies vs. Properly Designed Policies

- How the Death Benefit Grows to Include Cash Value

- How to Maximize What Your Beneficiaries Receive

- Can You Use Cash Value While You’re Still Alive?

- Frequently Asked Questions

Cash Value vs. Death Benefit: What’s the Difference?

Understanding the difference between cash value and death benefit is essential before you can understand what happens to each when you die.

The cash value (also called cash surrender value) is the savings component built into a whole life insurance policy. It grows over time through a guaranteed rate of return and optional dividends, and you can access it during your lifetime through loans or withdrawals.

The death benefit is the amount the insurance company pays your beneficiaries when you die, minus any outstanding policy loans.

Industry Insight: Many policyholders and even some financial advisors misunderstand that cash value typically does not automatically transfer to beneficiaries. This misunderstanding is one of the most common complaints about whole life insurance policies. However, with proper policy design and riders, you can ensure your beneficiaries receive maximum value.

Here’s the critical point: in most standard whole life policies, these two components are linked but separate. As your cash value grows, so does your death benefit—but they don’t automatically combine at death unless the policy is designed that way. As the policy nears maturity (typically at age 120 or 121 for newly issued policies), the cash value equals the death benefit.

For a deeper look at how cash value builds over time with different policy designs, see our whole life insurance cash value chart comparing three policy structures.

What Happens to Whole Life Cash Value When You Die?

This is the question that brings most people to this page—and the answer depends entirely on how your policy is designed.

With a standard whole life policy, the insurance company keeps your cash value when you die. They pay only the stated death benefit to your beneficiaries. If you’ve accumulated $200,000 in cash value inside a policy with a $500,000 death benefit, your family receives $500,000—not $700,000. The $200,000 in cash value reverts to the insurance company.

This is a key point that many policyholders don’t understand until it’s too late. It’s also the reason critics like Dave Ramsey say “the insurance company keeps your money.” And for standard policies sold by most agents, he’s not wrong.

But with a properly designed policy, the outcome is completely different.

Standard Policies vs. Properly Designed Policies

The distinction comes down to what happens to your cash value growth over the life of the policy.

In a standard policy, the death benefit stays relatively flat. Cash value grows underneath it, but at death, only the original death benefit amount pays out. The insurance company absorbs the accumulated cash value.

In a properly designed policy using paid-up additions (PUAs) and dividend reinvestment, the death benefit itself grows over time. Each PUA purchase and each reinvested dividend adds a small chunk of fully paid-up insurance to your policy—increasing both your cash value and your death benefit simultaneously. When you die, your beneficiaries receive the full, grown death benefit—which now includes all that accumulated growth.

Put simply: with the right design, the cash value isn’t “kept” by the insurance company—it’s already been converted into a larger death benefit that your family receives in full.

Think of It Like Home Equity

Cash value life insurance is an asset similar to real estate. You can think of your policy like a mortgage for a home purchase. With each mortgage payment, you build up equity in the home until, after all the mortgage payments are made, you own the home outright. When you fully pay off the mortgage, you don’t have the home equity and the home as two separate assets. The equity is tied to the home. The cash value of a whole life policy can be viewed as interest-earning equity in the death benefit.

How the Death Benefit Grows to Include Cash Value

This is the mechanism that makes the difference. With dividend-paying whole life insurance from a mutual company, your death benefit actually INCREASES as the years go by—making your policy more valuable as time passes.

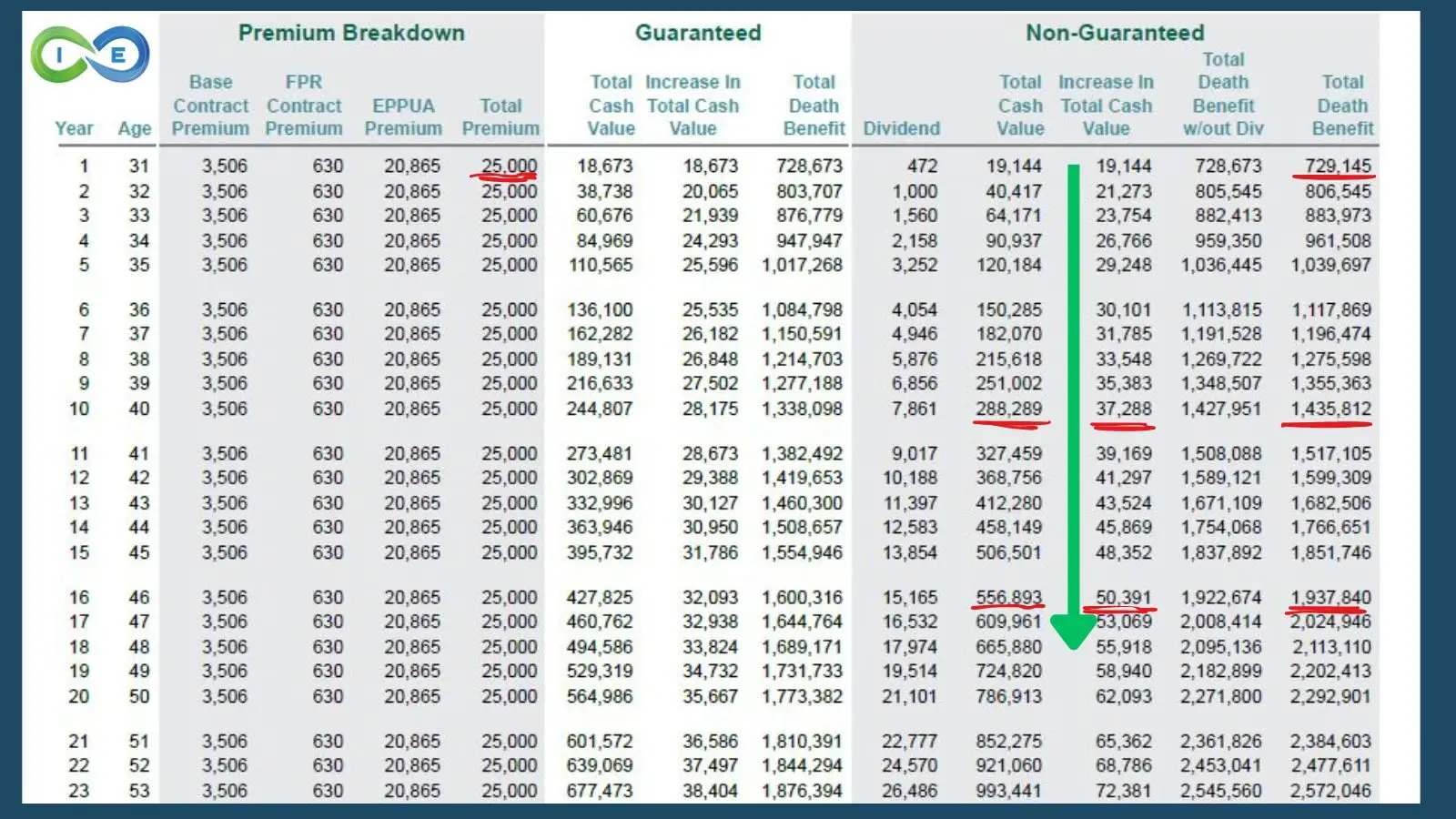

Policy Growth Example: $25,000 Annual Premium (Age 31 Start)

| Year | Age | Total Cash Value | Total Death Benefit | Growth Multiple |

|---|---|---|---|---|

| 1 | 31 | $19,144 | $729,673 | 1.0x (baseline) |

| 10 | 40 | $288,289 | $1,435,812 | 2.0x original death benefit |

| 23 | 53 | $993,441 | $2,572,046 | 3.5x original death benefit |

| Key Point: With proper policy design using paid-up additions, this death benefit grew from $728K to $2.57M—the beneficiaries receive the FULL $2.57M, not just the original $728K. The cash value growth is captured IN the death benefit, not lost to the insurance company.

Illustration based on actual carrier data. Your results will vary based on age, health, and carrier selection. |

||||

Notice what happened: the cash value and death benefit grew together. By year 23, the death benefit had more than tripled—from $728K to $2.57M. That growth came from paid-up additions and reinvested dividends compounding over time. The beneficiaries receive the full $2.57M. Nothing is “kept” by the insurance company.

This is the power of policy design. The same product—whole life insurance—produces completely different outcomes at death depending on how it’s structured. For a detailed comparison of how three different policy designs affect cash value growth, see our whole life insurance cash value chart.

How to Maximize What Your Beneficiaries Receive

At Insurance & Estates, we design policies differently than most insurance advisors. We focus on strategies that grow both the cash value and death benefit simultaneously, ensuring your beneficiaries receive much more than the original face amount when you pass away.

Here are the key strategies that determine how much your family actually receives at death:

- Paid-Up Additions (PUAs): These riders allow you to contribute additional money to your policy, purchasing small chunks of fully paid-up insurance that immediately add to both your cash value and death benefit. PUAs are the single most important factor in ensuring your cash value isn’t lost at death.

- Strategic Dividend Reinvestment: By directing dividends to purchase additional paid-up insurance rather than taking them as cash, you compound your policy’s growth over time. The best dividend-paying whole life companies have paid dividends every year for over a century.

- Policy Blending: Designing policies that blend base coverage with term riders and paid-up additions in precise ratios maximizes both immediate cash value and long-term death benefit.

- Carrier Selection: Not all insurance companies offer the same dividend history, PUA options, or policy design flexibility. Choosing the right carrier is critical to ensuring your death benefit grows to capture your cash value.

Expert Insight: Based on 18+ years of designing high cash value policies, a properly structured whole life policy can deliver 3-5 times the original death benefit after 30+ years through strategic use of paid-up additions and dividend reinvestment. This means a $500,000 policy could potentially provide a $1.5-2.5 million legacy for your beneficiaries.

It’s worth noting that certain riders and types of permanent life insurance other than traditional whole life are available that provide for payment of death benefits and accrued cash value. As you might suspect, though, premiums will be higher for a policy that pays out both.

Can You Use Cash Value While You’re Still Alive?

Yes—and how you use your cash value during your lifetime directly affects what your beneficiaries receive at death. If you tap the cash value for a withdrawal or a loan and don’t repay it, you decrease the death benefit. If you leave it alone or continue adding to it, the death benefit continues to grow.

Here’s a brief overview of your options, with links to our detailed guides on each:

Policy loans are the most powerful option. You borrow against your cash value while your full balance continues earning dividends. If repaid, your death benefit stays fully intact. Policy loans require no credit check, no mandatory repayment schedule, and don’t appear on your credit report.

Partial withdrawals let you access a portion of your cash value, but they permanently reduce your death benefit by the amount withdrawn. For a complete breakdown of all your options, see our guide on accessing cash value from life insurance.

Paying premiums with cash value becomes available once your policy reaches paid-up status—meaning enough cash value has accumulated that no further premium payments are required. This is particularly valuable for retirees.

Surrendering the policy cancels your coverage entirely. You receive the cash surrender value, but your beneficiaries lose all death benefit protection. This should generally be a last resort.

THE ULTIMATE FREE DOWNLOAD

The Self Banking Blueprint

A Modern Approach To The Infinite Banking Concept

Get a Custom Whole Life Strategy That Maximizes Both Cash Value AND Death Benefit

Unlike most advisors who sell standard policies where the insurance company keeps your cash value at death, our expert team designs policies specifically to grow both cash value and death benefit simultaneously.

- ✓ Receive a personalized policy design that ensures your beneficiaries get significantly more than the original face amount

- ✓ Learn how to use paid-up additions and dividends to maximize both living benefits and legacy

- ✓ Understand exactly how your cash value and death benefit will grow over time

- ✓ Get clarity on the optimal policy structure for your specific financial goals

Don’t settle for a standard policy where the insurance company keeps your cash value. Schedule your complimentary Whole Life Strategy Session today and discover how to maximize both cash value and death benefit.

No obligation. No sales pressure. Just expert guidance to help you design a policy that truly benefits your family for generations.

Frequently Asked Questions

Does the insurance company keep my cash value when I die?

In standard whole life policies, yes—the insurance company keeps the cash value and pays only the death benefit. However, with proper policy design using paid-up additions and dividend reinvestment, your death benefit grows to capture the cash value accumulation, so your beneficiaries receive significantly more than the original face amount.

Can my family get both the cash value AND death benefit?

With standard policies, no. But with properly designed policies, the death benefit increases to include the growth from your cash value. In our illustration, a $728K initial death benefit grew to $2.57M over 23 years—your beneficiaries receive the full $2.57M, not just the original amount.

Is Dave Ramsey right that insurance companies keep your cash value?

He’s partially right about standard policies sold by most agents. But he’s wrong about properly designed high cash value policies. When you use paid-up additions and dividend reinvestment, your death benefit grows WITH your cash value—so nothing is “kept” by the insurance company. The key is policy design, not the product itself.

What’s the difference between cash value and death benefit?

The cash value is the savings component you can access while living—through loans, withdrawals, or to pay premiums. The death benefit is what your beneficiaries receive when you die. In standard policies these are separate (and the company keeps the cash value). In properly designed policies, the death benefit grows to include cash value accumulation. For more detail, see our guide on cash value life insurance.

How do I make sure my beneficiaries get the cash value?

Work with an advisor who designs policies specifically to grow both cash value and death benefit simultaneously. The strategies include maximizing paid-up additions, reinvesting dividends into additional coverage, choosing the right dividend-paying carrier, and proper policy blending. This is exactly what we specialize in at Insurance & Estates.

Can I use my cash value while I’m still alive?

Yes. You can borrow against it tax-free, make partial withdrawals, use it to pay premiums once the policy is paid up, or surrender the policy entirely. Just remember—any amount you access and don’t repay will reduce what your beneficiaries receive at death. See our full guide on accessing cash value from life insurance.

How much can a properly designed policy grow?

Based on 18+ years of designing high cash value policies, a properly structured whole life policy can deliver 3-5x the original death benefit after 30+ years through strategic use of paid-up additions and dividend reinvestment. A $500,000 policy could potentially provide a $1.5-2.5 million legacy for your beneficiaries. See our cash value chart comparing three different policy designs.

Do beneficiaries pay taxes on whole life insurance cash value or death benefits?

In most cases, no. Life insurance death benefits are received income tax-free by beneficiaries under IRC Section 101. The cash value growth inside the policy is also tax-deferred. However, if the policy has been transferred for value or is owned inside certain trust structures, different rules may apply. For a comprehensive breakdown, see our guide on life insurance tax rules.

What happens to whole life insurance when you turn 65?

Nothing changes automatically at 65. Your policy continues in force, your cash value keeps growing, and your death benefit remains intact (or continues increasing if you’re reinvesting dividends into paid-up additions). If your policy was designed as limited pay whole life (such as paid-up at 65), you simply stop making premium payments while your coverage and cash value continue for life. Many retirees also begin using their cash value to supplement retirement income at this stage.